Remortgaging when your current deal ends could save you money. But should you fix? And for how long? What if your house value has increased? And when and how do you get the best deal?

Deal ending in next six months? Start the remortgage process now. You can secure a rate, then keep it under review in case a better rate comes up before you switch.

Already on your lender’s SVR? Review your options. SVRs are usually much higher than fixed or tracker deals.

Could you save money? If you remortgage onto a cheaper deal than your current one, you could save money. Remortgaging onto a higher rate will cost more, but could still be much cheaper than rolling onto your lender’s SVR.

Should I remortgage now?

If your current mortgage deal ends in the next six months, you should start the remortgage process now. Speak to a mortgage broker to find the best remortgage deal for you.

In August 2026, mortgage rates are edging back up amid renewed turmoil in the Middle East. Experts warn that it’s a reminder of how quickly markets can shift. By contrast, at the start of July, average fixed mortgage rates were falling at their fastest monthly pace in almost two years.

When the mortgage market is volatile, you can protect against potential rate rises by locking in a rate now, then keep an eye on mortgage rates in case a better deal comes up before you need to switch. The expert advisers at Mortgage Advice Bureau will do this for you.

If you’re on your lender‘s standard variable rate, you should consider reviewing your remortgage options because typical SVR rates can be expensive.

There may be other reasons why you want to remortgage now, such as to fund home improvements or pay off debt. Read on to find out more.

Some people may remortgage early to get a cheaper rate than they’re currently paying. This may be the case if rates have dropped since someone took out their mortgage, or if they now have access to better rates because they’ve built up equity in their property and have a lower LTV. However, it’s important to factor in all the costs, including any early repayment charge, and compare that to any savings you may be able to make by remortgaging early.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Please note some branches of Mortgage Advice Bureau may charge a fee for mortgage advice if you go direct. The fee is up to 1% but a typical fee is 0.3% of the amount borrowed. So make sure you use this site, this form or phone number for fee-free advice.

Can remortgaging save me money?

Remortgaging when your current deal ends could save you money on your mortgage payments, depending on your current mortgage deal and the best mortgage rate you can get.

If you’re among the 1 million households coming off a cheap 5 year fixed rate mortgage in 2026, your new mortgage payments will likely increase. But remortgaging could still save you money because if you do nothing and roll onto your lender’s standard variable rate it could cost you significantly more.

UK Finance figures show that around 1.8 million households’ fixed rate mortgages will end in 2026.

Remortgage example if you’re coming off a cheap 5 year fix

The average 5 year fixed rate mortgage in July 2021 was 2.75%. By comparison, the average 5 year fixed rate mortgage in July 2026 is 5.54%.

Example costs: You took out a 5 year fix when rates were cheap vs remortgaging now

Here’s an illustration of how much you’ll pay at these rates if you borrow £200,000 over 30 years.

Mortgage payment at July 2021’s average rate 2.75%

Mortgage payment at July 2026’s average rate 5.54%

How much more you’ll pay in July 2026

£816

£1,141

£325

Source data: Moneyfacts, 23 July 2026. Figures do not take into account any mortgage fees

But if you do nothing and roll onto your lender’s standard variable rate (SVR), which averaged 7.13% in July 2026, you could pay much more.

Here’s how much you’ll pay on a £200,000 mortgage over 30 years at 7.13%, compared to if you remortgage at July 2026’s average 5 year fix rate of 5.54%.

Mortgage payment at July 2026’s average rate 5.54%

Use our mortgage cost calculator to work out the cost of your mortgage at different rates.

