Find the best estate agent near you Start here

There are many types of mortgages in the UK, and choosing the right one can affect both your monthly payments and the total you repay. This guide explains how the main mortgage types work and how to choose the right one for you.

KEY INFORMATION

Here are the main types of mortgages to choose from:

When you’re taking out a mortgage, one of the biggest decisions is whether to take out a fixed rate or a variable rate mortgage. So it’s vital that you understand the difference between these types of mortgages so that you can pick the right one for you.

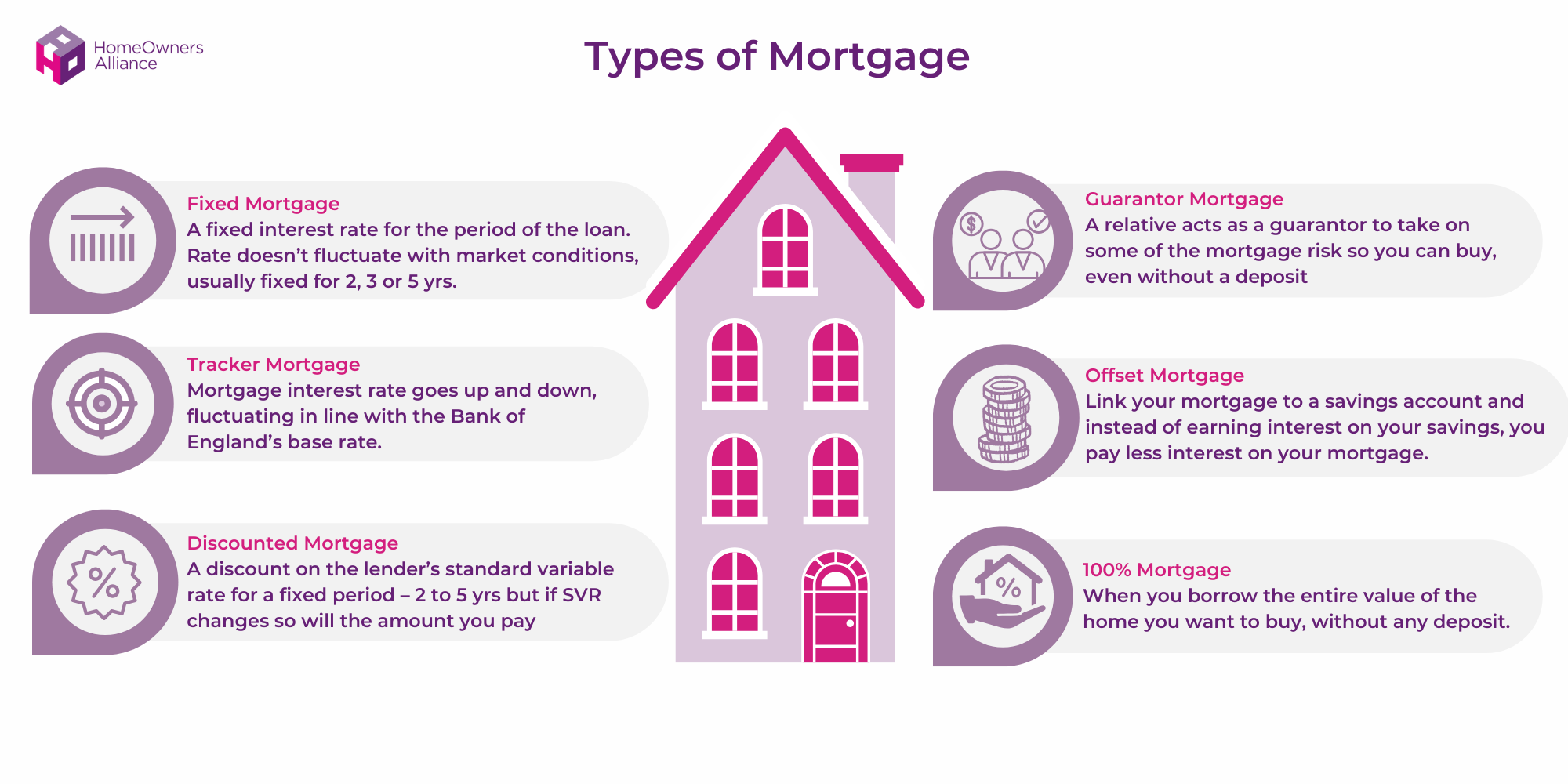

A fixed rate mortgage is a home loan where the interest rate and monthly payments stay the same for a set period, usually 2, 3, 5 or 10 years.

