Find the best estate agent near you Start here

Buying your first home is exciting but there’s a lot you’ll need to know about first time buyer mortgages. We look at what deposit you’ll need, how much you can borrow, your first time buyer mortgage options, how to apply and how to boost your chances of getting your mortgage application accepted.

A first time buyer mortgage is a mortgage for someone buying their first home. Most buyers need at least a 5% deposit, although some lenders offer 100% mortgages. The right mortgage will depend on your deposit, income and personal circumstances.

KEY INFORMATION

Get fee-free mortgage advice from the award-winning expert advisers at Mortgage Advice Bureau.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Please note some branches of Mortgage Advice Bureau may charge a fee for mortgage advice if you go direct. The fee is up to 1% but a typical fee is 0.3% of the amount borrowed. So make sure you use this site, this form or phone number for fee-free advice.

Start by getting an idea of how much you might be able to borrow using this How much can I borrow calculator. If you’re buying alone just leave the partner’s salary blank.

A mortgage affordability calculator gives you a starting point. The calculation assumes you can borrow 5x your salary.

To get a more accurate picture speak to a fee-free mortgage broker about your salary, outgoings and credit rating to find out how big a mortgage you can borrow and to check whether the monthly repayments are affordable. This is also a good time to check and improve your credit rating, click here to jump to how you can do this.

Your next step is to get a Mortgage in Principle (sometimes called an agreement or decision in principle). This is a statement from a lender on how much they would lend you ‘in principle’ based on information you have provided about your income and outgoings.

It’s advisable to get a mortgage in principle as early in the home buying process as possible, ideally before you start house-hunting. You want to be seen as a serious buyer, ready to proceed, before you make your first offer.

You can speak to the fee-free expert advisers at Mortgage Advice Bureau to arrange a Mortgage Agreement in Principle today.

Once you have found a property and had an offer accepted, you can start the formal mortgage application process. Your mortgage broker can take this forward for you. The lender will carry out a full credit check, undertake a mortgage valuation of the property and once happy with your application will issue a formal mortgage offer.

While every purchase is different, the mortgage process for first time buyers usually follows these steps:

| Stage | What happens |

|---|---|

| 1. Check your budget | Use an affordability calculator or speak to a mortgage broker to find out how much you could borrow. |

| 2. Get a Mortgage in Principle | This shows sellers you’re a serious buyer and gives you a clear budget before you start house hunting. |

| 3. Find a property | View homes, make an offer and have it accepted. |

| 4. Apply for your mortgage | Submit your full mortgage application and provide supporting documents. |

| 5. Mortgage valuation | Your lender checks the property’s value before making a formal offer. |

| 6. Receive your formal mortgage offer | Once approved, your lender issues a formal mortgage offer. |

| 7. Exchange contracts | You become legally committed to buying the property. |

| 8. Complete your purchase | Your mortgage funds are released and you get the keys to your new home. |

Get fee-free mortgage advice from the award-winning expert advisers at Mortgage Advice Bureau.

Mortgage lenders usually require at least 5% of the value of the property as a deposit. 5% deposit mortgages usually come with higher mortgage rates than you would get if you had saved a bigger deposit. The bigger your deposit, the wider the choice of lenders and potentially lower (i.e. cheaper) mortgage rates you’ll typically be able to access.

The average deposit first time buyers paid in 2024 was £61,090 with deposits averaging 20% of the purchase price, according to Halifax. First time buyers in London paid an average deposit of £124,688.

Specialised mortgage products such as Track record mortgages designed for renters with a proven rental payment history can help first time buyers purchase without a deposit.

This table shows how much you’d need to save for a deposit on a £300,000 home.

| Cost of property | Deposit % | Deposit in £ |

|---|---|---|

| £300,000 | 5% | £15,000 |

| £300,000 | 10% | £30,000 |

| £300,000 | 15% | £45,000 |

| £300,000 | 20% | £60,000 |

It’s possible to get a first time buyer mortgage with no deposit. Here are two ways to do this:

You can take out a 100% mortgage. For example, Skipton’s Track Record mortgage is designed for those with a ‘track record’ of paying rent and mortgage lender April’s 100% mortgage for those prepared to take out a fixed rate mortgage for 10 or 15 years. Find more information including on eligibility in our guide 100% mortgages: Should I get one?

