Find the best estate agent near you Start here

If you’re on your lender's Standard Variable Rate (SVR) mortgage you could be paying £100s more every month than you need to. We explain how SVR mortgages work, the current SVR rates what to do if you’re on one.

KEY INFORMATION

A standard variable rate (SVR) mortgage is a type of variable rate mortgage you’ll usually be moved onto when your fixed-term mortgage deal ends.

The standard variable rate (which is the rate you’ll pay on an SVR mortgage) is set by the lender and can change at any time. This means you’re at the whim of your mortgage lender.

Standard variable rate mortgages can be extremely expensive. If you’re already on your lender’s SVR you might be able to save £100s a month by remortgaging.

And if your current mortgage deal is ends in the next 6 months, start shopping around now to see if you can remortgage and save money.

The best mortgage depends on your personal circumstances. The award-winning expert advisers at Mortgage Advice Bureau will find the right mortgage for your individual circumstances.

Get fee-free remortgage advice from the award-winning expert advisers at Mortgage Advice Bureau.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Please note some branches of Mortgage Advice Bureau may charge a fee for mortgage advice if you go direct. The fee is up to 1% but a typical fee is 0.3% of the amount borrowed. So make sure you use this site, this form or phone number for fee-free advice.

Mortgage lenders set their own standard variable rates. These can be influenced by changes to the Bank of England base rate but unlike tracker mortgages, standard variable rates don’t track above the base rate at a fixed amount.

Plus, other factors like the cost of borrowing can influence what a lender sets its SVR mortgage rates at. And a lender can increase or decrease its SVR whenever it chooses to.

For example, if the Bank of England reduces interest rates by 0.5%, the lender may:

If you take out a fixed rate mortgage, the rate you’ll pay will remain the same during your initial term.

The size of your mortgage payments will depend on the size of your loan, the length of the term and your lender’s SVR:

Here’s an example to illustrate how much more you’ll pay on a standard variable rate mortgage, compared to if you remortgage.

These examples are based on taking out a mortgage over 30 years, based on an SVR of 7.5% compared to if you remortgage on a rate of 4%. These examples doesn’t include any mortgage fees.

Example 1: £200,000 mortgage

| Mortgage payment at 4% | Mortgage payment at 7.5% | £ Difference per month |

| £955 | £1,398 | £443 |

Example 2: £300,000 mortgage

| Mortgage payment at 4% | Mortgage payment at 7.5% | £ Differenceper month |

| £1,432 | £2,098 | £666 |

Get fee-free remortgage advice from the award-winning expert advisers at Mortgage Advice Bureau.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Please note some branches of Mortgage Advice Bureau may charge a fee for mortgage advice if you go direct. The fee is up to 1% but a typical fee is 0.3% of the amount borrowed. So make sure you use this site, this form or phone number for fee-free advice.

Here are the steps to take to find out what your lender’s standard variable rate is:

SVR mortgage rates can be painfully high and many people can save money by remortgaging onto a new fixed or tracker deal when their current deal ends.

However, the best mortgage for you depends on your personal circumstances. So get fee-free advice from the expert advisers at Mortgage Advice Bureau.

Paula Higgins, CEO of HomeOwners Alliance, said:

“The staggering SVRs we are seeing from some lenders at the moment is nothing short of daylight robbery. So we’re calling on all homeowners to check the rate they’re on. If it’s the SVR, they need to look at their options asap.

If your current mortgage term comes to an end in the next six months, start looking now to secure a rate and avoid defaulting onto the lender’s SVR.”

Paula also warns that standard variable rates are ‘completely inconsistent between lenders, making it harder for consumers to track’.

Get fee-free mortgage advice from the award-winning expert advisers at Mortgage Advice Bureau.

Get fee-free remortgage advice from the award-winning expert advisers at Mortgage Advice Bureau.

Some people may decide a standard variable rate mortgage is right for them.

But don’t assume what the best option for you will be. Always get expert advice.

So what are the advantages of a standard variable mortgage?

The best mortgage depends on your personal circumstances. The award-winning expert advisers at Mortgage Advice Bureau will find the right mortgage for you.

Get fee-free remortgage advice from the award-winning expert advisers at Mortgage Advice Bureau.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Please note some branches of Mortgage Advice Bureau may charge a fee for mortgage advice if you go direct. The fee is up to 1% but a typical fee is 0.3% of the amount borrowed. So make sure you use this site, this form or phone number for fee-free advice.