Fixed rate mortgages are a popular option, because you know exactly what your monthly repayments will look like over a set period.

However, while the rate you’ll pay won’t go up during your term it won’t go down either. Read more in our guide Fixed rate mortgages: pros & cons, latest rates and how to apply.

To consider whether to fix for a shorter or longer period of time, see our guide: 2 or 5 year fixed rate mortgage.

Get fee-free mortgage advice from the award-winning expert advisers at Mortgage Advice Bureau.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Please note some branches of Mortgage Advice Bureau may charge a fee for mortgage advice if you go direct. The fee is up to 1% but a typical fee is 0.3% of the amount borrowed. So make sure you use this site, this form or phone number for fee-free advice.

Variable rate mortgages are different to fixed rate mortgages because the rate you pay can go up or down. There are three main types of variable rate mortgages and they each work in different ways.

If you take out a tracker mortgage, the rate you pay goes up and down in line with the Bank of England’s base rate.

Tracker mortgages usually last for between two to five years, after which the rates revert to the lender’s standard variable rate, which can be much more expensive.

Read more in our guide Tracker mortgages explained.

Unlike tracker mortgages, which track the Bank of England base rate, with this type of mortgage, the rate you’ll pay is linked to the lender’s standard variable rate.

A standard variable rate mortgage is the type of variable rate mortgage you’ll usually be moved to when your fixed rate, tracker or discounted mortgage deal ends.

If your current mortgage deal ends in the next six months, start investigating your remortgage options ASAP, to reduce the chance of rolling onto your lender’s SVR when your current deal ends.

However, everyone’s circumstances are different. So the best way to find out if staying on your lender’s SVR is right for you is to speak to a mortgage broker.

Get fee-free mortgage advice from the award-winning expert advisers at Mortgage Advice Bureau.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Please note some branches of Mortgage Advice Bureau may charge a fee for mortgage advice if you go direct. The fee is up to 1% but a typical fee is 0.3% of the amount borrowed. So make sure you use this site, this form or phone number for fee-free advice.

Whether you take out a fixed or variable rate mortgage, you’ll usually take it out for 2, 3 or 5 years, however some 7 and 10 year terms (or even longer) are available.

You’ll need to weigh up how long you’ll want to be tied into your deal for.

You’ll also need to decide whether you want to take out a repayment mortgage or an interest-only mortgage.

Here is how these mortgage types work:

Get fee-free mortgage advice from the award-winning expert advisers at Mortgage Advice Bureau.

The types of mortgages available for you will depend on your circumstances, including what type of buyer (or remortgager) you are.

You may have a number of different types of mortgages available to you if you’re a first time buyer. These may let you:

Read more in our guide to First time buyer mortgages.

This is the type of mortgage (or remortgage) for people taking out a loan on a property they will live in.

If you take out a residential mortgage, you can’t usually let the property out unless you have consent from your lender.

You’ll usually need at least a 5% deposit to take out a residential mortgage, although you can get a mortgage with a smaller, or even no deposit.

This is the most common reason for getting a mortgage in the UK.

Buy to Let mortgages are the type of mortgage landlords take out if they’re buying or remortgaging a property that will be let out to tenants.

Buy to Let mortgages are similar to residential mortgages but there are some key differences:

This type of mortgage is also designed for people who are letting out a property but they work differently because Let to Buy involves renting out your current home and buying a new one to live in:

This allows you to keep your original property as an investment, with the aim of earning rental income and benefiting from any increase in property value.

Let to Buy can be a popular option with couples wanting to move in together, but each have their own property. In this case, you could both move into one of the properties and rent the other one out using a Let to Buy mortgage.

Not sure whether to sell up or rent out? Read our guide on when letting a property makes sense

Get fee-free mortgage advice from the award-winning expert advisers at Mortgage Advice Bureau.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Please note some branches of Mortgage Advice Bureau may charge a fee for mortgage advice if you go direct. The fee is up to 1% but a typical fee is 0.3% of the amount borrowed. So make sure you use this site, this form or phone number for fee-free advice.

