Find the best estate agent near you Start here

Saving a deposit for a house is one of the biggest hurdles for first-time buyers, so it's no surprise that gifted deposits are a common feature of buying a home. Find out what gifted deposits are, how they work and the legal and tax implications

House prices are at such a high level that the average deposit required by first-time buyers has increased significantly over the years. According to Halifax, the average deposit first time buyers paid in 2024 was £61,090. For many people, saving this amount of money is unachievable. Which is why so many aspiring homeowners look for financial help, in the form of gifted deposits, to help boost their savings and get a step on the property ladder.

A “gifted deposit” refers to money given to a homebuyer to help them buy a property. The amount of money gifted can be a contribution towards the deposit or equate to the whole deposit. However, it’s not as straight-forward as a parent simply transferring the money into a child’s account and saying it’s a gift. There are a number of factors to consider which we outline below.

In terms of how much deposit you need to buy a house, a deposit of 5% is usually the minimum a mortgage lender will require, although it is possible to buy a house with a smaller or even no deposit.

But having a bigger deposit means:

So even if you have saved enough for a deposit to buy your first home, you may benefit from a gifted deposit top-up. For example, if you have a 25% deposit, rather than a 10% deposit, your mortgage payments will be more affordable.

Gifted deposits are just that – gifted. Unlike a loan, they are given with the understanding that the money doesn’t need to be repaid. The person gifting the money has no rights or legal interest in the property being purchased.

Get fee-free mortgage advice from the award-winning expert advisers at Mortgage Advice Bureau.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Please note some branches of Mortgage Advice Bureau may charge a fee for mortgage advice if you go direct. The fee is up to 1% but a typical fee is 0.3% of the amount borrowed. So make sure you use this site, this form or phone number for fee-free advice.

Most mortgage lenders prefer it if the person gifting you the money is an immediate relative, such as a parent, grandparent or sibling. You can also receive a gifted deposit from a partner. But more distant relatives such as aunts and uncles, or friends, may not be allowed. Some lenders’ lending criteria may state it must be a parent who gifts the money.

Most lenders won’t accept a gifted deposit if the person giving the money is the vendor – the person selling the house. It may seem like an unlikely prospect but it could be a problem if you’re buying a house from your parents or another family member.

If you’re expecting a gifted deposit, it’s a good idea to speak to a broker as they will know what different lender rules apply.

The best mortgage depends on your personal circumstances. The award-winning expert advisers at Mortgage Advice Bureau will find the right mortgage for you.

You will also need to inform your conveyancing solicitor that you are buying with a gifted deposit.

Yes, you must declare any gifts you use for your deposit to your mortgage. To avoid additional undisclosed debt, lenders need to ensure the money is a gift, not a loan. The person gifting the money may also need to provide bank statements to show the origin of the funds, as part of anti-money laundering checks.

If you receive a gifted deposit, your lender may require whoever is gifting you the money to sign a ‘Gifted Deposit Letter’. This will need to include:

Bigger banks and building societies will usually have a gifted deposit declaration form that can be filled out. But smaller lenders may request a signed and certified letter. However, if you’re unsure about your letter, it’s a good idea to speak to your mortgage broker who’ll be able to advise you.

Want to buy a home with a gifted deposit? Get fee-free advice from the award-winning expert advisers at Mortgage Advice Bureau.

The person gifting you the deposit will also need to provide:

Mortgage lenders view gifted deposits and loaned deposits as completely different things. A bank may accept a loaned deposit, provided there’s a signed declaration that it will only need to be repaid when the property is sold. If that’s not the case, they will view the loan as a financial commitment, like a credit card. So it will factor in the planned repayments when assessing the buyer’s affordability.

There is no limit on how large a gifted deposit you receive can be, unless a lender stipulates this.

In the UK, gifted deposits are generally tax-free. Everyone is allowed to give away up to £3000 per year, exempt from inheritance tax. Any unused allowance can be carried over from the previous year. However, for larger gifts or if the gifter doesn’t have the full annual inheritance tax allowance and passes away within seven years of the gift, it may be subject to inheritance tax. It’s always advisable to consult an Independent Financial Adviser for tailored advice.