With guarantor mortgages, you can buy a house with no deposit, if you have a loved one who is prepared to put up savings or a property as security against the loan. Family Springboard mortgages work in a similar way. We explain all your options and what to consider in our guide on how to get a mortgage with no deposit.

There are risks with all mortgages – your home or property may be repossessed if you don’t keep up repayments on your mortgage. But if you take out a mortgage with a small or no deposit, there is a greater risk of negative equity than if you get a mortgage with a larger deposit. Negative equity is when the value of your home is lower than your outstanding mortgage balance.

Get fee-free mortgage advice from the award-winning expert advisers at Mortgage Advice Bureau.

Here’s what a lender will assess when deciding how much they’ll let you borrow on a mortgage

| Factor | How it affects how much you can borrow |

|---|---|

| Salary | Lenders will typically lend up to 4.5 x your salary, but some lend bigger multiples. Find out more in our guide to the Best mortgage lenders. Bonuses and income from second jobs may be considered in this. |

| Outgoings | Lenders will go through your outgoings and monthly financial commitments, such as childcare costs and outstanding loans, when determining how much they may lend you. |

| Credit history | Lenders will check your credit history. If you have bad credit, it may be harder to get a mortgage or borrow as much. Read our guide 11 Tips to improve your credit score for a mortgage. |

For example, say you and your partner have a combined income of £60,000 and a lender says it will lend you 4.5 times this amount, this means you can borrow a maximum of £270,000.

If you have saved £30,000 for your deposit, this means you can buy a £300,000 house with a 10% deposit and take out a £270,000 mortgage for the remaining 90%.

| Source of £ | Amount |

|---|---|

| Deposit | £30,000 |

| Mortgage | £270,000 |

| Total | £300,000 |

However, this example doesn’t take into account the other costs of buying a house such as solicitor fees when buying a house and survey costs. Read more in our guide on the Costs of buying a house.

Once you know how much you can borrow and how much deposit you’ve saved, you can start comparing first time buyer mortgage rates.

If you’re a first time buyer, mortgage calculators are a good place to start to see how much you can afford to borrow. The following affordability calculator shows you instantly how much you may be able to borrow and afford based on your income. While the following mortgage cost calculator will also give you an idea of what your monthly mortgage costs are likely to be.

Get fee-free mortgage advice from the award-winning expert advisers at Mortgage Advice Bureau.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Please note some branches of Mortgage Advice Bureau may charge a fee for mortgage advice if you go direct. The fee is up to 1% but a typical fee is 0.3% of the amount borrowed. So make sure you use this site, this form or phone number for fee-free advice.

Our Mortgage Expert Sarah Tucker says,

“I would always recommend speaking to a mortgage adviser as early as possible, even if you think buying a property is still years away. It can be incredibly valuable in helping you understand how much you may need to save, what affordability could look like and what early steps you may need to take.

That early guidance can be especially useful if you’re self-employed or if your situation needs a bit more planning. My message to first-time buyers is that homeownership is still very achievable and there are lots of products and schemes designed to help people get there.”

Before comparing first time buyer mortgage rates, make sure you know:

Mortgage rates vary between lenders so as a first time buyer, you could save a considerable amount of money in the long term by shopping around for the best deal for you.

Here are the best first time buyer mortgage rates on offer in July 2026 if you have a 10% deposit and are looking for a 2 year fixed rate mortgage. Mortgage rates tend to differ depending on your loan to value (LTV). Calculate your loan to value ratio instantly with our simple mortgage loan to value calculator.

For a full range of the best mortgage rates at all deposit levels from 0% to 40%, for 2 year and 5 year fixed rate mortgages and the best rates on variable rate mortgages, read our guide on the Best first time buyer mortgage rates, which is updated regularly.

