Find the best estate agent near you Start here

Shared ownership can help some people buy a home when buying outright isn’t possible. But it is a complex scheme with long-term costs and restrictions that are often overlooked. So is shared ownership worth it? That depends on your circumstances and how well you understand the trade-offs. This guide explains how shared ownership works, the pros and cons, and what you need to consider before deciding if it’s right for you.

KEY INFORMATION

Whether shared ownership is worth it depends entirely on your circumstances, how long you plan to stay in the property, and how well you understand the long-term costs and restrictions involved.

For some people, shared ownership can be a useful stepping stone onto the property ladder. For others, it can prove expensive, inflexible and difficult to exit.

Shared ownership may be worth considering if:

In these situations, shared ownership can offer more security than renting and allow you to start building some equity sooner.

Shared ownership is unlikely to be a good idea if:

For these buyers, the downsides of shared ownership – including high ongoing costs, limited control and potential difficulty selling – can outweigh the initial affordability benefits.

If you’re happy to delay buying, shared ownership is not always the best option. In many cases, waiting and buying outright on the open market offers greater flexibility, fewer long-term risks and lower overall costs.

Some buyers may be better off saving for a larger deposit – for example through a Lifetime ISA, which offers a 25% government bonus – or buying with a partner, friend or family member to increase their purchasing power.

That said, if shared ownership is the only realistic way for you to buy a suitable home now – and you’ve fully researched the costs, restrictions and exit options – it can still be worth considering. The key is to treat it as a long-term commitment, not an easy or low-risk shortcut onto the property ladder.

Get fee-free mortgage advice from the award-winning expert advisers at Mortgage Advice Bureau.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Please note some branches of Mortgage Advice Bureau may charge a fee for mortgage advice if you go direct. The fee is up to 1% but a typical fee is 0.3% of the amount borrowed. So make sure you use this site, this form or phone number for fee-free advice.

Shared ownership is a government scheme that lets you buy a share of a property and pay rent on the remaining portion to the housing association or private developer that owns the building.

It’s designed to help people who can’t afford the full purchase price of a home.

Shared ownership works by making the cost of home ownership more affordable because you only buy a share of a property (10%-75%). This means you need a smaller mortgage and deposit. You’ll then pay rent on the share you don’t own.

There are other costs you’ll need to cover including legal and other costs associated with buying a home as well as ongoing costs such as a service charge. Read on to find out more about these.

Also, it’s important to understand that shared ownership schemes are provided by housing associations or private developers. The details, costs and restrictions involved vary by provider so research each one on its individual merits and read the small print of your lease. Getting independent legal advice when you buy is essential, particularly when it comes to shared ownership conveyancing. You can get instant quotes from a conveyancing solicitor to advise you today.

Get instant quotes from regulated and reviewed conveyancing solicitors that cover your area. Our customers save on average £490.