To find out more, read our guide How to keep on top of inheritance tax

Absolutely. The bigger the deposit you can raise, the more affordable your repayments will be and the greater the range of mortgages you’ll usually have access to. As mentioned above, you may get access to better rates too, especially if you can save enough to get to a threshold, such as a 15%, 20% or 25% deposit.

Get fee-free mortgage advice from the award-winning expert advisers at Mortgage Advice Bureau.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Please note some branches of Mortgage Advice Bureau may charge a fee for mortgage advice if you go direct. The fee is up to 1% but a typical fee is 0.3% of the amount borrowed. So make sure you use this site, this form or phone number for fee-free advice.

If you’re gifting your child a deposit and they’re buying a property with their partner or buying with friends, you can protect the money you have gifted in the event they split up with a declaration of trust, or deed of trust. This can be drawn up by the conveyancing solicitor working on the property purchase. It will state who the money was given to – this allows you to specify that you gifted it to your child and not to them and their partner. So if the couple split up, it will make sure your child keeps ownership of the money you gifted.

It can also clarify whether the money is a gift or a loan. And if it’s a loan, when it needs to be paid back. A deed of trust can also be used by the people buying the property to set out responsibilities for outgoings and what will happen to the property if they break up. However, if your child goes on to marry the person they bought the home with this could affect the deed of trust.

Some homeowners choose to use equity release to allow them to unlock cash from their home for a gift. But this can be an expensive commitment and you should consider it carefully, taking independent financial advice. The same can be said for anyone considering accessing money from their savings or pension to gift to a child.

If your parents or family want to help you but can’t afford to gift you money, there may still be ways they can help you, particularly if you are trying to get a mortgage with no deposit. Such as:

Get fee-free mortgage advice from the award-winning expert advisers at Mortgage Advice Bureau.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Please note some branches of Mortgage Advice Bureau may charge a fee for mortgage advice if you go direct. The fee is up to 1% but a typical fee is 0.3% of the amount borrowed. So make sure you use this site, this form or phone number for fee-free advice.