Here are the lowest mortgage rates this month if you’ve got a 10% deposit. The monthly mortgage cost examples are based on borrowing £200,000 over 30 years.

| Lender | Initial Rate | Fees | Monthly Payment | APRC | Annual Cost | Max LTV | Rep. Example |

|---|---|---|---|---|---|---|---|

| Danske Bank | 4.58% | £1,124 | £1,027 | 6.1% | £12,383 | 90% | Details |

| Halifax | 4.69% | £1,099 | £1,040 | 7.0% | £12,530 | 90% | Details |

| West Brom Building Society | 4.78% | £1,624 | £1,054 | 6.2% | £12,702 | 90% | Details |

| HSBC | 4.84% | £1,016 | £1,059 | 6.2% | £12,710 | 90% | Details |

| West Brom Building Society | 4.84% | £1,124 | £1,059 | 6.2% | £12,758 | 90% | Details |

The best mortgage depends on your personal circumstances. The award-winning expert advisers at Mortgage Advice Bureau will find the right mortgage for your individual circumstances.

Get fee-free mortgage advice from the award-winning expert advisers at Mortgage Advice Bureau.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Please note some branches of Mortgage Advice Bureau may charge a fee for mortgage advice if you go direct. The fee is up to 1% but a typical fee is 0.3% of the amount borrowed. So make sure you use this site, this form or phone number for fee-free advice.

The best mortgage lender for you as a first time buyer will depend on your circumstances. But some lenders offer special products designed for first time buyers. For example:

Find out more in our guide to the best mortgage lenders.

Lifetime ISAs are for your first home or your retirement. Anyone aged 18-39 can open a LISA. You can save up to £4,000 each tax year into it and the government will give you a 25% bonus on your contributions, up to a max of £1,000 per year. However, there are restrictions on how you can use the money so be clear on that before saving into one. Find out more in our Best Lifetime ISA guide.

The Mortgage Guarantee scheme isn’t a scheme you specifically apply for, it was designed to encourage lenders to offer 95% mortgages. However, many lenders offering 95% mortgages don’t use this scheme. It’s open to home movers as well as first time buyers. This scheme ended in June 2025 and was replaced by the Freedom to Buy Mortgage scheme which works in a similar way.

You buy a share of a property (usually 25%-75%) and pay rent on the rest, so you’ll need a smaller mortgage and smaller deposit than if you buy on the open market. But there are pros and cons to this complicated scheme. Read more in Shared Ownership: What is it? Is it worth it?

The First Homes scheme offers newly built homes to local first time buyers with a discount of at least 30% which stays on the First Home forever.

However, there’s criteria you’ll need to meet to be eligible:

Get fee-free first time buyer mortgage advice from the award-winning Mortgage Advice Bureau.

You’ll need to decide what type of first time buyer mortgage to take out:

| Mortgage type | What it means |

|---|---|

| Fixed rate mortgage | You’ll pay a fixed rate during your initial term, usually 2-5 years. So you won’t pay more on your monthly mortgage payments if interest rates increase, but you won’t pay less if they fall either. |

| Tracker mortgages | The rate you’ll pay will go up and down in line with the base rate. This means if the Bank of England cuts interest rates, your mortgage payments will go down. But if it hikes interest rates, your mortgage payments will go up. |

| Discounted mortgages | Discounted mortgages track under the lender’s standard variable rate. So your rate may go up or down, but this depends on any changes the lender decides to make to its standard variable rate. |

| Offset mortgages | With an offset mortgage, you use a linked savings account to offset the amount you owe on your mortgage – this means instead of earning interest on your savings, you pay less interest on your mortgage. If you’re a first time buyer and you have a large chunk of savings you might be better off using these for your deposit. But your fee-free mortgage broker will talk you through it to help you make the best decision for you. |

| Guarantor mortgages | These allow you to get a mortgage even if you have no deposit. A mortgage guarantor is someone – usually a parent, a relative or even a close friend – who takes on some of the risk of the mortgage by acting as a guarantor. This usually involves them offering their savings or their home as security against the loan and committing to making the mortgage payments if the borrower defaults. |

| 100% mortgages | These allow you to take out a mortgage with no deposit. Although downsides include higher mortgage rates compared to if you’ve saved a deposit. For more details see our guide on 100% mortgages. |

Get fee-free mortgage advice from the award-winning expert advisers at Mortgage Advice Bureau.