An offset mortgage is a type of mortgage that allows you to use your savings to reduce the amount of interest you pay on your mortgage.

However, these mortgages may have higher interest rates. Find out more about offset mortgages, the pros and cons and how they work.

Guarantor mortgages are a type of mortgage that allow a relative to act as a guarantor, using either savings or their own property as security.

You can usually borrow a larger amount than you would be able to on your own. In fact some guarantor mortgages will let you borrow 100% of the property’s value.

Find more information on how guarantor mortgages work, the risks and popular options such as Barclays Family Springboard.

Green mortgages reward you for saving energy in your property.

Get FEE-FREE expert advice on green mortgages from Mortgage Advice Bureau.

| Mortgage types | Pros | Cons |

|---|---|---|

| Fixed rate mortgage | Repayments won’t go up. Easier to budget. Removes uncertainty. | Rates won’t go down if base rate falls. High fees to leave deal early. |

| Tracker mortgage | Rate could go down. Rates are transparent & go up and down in line with base rate. Some deals come with no fee if you leave early. | Repayments can increase. |

| Standard variable rate mortgage | May be suitable for some people. | More expensive. Lenders can charge what they want. Repayments can change at any time. |

| Offset mortgage | You can use savings to lower your interest repayments. More flexible. | You won’t earn interest on your savings. Rates may be slightly higher. |

| First time buyer mortgage | May be able to borrow more based on income. Available for lower or even no deposit. | |

| Guarantor mortgage | You can borrow larger amounts. | You need a guarantor and they face significant risks. |

| Green mortgage | You may get a cheaper rate or cashback. | Only available on certain properties. May not be the best deal for you. |

The most common mortgage term length has traditionally been 25 years, however the average length of mortgage for first time buyers has increased in recent years.

In fact, the number of borrowers taking out ultra-long mortgages of more than 35 years has tripled since 2020, according to Thisismoney.co.uk.

Some people prefer taking a mortgage out over a longer term because it can make repayments more affordable, however, it also means you’ll pay more interest over the life of your mortgage.

See our guide on 30 year mortgages to help you weigh up the pros and cons of a longer mortgage term.

The easiest way to find the best mortgage for you is to speak to a mortgage broker. They’ll discuss your personal circumstances, help you understand the different types of mortgages available and find the best mortgage for you.

Get fee-free mortgage advice from the award-winning expert advisers at Mortgage Advice Bureau.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Please note some branches of Mortgage Advice Bureau may charge a fee for mortgage advice if you go direct. The fee is up to 1% but a typical fee is 0.3% of the amount borrowed. So make sure you use this site, this form or phone number for fee-free advice.

The main types of mortgages in the UK are fixed rate, tracker, discount and standard variable rate mortgages.

With a repayment mortgage, you pay back both the loan and the interest each month, so the mortgage is fully paid off at the end of the term. With an interest-only mortgage, you only pay the interest, meaning you must repay the original loan separately.

Some people prefer a fixed rate mortgage because it gives certainty, as your payments stay the same for a set period. However, others prefer variable rate mortgages. Which is better for you depends on your circumstances.

Generally speaking, most first time buyers can choose from the same types of mortgages as existing homeowners, although interest-only mortgages may be less common. Also, some deals are specifically designed for first time buyers, often with smaller deposit requirements.

However, the types of mortgages you’ll be able to access will depend on your circumstances so it’s a good idea to get fee-free mortgage advice.

HomeOwners Alliance Ltd is registered in England, company number 07861605. Information provided on HomeOwners Alliance is not intended as a recommendation or financial advice.

HomeOwners Alliance Ltd is an Introducer Appointed Representative of Mortgage Advice Bureau (Derby) Limited which is authorised and regulated by the Financial Conduct Authority.

HomeOwners Alliance Ltd is an Introducer Appointed Representative (IAR) of LifeSearch Limited, an Appointed Representative of LifeSearch Partners Ltd, authorised and regulated by the Financial Conduct Authority. (FRN: 656479).

Independent Financial Adviser service is provided by Unbiased, who match you to a fully regulated, independent financial adviser, with no charge to you for the referral.

HomeOwners Alliance Ltd is an Introducer Appointed Representative (IAR) of Fluent Money Limited, which is authorised and regulated by the Financial Conduct Authority. Calls may be monitored/recorded.