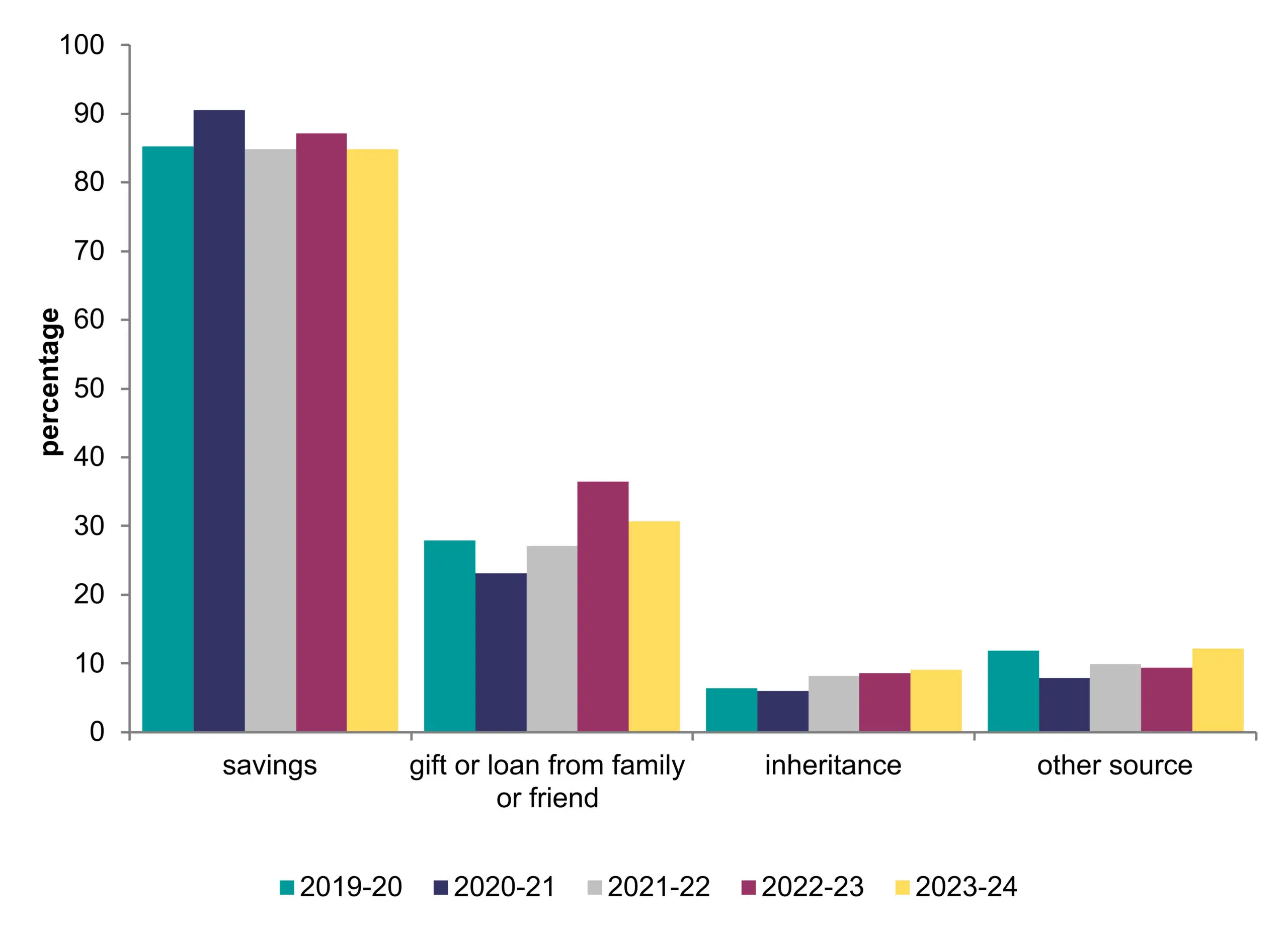

It seems not everyone is lucky enough or perhaps wants to accept financial help. According to the English Housing Survey 2023-2024, most first time buyers (85%) funded the purchase of their first home with savings, but 31% reported receiving help from family or friends while 9% used an inheritance as a source of deposit.

The graph below shows the source of deposit for recent first time buyers in 2019-2020, 2020-2021, 2022-2023 and 2023-2024.

Base: all recent first time buyers

Notes:

1) more than one answer could be given

2) underlying data are presented in Annex Table 2.1

Source: English Housing Survey, full household sample

No. Lenders can rule out gifted deposits.

During the height of the COVID-19 pandemic, when the economic climate was uncertain and lenders became very risk averse, some lenders restricted the use of gifted deposits. For example, Nationwide launched a 90% LTV mortgage, and stipulated that buyers would need to prove at least 75% of their deposit came from their own savings. This capped the amount of money buyers could use from gifted deposits. But Nationwide has since relaxed its rules. And gifted deposits are now widely accepted again by lenders. However, as lenders’ lending criteria is subject to change, it’s always a wise move to speak to a mortgage broker to get the most up-to-date information.

HomeOwners Alliance Ltd is registered in England, company number 07861605. Information provided on HomeOwners Alliance is not intended as a recommendation or financial advice.

HomeOwners Alliance Ltd is an Introducer Appointed Representative of Mortgage Advice Bureau (Derby) Limited which is authorised and regulated by the Financial Conduct Authority.

HomeOwners Alliance Ltd is an Introducer Appointed Representative (IAR) of LifeSearch Limited, an Appointed Representative of LifeSearch Partners Ltd, authorised and regulated by the Financial Conduct Authority. (FRN: 656479).

Independent Financial Adviser service is provided by Unbiased, who match you to a fully regulated, independent financial adviser, with no charge to you for the referral.

HomeOwners Alliance Ltd is an Introducer Appointed Representative (IAR) of Fluent Money Limited, which is authorised and regulated by the Financial Conduct Authority. Calls may be monitored/recorded.

If you take out a mortgage or protection product through Mortgage Advice Bureau, they pay us a referral fee of 25%. You are not obliged to use their services.