When you apply for a mortgage, the lender will check your credit report and what’s contained in it will be a factor in whether your mortgage application is accepted or not. It can also have a bearing on the mortgage rate you’re offered and how much you can borrow.

So make sure you check your credit reports first. You can request your report from the three credit referencing agencies (Experian, Equifax and TransUnion). Make sure all the information is correct and up-to-date. If anything is wrong, make sure you get it corrected as soon as possible. You should also:

Find more advice in our guide 11 Tips to improve your credit score for a mortgage.

KEY INFORMATION

When you’re taking out a first time buyer mortgage, don’t just focus on what you can afford now – it’s vital to consider how you’d cope financially if your circumstances change due to illness or injury.

Our research, in partnership with LifeSearch, found:

So think carefully about what cover you need. You can find more information in our guides Income protection insurance explained, Critical illness cover, and How does life insurance work?

Find the right life cover. Search the UK’s leading insurers using the service provided by LifeSearch

Yes it is possible but getting a Buy to Let mortgage as a first time buyer can be more difficult than getting a standard mortgage. Buy to Let mortgages require a bigger deposit and are typically more expensive than residential mortgages. You can get an idea of how much you could borrow with our Buy to Let mortgage calculator.

For decades, most homeowners in the UK have had a 25-year term on their mortgage. However, longer-term mortgages of 30 years or more are becoming increasingly popular. Research from Uswitch found 51% of mortgage borrowers chose a term of 30 years or longer in 2023.

Taking out a 30 year mortgage term or longer so you can stretch repayments over a longer period will lower the monthly cost of your mortgage. By doing so, your mortgage will cost more in total as you will pay more in interest over the period of your mortgage. Read more in our guide on 30 year mortgages.

Documents you’ll need to provide in the mortgage application process may include:

You might also need to show your outgoings, including how much you’re borrowing on credit cards and other loans and general living costs such as travel, childcare and entertainment.

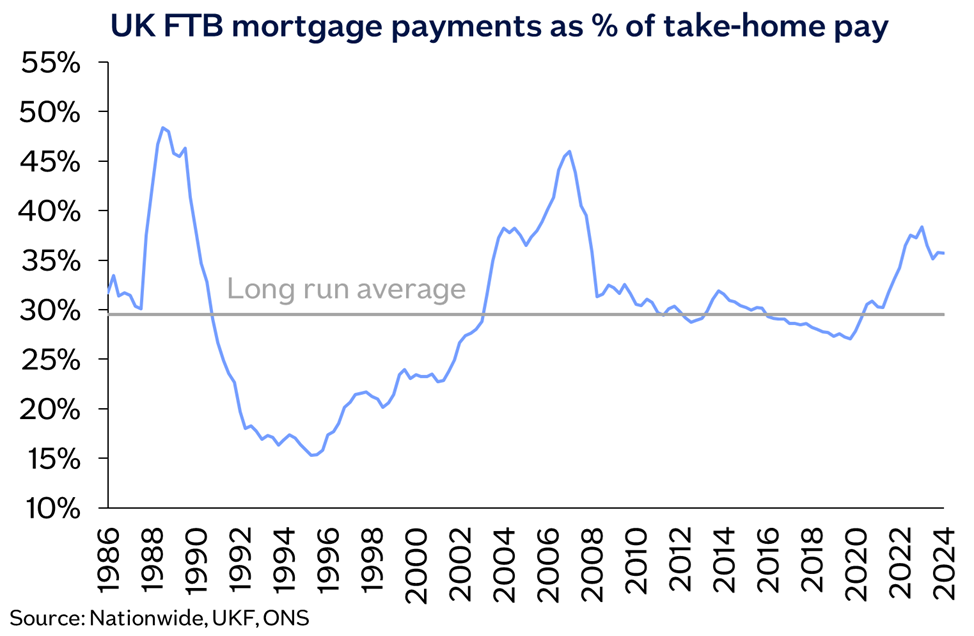

According to Nationwide’s affordability report, a prospective buyer earning the average UK income and buying a typical first-time buyer property with a 20% deposit would have a monthly mortgage payment equivalent to 36% of their take-home pay – well above the long-run average of 30%.