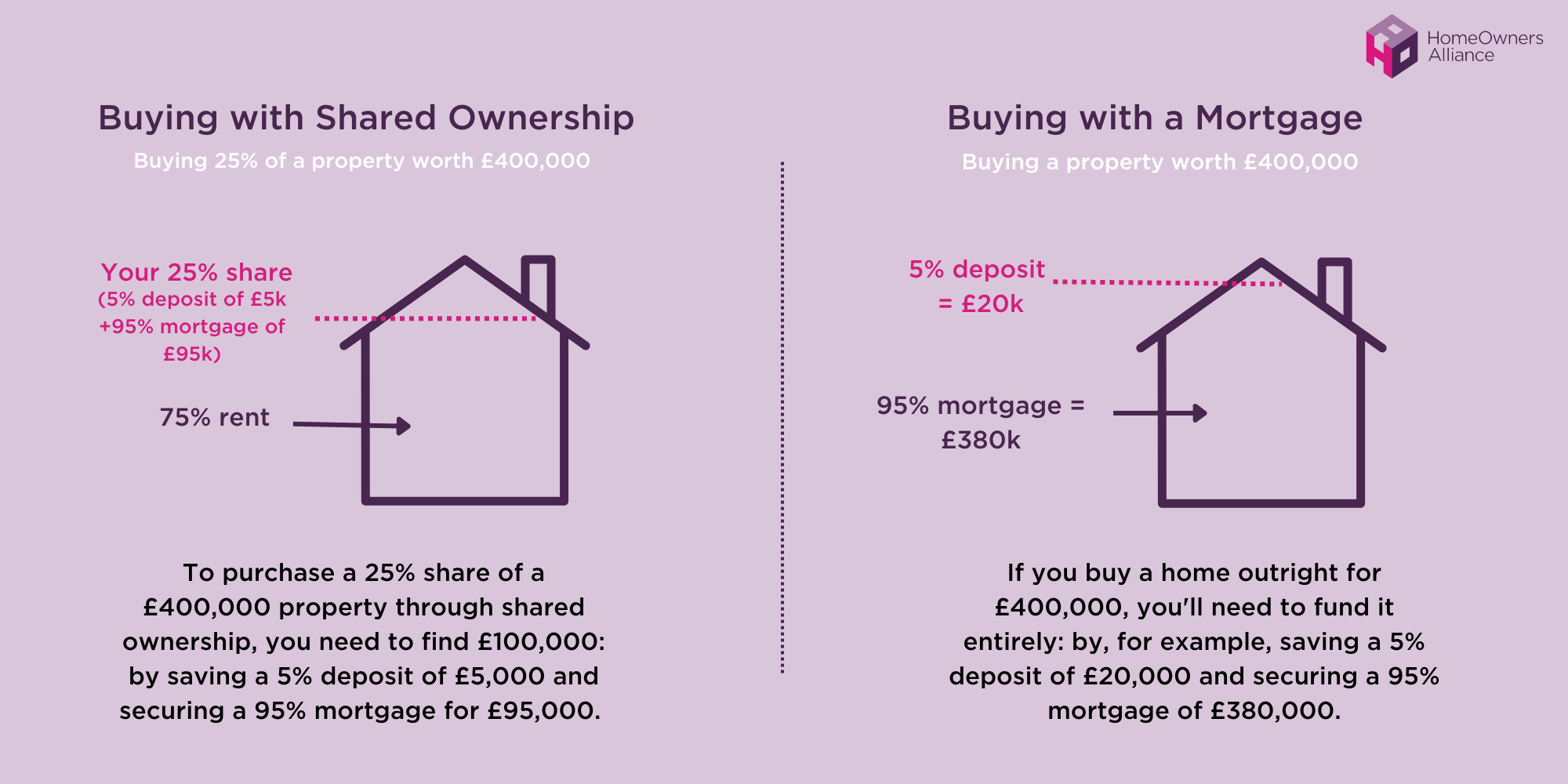

If you’re buying a 25% share of a £400,000 property, your share will be worth £100,000. If you put down a 5% deposit of £5,000, you’ll need a £95,000 mortgage.

| House value | £400,000 |

| Value of your 25% share | £100,000 |

| Deposit amount | £5,000 |

| Mortgage required | £95,000 |

When you buy a share of a new build shared ownership property, the amount of rent you’ll pay initially is based on the value of the share you’re renting.

Homes England’s Capital Funding Guide sets out a maximum initial rent level of 3% on the value of the share the landlord owns, although most landlords charge 2.75%.

Your landlord will then review your rent at the times set out in your lease, it’s usually once a year. Jump for more information on how shared ownership rent increases are calculated each year.

Here’s an example of how much your rent may cost if you buy a 25% share of a £400,000 new build property. In this example, the landlord’s 75% share is worth £300,000.

| House value | £400,000 |

| Value of landlord’s 75% share | £300,000 |

| Annual rent 2.75% x £300,000 | £8,250 |

| Monthly rent | £687.50 |

Buyers beware: Initial rent calculations are only used to calculate the rent for people buying a share of a new build shared ownership property. If you buy a shared ownership resale property, your starting rent will be at the same level as the previous shared owner was paying.

Staircasing your shared ownership property refers to the process of buying additional shares in your property. This increases your ownership percentage, reduces the rent you pay and can eventually lead to full ownership.

