Find the best estate agent near you Start here

For first time buyers the prospect of getting on the property ladder feels overwhelming and out of reach. Here we simplify the steps you need to take to get started and demystify the process of buying a first home.

Right now buying a first home might feel out of reach. In fact, our research found the challenges facing first time buyers top the list of housing concerns among UK adults in 2025. These include getting on the ladder (81%), house prices (81%) and saving a deposit (79%).

But there are small things you can do to get started. Here we simplify the essential first steps and set out what you need to do and what help you can access when buying your first home.

Buying a first home starts with saving a deposit. In terms of how much deposit you need to buy a house, normally you need a minimum 5% deposit of the value of the property you want to buy. So if you want to buy a home costing £250,000, you’ll need to save up a deposit of at least £12,500. Although it is possible to buy a house with a smaller or even no deposit.

Ideally though, when buying a first home you would save more than 5%. The bigger the deposit, the wider range of mortgages you’ll typically be able to access and typically at lower rates too. This is because with a bigger deposit you’re perceived as lower risk by mortgage lenders.

The average first time buyer deposit in 2024 was £61,090, according to Halifax and the average deposit size was 20%. First time buyers in London face a particular challenge because of the inherently high house prices and deposits required. The average first time buyer paid £511,514 for a house in London in 2024, putting down an average deposit of £124,688.

It’s a good idea to get an idea of house prices in the area you are looking to buy. See our monthly House Price Index report and our guide to the cheapest places to buy in the UK. Being a first time buyer in London

The good news is you can get help from government to boost your deposit when you’re buying a first home. With a Lifetime ISA, you can save up to £4,000 a year – and the government will add a 25% bonus, up to a maximum of £1,000 annually. This is first on the list on our guide to buying a first home as the sooner you start saving, the bigger the bonus you’ll be able to get. Restrictions on using the cash apply though, find out more with our Best Lifetime ISA guide.

Get fee-free mortgage advice from the award-winning expert advisers at Mortgage Advice Bureau.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Please note some branches of Mortgage Advice Bureau may charge a fee for mortgage advice if you go direct. The fee is up to 1% but a typical fee is 0.3% of the amount borrowed. So make sure you use this site, this form or phone number for fee-free advice.

While you‘re planning on buying a first home, you can start sprucing up your credit rating ready for when you make a mortgage application. Lenders want to see you are a reliable borrower when they are assessing your mortgage application, so it helps to have a good credit score. Read our full guide to find out how to improve your credit rating.

How much you can borrow when buying a first home will be determined by your lender who will do an affordability test based on your income and monthly outgoings. It can be a really good idea, therefore, to go through your current account six months before you make a mortgage application and see for yourself where all your money is going.

If you have an expensive gym membership, regular big nights out or expensive credit agreements try to cancel them and curtail your spending so that your finances look in better shape when the lender starts looking.

When you’re buying a first home, you’ll want to know how much you’ll be able to borrow on a mortgage. Our How much can I borrow calculator will give you an idea based on your income.

Next, it’s a good idea to get a Mortgage in Principle, which is a statement from a lender or mortgage broker confirming how much you may be able to borrow, based on your circumstances. It isn’t a guaranteed mortgage offer, but it can strengthen your position when viewing properties or making an offer.

You should be able to get a mortgage in principle for free. With our partners at Mortgage Advice Bureau, you can get a personalised Decision in Principle today. Getting a Decision in Principle from Mortgage Advice Bureau won’t impact your credit score. There’s no obligation to proceed with the deal they find you, but it gives you a good indication of how much you can borrow.

Getting expert mortgage advice is important because it’s not just the mortgage rate you need to consider, any mortgage fees can make a big difference to the overall cost of buying your first home too.

You’ll also need to decide on the type of mortgage, whether fixed or variable, and the term of the mortgage.

Mortgage brokers will also know about new mortgage products like 100% mortgages, Deposit Unlock or Green mortgages and can discuss the pros and cons of these.

Get fee-free mortgage advice from the award-winning expert advisers at Mortgage Advice Bureau.

First time buyers buying a home up to £300,000 in England and Northern Ireland do not have to pay any stamp duty.

When buying your first home, if your new property is worth £300,001 to £500,000 you’ll pay 5% stamp duty, but only on the value above £300,000. You’ll pay normal stamp duty rates if the property costs over £500,000. Different rules apply in Scotland and Wales. Find out more in our guide on First time buyer stamp duty.

When buying a first home, you’ll find it involves a lot of additional costs that you’ll need to factor in when working out what you can afford.