The property cost and any fees on first time buyer mortgages are not the only costs of buying a house. There are quite a few extras to be aware of when you are budgeting how much you can afford.

Cover for conveyancing, mortgage and survey costs, should your property purchase fall through.

If your child wants to buy their first home, there are a number of ways you can help them do it.

Get fee-free mortgage advice from the award-winning expert advisers at Mortgage Advice Bureau.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Please note some branches of Mortgage Advice Bureau may charge a fee for mortgage advice if you go direct. The fee is up to 1% but a typical fee is 0.3% of the amount borrowed. So make sure you use this site, this form or phone number for fee-free advice.

If you’re a first time buyer, you’re exempt from paying any stamp duty in England and Northern Ireland providing the property costs less than £425,000. However, due to stamp duty changes this threshold is being lowered to £300,000 from 1 April 2025.

Many first time buyers choose fixed rate mortgages because they offer security in terms of how much mortgage payments will be each month. The most common are 2 or 5 year fixed rate mortgages. Other first time buyers opt for tracker or discounted mortgages, in the hope they’ll be cheaper over time.

However, the best mortgage depends on your personal circumstances. The award-winning expert advisers at Mortgage Advice Bureau will find the right mortgage for you. For more information, also read our guide Types of Mortgages Explained & How to Choose the Right One.

Getting mortgage advice for first time buyers at the start of the process is advisable because you’ll know from the outset what your likely budget will be and understand your options. For more information, read our guide Do I need a mortgage broker? What they do, costs, and when to use one.

You’ll usually need at least a 5% deposit, there are unless you’re taking out a 100% mortgage.

If you’re looking for mortgage advice for first time buyers, it’s a good idea to speak to an expert mortgage adviser.

While you can apply for a mortgage in principle before you start house hunting, you can only apply for mortgage once you’ve had an offer accepted on a property. Read more in our guide When to apply for a mortgage.

The term LTV stands for loan-to-value, and tells you what percentage of the home’s value is borrowed. For example, if you buy a £100,000 house and you pay £20,000 as the deposit, your LTV is 80% because you’ve already paid 20% when you put down the deposit and borrowed the remaining 80. If you were to pay £5,000 deposit, your LTV would be 95%. Generally speaking, higher LTVs lead to higher interest rates, because they are seen as riskier for lenders.

Yes. As long as you can get a mortgage that’s affordable and you’re able to buy a house you can afford, it may be a good time to get a first time buyer mortgage. In fact, 341,068 first time buyers got on the property ladder in 2024, according to Halifax.

HomeOwners Alliance Ltd is registered in England, company number 07861605. Information provided on HomeOwners Alliance is not intended as a recommendation or financial advice.

HomeOwners Alliance Ltd is an Introducer Appointed Representative of Mortgage Advice Bureau (Derby) Limited which is authorised and regulated by the Financial Conduct Authority.

HomeOwners Alliance Ltd is an Introducer Appointed Representative (IAR) of LifeSearch Limited, an Appointed Representative of LifeSearch Partners Ltd, authorised and regulated by the Financial Conduct Authority. (FRN: 656479).

Independent Financial Adviser service is provided by Unbiased, who match you to a fully regulated, independent financial adviser, with no charge to you for the referral.

HomeOwners Alliance Ltd is an Introducer Appointed Representative (IAR) of Fluent Money Limited, which is authorised and regulated by the Financial Conduct Authority. Calls may be monitored/recorded.

If you take out a mortgage or protection product through Mortgage Advice Bureau, they pay us a referral fee of 25%. You are not obliged to use their services.

{kind=link}