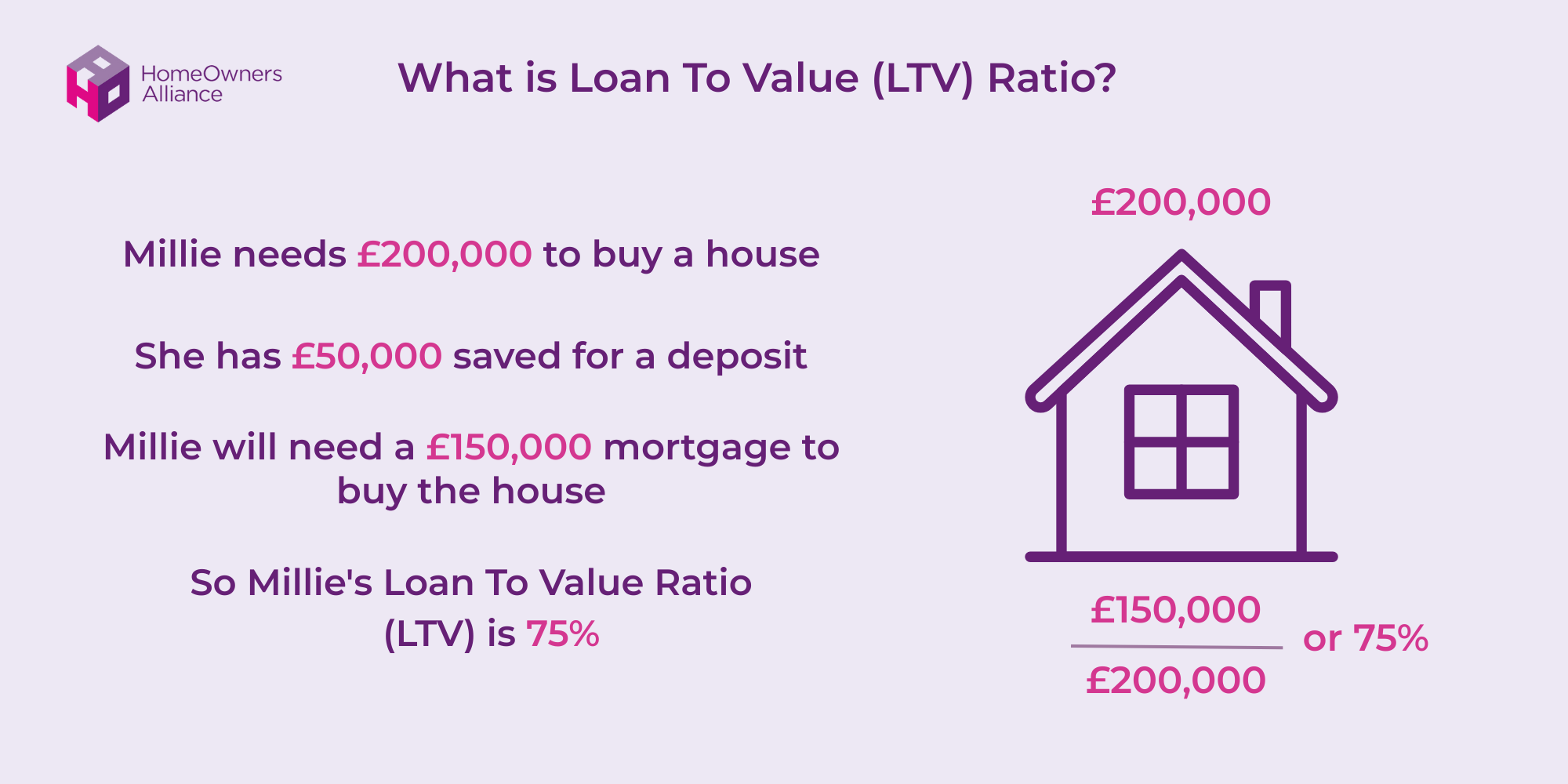

What if my house value has increased?

When you remortgage, one of the factors that determines what mortgage rate you may get access to is your LTV – this stands for loan-to-value, and tells you what percentage of the home’s value is borrowed.

So if your house has increased in value you’ll own a larger proportion of it. Plus, if you’ve taken out a repayment mortgage, you will have built up equity in it via your repayments too.

If you have a lower LTV, you may get access to better mortgage rates.

In July 2026, the best remortgage rate on a 5 year fixed rate at 95% LTV is 5.25% (plus fees) while at 90% LTV the best remortgage rate available on a 5 year fixed deal is 4.73% (plus fees).

Should I remortgage now or wait?

If your current mortgage deal ends in the next 6 months, and certainly if it ends in the next 4 months, you should start the remortgage process now instead of waiting in case mortgage rates go down.

When you’re considering ‘Should I remortgage now?’, start by checking your mortgage deal. Remind yourself of your current rate, check when that deal ends, and penalties for exiting early – often called early repayment charges.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Please note some branches of Mortgage Advice Bureau may charge a fee for mortgage advice if you go direct. The fee is up to 1% but a typical fee is 0.3% of the amount borrowed. So make sure you use this site, this form or phone number for fee-free advice.

What’s happening to UK mortgage rates?

After falling sharply during June, average mortgage rates have started edging back up in July 2026 as many lenders increased fixed mortgage rates.

These moves follow mortgage rates jumping sharply earlier this year following the outbreak of the conflict in the Middle East.

The outlook remains highly uncertain due to global factors. While at home, having a new prime minister has added some political uncertainty into the mix.