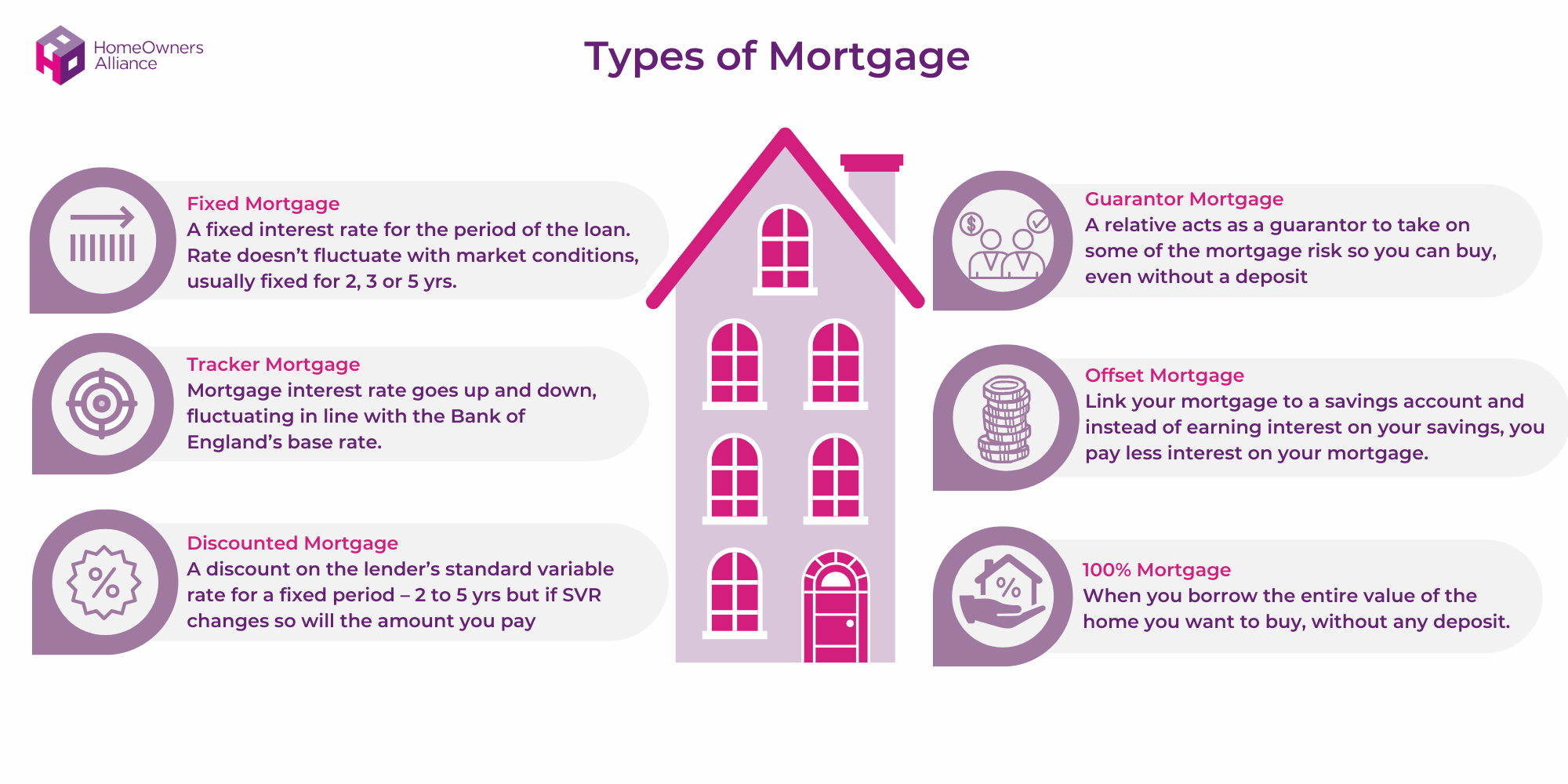

There are lots of different types of mortgages available. These include:

Find out more information in our guide on Understanding mortgage types and what one you need to get.