Although, check the terms of your lease as this isn’t always possible as some housing providers limit the amount of shares you buy.

How the staircasing process works depends on whether you buy a shared ownership property that was built under the original scheme, or whether you buy a shared ownership home under the new scheme. Find more detailed information on in our guide Staircasing shared ownership explained.

| Shared Ownership available on homes until 2023 | Shared Ownership available on homes from 2022 | |

| Minimum share of property for sale | 25% | 10% |

| Minimum ‘staircasing’ | 10% share each year | 1% share each year, with reduced fees |

| Who covers repairs? | Carrying out repairs is your responsibility | You’ll get support from your landlord for essential repairs for 10 years |

| Landlord’s exclusivity when selling | 8 weeks | 4 to 8 weeks |

When buying a shared ownership house or flat, the legal process is typically more complex than a standard purchase due to the involvement of a housing provider and the terms of the lease.

The shared ownership conveyancing process still covers the usual steps, such as legal searches, raising enquiries and transferring ownership, but your conveyancing solicitor will also need to check the terms of the lease and liaise with both your mortgage lender and the housing association.

Shared ownership solicitors’ fees are often slightly higher than standard conveyancing costs, due to the additional legal work involved.

Because of this added complexity, it’s important to use a conveyancing solicitor with experience in shared ownership purchases. You can get instant quotes from conveyancing solicitors to compare your options.

Get instant quotes from regulated and reviewed conveyancing solicitors that cover your area. Our customers save on average £490.

Shared ownership has both advantages and disadvantages. At a glance, it can make buying a home more affordable in the short term, but it also comes with ongoing costs and restrictions that don’t apply to buying outright.

(The key downsides are explained in more detail below.)

While shared ownership can help some people buy a home, it comes with a number of long-term risks and restrictions that are often underestimated. These downsides can significantly affect affordability, flexibility and your ability to move on in the future.

The best mortgage depends on your personal circumstances. The award-winning expert advisers at Mortgage Advice Bureau will find the right mortgage for you.

Get fee-free mortgage advice from the award-winning expert advisers at Mortgage Advice Bureau.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Please note some branches of Mortgage Advice Bureau may charge a fee for mortgage advice if you go direct. The fee is up to 1% but a typical fee is 0.3% of the amount borrowed. So make sure you use this site, this form or phone number for fee-free advice.

The amount your rent can be increased by a rent review is capped by a formula. However, in times of high inflation, this could rise much more than you had expected.

If you signed your lease on or after 12 October 2023:

Check your lease to see how much your landlord can increase your rent by. It will be either:

If you’ve already bought a shared ownership property and signed your lease before 12 October 2023, the most your rent can go up by is RPI plus 0.5%. Changes to how rent reviews could be calculated were announced by the Department for Levelling Up, Housing and Communities in 2023.

The example on the Government’s shared ownership scheme website gives the following example:

But at HomeOwners Alliance we have highlighted this as misleading. In times of high inflation, this formula means rents can increase by much higher than the figure quoted in the example. If we use the RPI figure from April 2023 of 11.4% and add 0.5%, it means rent could increase by up to 11.9%. This means a rent of £360 a month would increase to around £400 a month.

To be eligible, you must meet certain shared ownership rules / criteria. You must:

Firstly, you may not need to pay stamp duty. When you’re buying a property to live in (assuming it’s not an additional property and that you’re UK-based) you will only pay stamp duty on properties over £125,000. And the threshold for first time buyer stamp duty is higher. First time buyers buying a home up to £300,000 in England and Northern Ireland do not have to pay any stamp duty. And if your new home is worth £300,000 to £500,000 you’ll pay 5% stamp duty, but only on the value above £300,000.

However, if you do need to pay stamp duty you have two options:

If you opt to pay stamp duty in stages, you pay anything that’s due on the first purchase amount. But you then don’t make any further payments until you own more than an 80% share of the property.

You can choose which option’s best for you, depending on your circumstances. You can use HMRC’s stamp duty calculator to work out how much tax you would have to pay if you buy a shared ownership home.