So if you need to remortgage, it’s more important than ever to lock in a mortgage deal as soon as possible. You can then keep it under review in case a better deal comes up before you need to complete. Award-winning mortgage brokers Mortgage Advice Bureau offer this service for free.

Read on below for more details on what has been happening to UK mortgage rates.

Here’s a timeline of why mortgage rates have fluctuated in the UK

December 2021: The Bank of England started hiking the base rate from 0.25%. Mortgage rates increased steadily with each increase to interest rates.

September 2022: Mortgage rates had been creeping up steadily with interest rates having increased to 2.25%. But when former prime minister Liz Truss and then chancellor Kwasi Kwarteng announced their disastrous mini-budget that included £45bn of unfunded tax cuts it caused a dramatic increase in mortgage rates.

October 2022: Inflation hits 11.1%.

2023: Mortgage rates fell, before rising again, then falling again as markets predicted the base rate had peaked and would fall in 2024.

Early 2024: Fierce competition in the mortgage market also led to better mortgage rates being available to borrowers. But in the months that followed, lenders hiked fixed rate mortgages in response to the expectation that interest rate cuts would be slower and fewer than had previously been predicted.

August 2024: Following August’s base rate cut from 5.25% to 5%, mortgage lenders started slashing rates on fixed deals.

November 2024: Mortgage rates on fixed deals started increasing in November 2024 despite the Bank of England’s decision to cut interest rates again to 4.75%, due to the expectation that interest rates are likely to stay higher for longer.

December 2024: Mortgage rates edged higher before nudging back down. This was despite the Bank of England’s decision to hold interest rates at 4.75% on 19 December.

January 2025: Mortgage rates edge up as markets predict interest rate cuts will be slower and shallower than previously expected.

March 2025: Average mortgage rates nudged down after several major lenders cut rates following the Bank of England’s decision to cut interest rates in February from 4.75% to 4.5%.

June 2025: A growing number of UK lenders cut mortgage rates as the fallout from US tariffs continued to fuel forecasts of deeper than expected interest rate cuts. However, as these fears subsided, mortgage rates crept up before settling.

July 2025 Mortgage rates on fixed deals nudge down as lenders compete to trim rates. However, inflation figures for June showed an unexpected increase to 3.6%.

August 2025: Fixed rate mortgages in the UK continued to fall as lenders cut mortgage rates ahead of the Bank of England’s interest rates announcement on 7 August. However, this vote was closer than expected, which led to many economists scaling back predictions of a further interest rate cut in 2025. While after higher than expected inflation figures for July, experts warned rates cuts on fixed deals may slow or even reverse.

September 2025 Bank of England governor Andrew Bailey warns there’s ‘considerably more doubt’ about when further interest rate cuts would be made. Fixed rate mortgages in the UK creep up amid growing inflation fears. However, as the month progressed some lenders trimmed rates, while others continued to nudge rates up.

October 2025: Lenders started cutting mortgage rates on fixed deals after better than expected inflation figures led to predictions that interest rates may be cut sooner than previously expected.

November: 2025 Mortgage price war heats up. Bank of England holds interest rates at 4% but considered more likely than not to cut interest rates in December. Inflation cools to 3.6%, raising hopes of a December interest rate cut. Chancellor Rachel Reeves’ Budget on 26 November not expected to reverse drops in mortgage rates as it avoided major market jitters.

December 2025:Figures show inflation fell in November 2025 to 3.2%, lower than expected. Bank of England cuts interest rates from 4% to 3.75%. Mortgage price war gathers pace.

January 2026:Figures show inflation in December increased by more than expected to 3.4%. Mortgage rates edge up.

February 2026: Worse than expected employment data is released and figures show inflation fell in January. Experts say these boost chance of a March interest rate cut. Mortgage rates start to fall.

March 2026: The US-Israel war with Iran sends the price of oil and gas soaring, increasing inflation risk and delays of interest rates cuts. Fixed mortgage rates edge up. Bank of England holds interest rates at 3.75%. Following the decision, traders predict two interest rate hikes in 2026.

April 2026: Some lenders started cutting mortgage rates as market volatility eased following the ceasefire. Inflation figures for March show rise to 3.3%, up from 3% in February. Bank of England held interest rates at 3.75%.

May 2026: Inflation falls to 2.8% in April, as a reduction in the household energy price cap helped soften the sharp rise in fuel costs since the start of the Iran war.

June 2026: UK inflation rate unexpectedly remains at 2.8% in May. Bank of England holds interest rates at 3.75%.