Here’s how SVR mortgages compare to tracker mortgages:

| SVR | Tracker mortgage |

|---|---|

| The rate you’ll pay is set by the lender. | The rate you’ll pay is fixed at a set level above the Bank of England base rate |

| Lenders can change the rate at any time. | The rate you’ll pay will change of the Bank of England increases or decreases interest rates. |

| The lender may not pass on all, or any, of an interest rates cut. | If the Bank of England cuts interest rates by 0.25%, the rate you’ll pay on your mortgage will reduce by the same amount. |

| You won’t usually need to pay an Early repayment charge if you switch to a new deal. | You may need to pay an early repayment charge if you switch to a new deal during your initial term. But not always. Check your paperwork. |

No, you don’t take out a standard variable rate mortgage. You’ll usually be switched onto an SVR mortgage when your fixed term deal ends, unless you remortgage

If you’re weighing up staying on the SVR or remortgaging onto a new fixed, tracker or discounted variable rate mortgage, the easiest way to find the best mortgage for you is by speaking to a mortgage broker.

They’ll compare the best mortgage rates and terms to find the best mortgage for you.

You can use our mortgage cost calculator to work out the monthly and total cost of your mortgage. Plus, you can compare the cost of two mortgages – for example, the SVR vs a remortgage.

Get fee-free mortgage advice from the award-winning expert advisers at Mortgage Advice Bureau.

Get fee-free remortgage advice from the award-winning expert advisers at Mortgage Advice Bureau.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Please note some branches of Mortgage Advice Bureau may charge a fee for mortgage advice if you go direct. The fee is up to 1% but a typical fee is 0.3% of the amount borrowed. So make sure you use this site, this form or phone number for fee-free advice.

When your fixed rate mortgage ends you’ll usually be moved onto your lender’s standard variable rate. The rate you’ll pay could increase significantly, leaving you with bigger monthly payments.

You can avoid this by remortgaging onto a new deal. You can start the remortgage process 6 months before your current deal ends, then keep the rate under review in case you find a better deal.

You can find a wide selection of the best standard variable mortgage rates by checking our current SVR mortgage rates table.

Most people can save money by remortgaging onto a new deal instead of moving onto their lender’s Standard variable rate, but what’s right for you will depend on your circumstances. So it’s a good idea to speak to an expert mortgage broker who will find the right mortgage for you

There isn’t a set standard variable mortgage rate, each lender will set its own rates, although, in spring 2026, the average standard variable rate in the UK was 7.13%. This is significantly higher than the best mortgage rates available.

However, the best mortgage for you depends on your personal circumstances. The award-winning expert advisers at Mortgage Advice Bureau will find the right mortgage for you.

An SVR mortgage is a type of variable rate mortgage you’re moved onto when your fixed-term mortgage deal ends. So if you take out a 5 year fixed rate mortgage, you’ll typically move to your lender’s standard variable rate at the end of the 5 year term unless you remortgage onto a new deal.

The lender sets the standard variable rate you’ll pay and can change the SVR at any time. SVR mortgages can be very expensive.

Each lender sets its own SVR and this can be much higher than the Bank of England base rate.

Lenders can change their SVR at any time but they usually change their SVRs after the Bank of England cuts or increases interest rates. But they won’t necessarily make changes when this happens.

A good SVR rate in 2026 is 6%-6.5%. But you may be able to get a much lower mortgage rate than this by remortgaging.

Variable rate mortgage refers to a range of mortgages where the rate you pay can go up or down. These mortgages include tracker mortgages, discounted variable rate mortgages and standard variable rate mortgages.

Variable rate mortgages are different to fixed rate mortgages where the rate you’ll pay is fixed for a set period of time.

HomeOwners Alliance Ltd is registered in England, company number 07861605. Information provided on HomeOwners Alliance is not intended as a recommendation or financial advice.

HomeOwners Alliance Ltd is an Introducer Appointed Representative of Mortgage Advice Bureau (Derby) Limited which is authorised and regulated by the Financial Conduct Authority.

HomeOwners Alliance Ltd is an Introducer Appointed Representative (IAR) of LifeSearch Limited, an Appointed Representative of LifeSearch Partners Ltd, authorised and regulated by the Financial Conduct Authority. (FRN: 656479).

Independent Financial Adviser service is provided by Unbiased, who match you to a fully regulated, independent financial adviser, with no charge to you for the referral.

HomeOwners Alliance Ltd is an Introducer Appointed Representative (IAR) of Fluent Money Limited, which is authorised and regulated by the Financial Conduct Authority. Calls may be monitored/recorded.