Get fee-free mortgage advice from the award-winning expert advisers at Mortgage Advice Bureau.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Please note some branches of Mortgage Advice Bureau may charge a fee for mortgage advice if you go direct. The fee is up to 1% but a typical fee is 0.3% of the amount borrowed. So make sure you use this site, this form or phone number for fee-free advice.

When it comes to eligibility, with shared ownership London, maximum household income is capped at £90,000 compared to £80,000 outside London.

You can also find organisations selling shared ownership homes outside London on gov.uk and in London at London.gov.uk. If you’re looking for shared ownership houses or flats to buy, another good place to look is the Share to Buy website. You can also find shared ownership properties on portals like Rightmove too.

Before committing to a shared ownership property, it’s essential to look beyond the headline affordability and understand the long-term implications. Based on the issues we see most often, here are some of the key checks we recommend making before you buy:

Get instant quotes from regulated and reviewed conveyancing solicitors that cover your area. Our customers save on average £490.

Yes, even if you only own say a 25% stake in a property you would pay the same amount of council tax as if you owned 100% of the property. Although you may be eligible for a council tax discount or reduction, depending on your circumstances. Read more in our guide Can I get a council tax reduction?

There are fewer shared ownership providers so your mortgage options are more limited. As with all mortgages, you’ll need a good credit history and will have to pass the lender’s affordability checks. Read more in our guide on shared ownership mortgages.

Ultimately, whether it’s hard for you to get a shared ownership mortgage or not will depend on your circumstances. So it’s a good idea to get fee-free mortgage advice.

The main shared ownership cost you’ll pay up front when buying a shared ownership house is your deposit, which must be at least 5% of the share you’re buying. You’ll also need to pay other shared ownership costs like conveyancing fees. You will also have ongoing shared ownership costs like a service charge and you may have to pay for repair and maintenance works too.

With shared ownership schemes you buy a share of 10%-75% of a property with a shared ownership mortgage and pay rent on the remaining share.

This depends on whether you’ve explored all the pros and cons first like whether you would be able to cover increased rent costs or can afford to extend the lease if you need to. If you think it’s the right thing for you, it’s advisable to start looking at shared ownership mortgages to work up more precise costs.

The main pitfalls are around how complicated it is to work out as well as the potential costs further down the line.

Once you’ve worked out the costs at point of purchase, you then really need to estimate ongoing costs during ownership (mortgage payments, rent payments, service charges etc), costs involved in “staircasing” to buy up more shares if that’s something you’re likely to want to do, and costs when it comes to selling a shared ownership – because there are additional costs and restrictions involved in the scheme than if you owned the property outright.

Good question. It certainly needs to be simpler. At HomeOwners Alliance, we believe more needs to be done to make sure shared ownership is a fair and affordable scheme. And the interests of homebuyers needs to be better protected. For more information on what needs to change, read about our Better Shared Ownership Campaign.

Buying a shared ownership house (or flat) involves applying through a housing provider, arranging a shared ownership mortgage, and completing a more complex conveyancing process due to the lease and shared ownership structure.

Yes, buying a shared ownership house is usually more complex because shared ownership houses are usually leasehold, plus your conveyancer will need to deal with a housing provider.

HomeOwners Alliance Ltd is registered in England, company number 07861605. Information provided on HomeOwners Alliance is not intended as a recommendation or financial advice.

HomeOwners Alliance Ltd is an Introducer Appointed Representative of Mortgage Advice Bureau (Derby) Limited which is authorised and regulated by the Financial Conduct Authority.

HomeOwners Alliance Ltd is an Introducer Appointed Representative (IAR) of LifeSearch Limited, an Appointed Representative of LifeSearch Partners Ltd, authorised and regulated by the Financial Conduct Authority. (FRN: 656479).

Independent Financial Adviser service is provided by Unbiased, who match you to a fully regulated, independent financial adviser, with no charge to you for the referral.

HomeOwners Alliance Ltd is an Introducer Appointed Representative (IAR) of Fluent Money Limited, which is authorised and regulated by the Financial Conduct Authority. Calls may be monitored/recorded.

If you take out a mortgage or protection product through Mortgage Advice Bureau, they pay us a referral fee of 25%. You are not obliged to use their services.