July 2026: Mortgage rates start edging back up amid renewed hostilities in the Middle East. The Bank of England holds Bank Rate at 3.75% for a fifth consecutive meeting, with the MPC voting 7–2 to hold.

Current best mortgage rates – remortgaging

Here’s an overview of the current best mortgage rates at different deposit levels for 2 and 5 year fixed rate mortgages and 2 year tracker mortgages if you’re remortgaging.

Source: Mortgage Advice Bureau. Updated: 6 August 2026. Find more about our rates data here. The best mortgage for you depends on your personal circumstances.

The best mortgage depends on your personal circumstances. The award-winning expert advisers at Mortgage Advice Bureau will find the right mortgage for you.

Should I fix my mortgage?

Some people choose to fix their mortgage because it gives them budgeting certainty that the amount they’ll pay each month on their mortgage won’t change.However, if you fix your mortgage, while your repayment amounts won’t increase during the term they won’t go down either, such as if the Bank of England cuts interest rates.

How long should I fix my mortgage for?

If you’re asking should I remortgage now and want a fixed rate mortgage, you’ll need to decide how long you want to fix for.

Should I fix my mortgage for 2 or 5 years?

Whether a 2 or 5 year fixed rate mortgage is best for you will depend on your circumstances. You may want to fix for 2 years in the hope that mortgage rates will improve in the near future and that you’ll be able to remortgage onto a cheaper deal once your 2 year deal ends.

However, you may prefer the security of a 5 year term or you might opt for a 3 year fix.

Should I fix for 10 years or longer?

The advantages of fixing for 10 years or longer are that you’ll have the security of knowing how much you’ll pay on your mortgage for a longer period. Plus, you may pay less in arrangement fees than if you take out multiple 2 or 5 year mortgages.

Fixing your mortgage for 10 years or longer also protects you against changes to lending criteria; if a lender tightens up its lending criteria it may make it harder for you to get a mortgage.

However, fixing your mortgage for such a long time means you may run the risk of potentially missing out on better deals in the meantime.

Also consider what would happen if you move house? Some mortgage deals are portable which means you can take it with you penalty-free if you move house. However, there is no guarantee that the lender will let you do this.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Please note some branches of Mortgage Advice Bureau may charge a fee for mortgage advice if you go direct. The fee is up to 1% but a typical fee is 0.3% of the amount borrowed. So make sure you use this site, this form or phone number for fee-free advice.

Fixed vs variable rate and tracker mortgages

When you’re asking should I remortgage now, how do tracker mortgages and discounted variable rate mortgages compare to fixed rate mortgages?

Tracker mortgage: These go up and down in line with the base rate they track, usually the Bank of England base rate. So if there’s a cut in interest rates, the amount you’ll pay on your mortgage each month would reduce.

Discounted variable rate mortgages: These work in a similar way but instead of tracking the base rate, they track the lender’s SVR at a discounted rate.

Some variable rate mortgages come with no early repayment charges which means you could switch to a different deal later down the line without having to pay a hefty penalty. For more information read our guide: What type of mortgage should I get?

Can I fix a new deal before the end of my current mortgage?

Yes. You can start the remortgage process now if your current deal ends within the next six months, so that you’re ready to roll onto the new deal when your current deal ends.

Can I remortgage in the middle of my mortgage deal?

There are lots of reasons why you may want to remortgage in the middle of a mortgage deal such as remortgaging to release equity from your home. But whether it’s right for you will depend on your circumstances.

Firstly, will you need to pay an early repayment charge if you remortgage? It’s vital you check this because these can be substantial. It’s advisable to talk it through with a mortgage broker.

Secondly, you’ll want to consider the rate you can get now compared to the rate you’re currently on.

So if you’re asking should I remortgage now? and you’re in the middle of a mortgage deal, it’s important to get advice.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Please note some branches of Mortgage Advice Bureau may charge a fee for mortgage advice if you go direct. The fee is up to 1% but a typical fee is 0.3% of the amount borrowed. So make sure you use this site, this form or phone number for fee-free advice.

Should I move to my lender’s Standard Variable Rate?

In most cases, moving to your lender’s standard variable rate isn’t advisable because they can be extremely expensive, and you may be able to save money by remortgaging.

However, an SVR mortgage might be the right solution for some, for example, if you have a small mortgage.

But if you’re asking ‘Should I remortgage now?’, don’t assume what the best option for you will be. Always speak to a fee-free broker to make sure you get the best mortgage deal for you.

Why else should I remortgage now?

Apart from saving money, there are other reasons you may ask ‘should I remortgage now?’ including:

Funding home improvements: If you’re planning an extension or home improvements, you may be able to fund the project by remortgaging and releasing equity from your home. See how to finance home improvements.

Paying off debts: Some people remortgage to release equity to pay off debts they’ve accrued. However, if you do this your mortgage will be bigger and you may pay more interest in the long term. So it’s a good idea to get independent financial advice.

To make overpayments. Another reason why you may want to remortgage is if you want to overpay on your mortgage and your current deal doesn’t let you do this.

However, what’s right for you will depend on your circumstances so it’s a good idea to get expert advice.

If you’re asking ‘Should I remortgage now?’, you’ll also need to make sure you’re in good financial shape before you apply to remortgage.

This includes checking your credit rating and taking steps to improve it if necessary, staying out of your overdraft and paying all your bills on time. Find more tips in our guide How to get a mortgage in 6 easy steps.

Why shouldn’t I remortgage now?

There are some circumstances which mean remortgaging may not be the right option for you such as:

If you are in negative equity, it is very unlikely you will find a remortgage deal.

If your financial circumstances have changed since you took out your current mortgage such as you’ve stopped working or recently become self-employed.

However, what’s right for you will depend on your personal circumstances. So it’s advisable to get expert mortgage advice.

Should I switch to an interest-only mortgage?

If you’re asking should I remortgage now, you may be considering switching to an interest-only mortgage. If so you’ll need to consider:

Your monthly payments will be cheaper because you only pay the interest on your mortgage each month; you don’t pay off any of the capital. But an interest-only mortgage will usually cost you more than a repayment mortgage over its lifetime because you pay interest on the full amount throughout.

The few lenders that offer interest-only mortgages on residential properties often require large deposits (50-60%), large annual household incomes (£75,000 to £100,000) or high-value repayment vehicles such as pension pots, the value of which must be 150% of the balance of the mortgage secured.

Interest-only mortgages can be high-risk. What if your plan to pay back your mortgage at the end of the term doesn’t work? Find out more in our guide on Interest-only mortgages

Whether or not paying off your mortgage is right for you will depend on your circumstances and there are pros and cons to consider. For more information, read our guide Should I pay off my mortgage.

Best mortgage rates methodology

At HomeOwners Alliance the best mortgage rates in our tables are from the expert advisers at Mortgage Advice Bureau and updated regularly. These best mortgage rates do not take into account fees and are for illustration only. The average mortgage rate figures we use are from sources including Rightmove and Moneyfacts.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Please note some branches of Mortgage Advice Bureau may charge a fee for mortgage advice if you go direct. The fee is up to 1% but a typical fee is 0.3% of the amount borrowed. So make sure you use this site, this form or phone number for fee-free advice.

Frequently Asked Questions

Is now a good time to remortgage?

Generally, it is a good time to remortgage if you’re in the last 6 months of your current mortgage deal. You can lock in a deal, then keep it under review in case you find a better deal. Remortgaging means you’ll avoid your lender’s expensive standard variable rate mortgage. However, when is a good time for you to remortgage will depend on your personal circumstances.

What are the risks of remortgaging too early?

If you remortgage before the end of your current deal, you may need to pay an early repayment charge. But you can start the remortgage process 6 months before your current mortgage deal ends – this means you can switch to your new deal straight afterwards.

Is it better to remortgage or do a product transfer?

Remortgaging with a new lender means you’ll usually have a wider choice of deals than if you take out a new deal with your existing lender – known as a product transfer. But a product transfer can be quicker and easier. The right decision for you will depend on your circumstances, so it’s a good idea to get advice from a mortgage broker.

HomeOwners Alliance Ltd is registered in England, company number 07861605. Information provided on HomeOwners

Alliance is not intended as a recommendation or financial advice.

HomeOwners Alliance Ltd is an Introducer Appointed Representative of Mortgage Advice Bureau (Derby) Limited which is authorised and regulated by the Financial Conduct Authority.

HomeOwners Alliance Ltd is an Introducer Appointed Representative (IAR) of LifeSearch Limited, an Appointed

Representative of LifeSearch Partners Ltd, authorised and regulated by the Financial Conduct Authority. (FRN:

656479).

Independent Financial Adviser service is provided by Unbiased, who match you to a fully regulated, independent

financial adviser, with no charge to you for the referral.

HomeOwners Alliance Ltd is an Introducer Appointed Representative (IAR) of Fluent Money Limited, which is authorised and regulated by the Financial Conduct Authority. Calls may be monitored/recorded.

If you take out a mortgage or protection product through Mortgage Advice Bureau, they pay us a referral fee of 25%. You are not obliged to use their services.