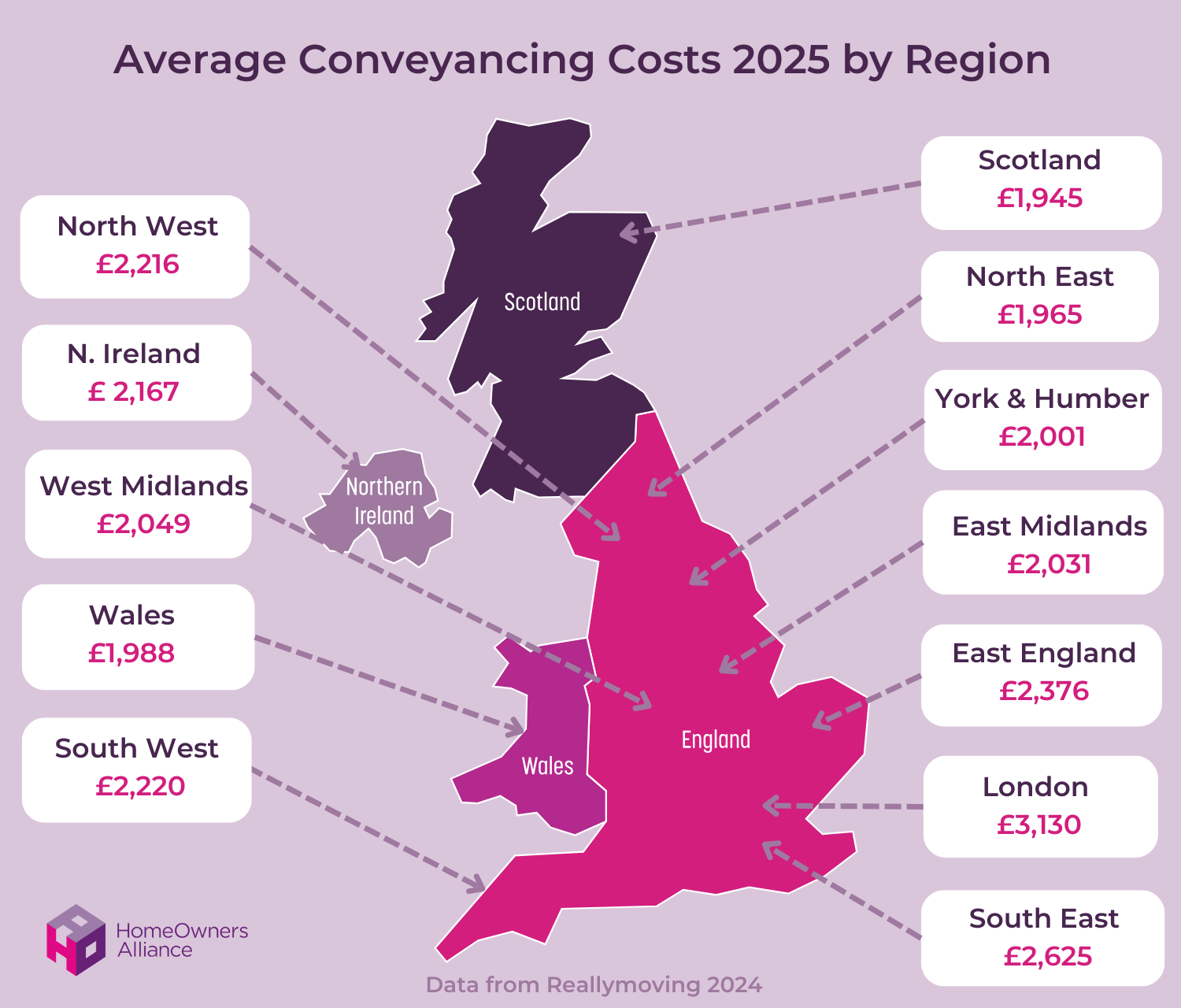

So do your research carefully and cut costs where you can including by shopping around for the best deals on conveyancing fees, survey costs and removals.

Once you own your first home, you’ll discover there are also a lot of costs involved in running it that you may never have had to deal with before. These may include ground rent, service charges, ongoing maintenance costs and utilities.

Understand the full range of costs involved with our guide on the cost of buying and owning a home. See our cost of moving calculator to help you estimate the costs.

It’s a good time to review your finances generally — an independent financial adviser may be a help in reaching your goals. When reviewing your financial plans, it is sensible to think about life insurance cover.

Your family may be able to help you in a number of ways when buying a first home. The Bank of Mum and Dad is now considered the seventh biggest lender in the UK mortgage market because so many parents are helping their children with a gifted deposit on their first home.

But when it comes to how to buy a first home, family can also help without having to hand over their savings. Many mortgage lenders now offer products aimed at people whose family want to help them buy their first home. It could be a joint mortgage where you buy a place with your parents. Alternatively, you could get a family offset mortgage where a family member puts their savings into an account that is used to reduce your mortgage costs.

Get fee-free mortgage advice from the award-winning expert advisers at Mortgage Advice Bureau.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Please note some branches of Mortgage Advice Bureau may charge a fee for mortgage advice if you go direct. The fee is up to 1% but a typical fee is 0.3% of the amount borrowed. So make sure you use this site, this form or phone number for fee-free advice.

Another way to make buying your first home easier is to only buy part of it. Shared ownership schemes are offered by housing associations and private developers who allow you to buy a proportion of a property and then pay rent on the remainder. You then have the option to buy more of the property when you can afford to.

But make sure you do your research and tread carefully with shared ownership properties. The properties are usually leasehold and you therefore have to pay a monthly service charge as well as contribute to major maintenance works. The process of buying more shares can also be quite complicated so make sure you understand the process and costs involved before you buy.

The Mortgage Guarantee Scheme, is a government backed scheme which lets you get a mortgage with just a 5% deposit. However, its purpose is to stimulate lenders to offer 95% LTV deals, so the scheme isn’t something you specifically apply for and you may not know if your lender is using it.

Not all lenders use the mortgage guarantee scheme when offering 95% mortgages. So don’t assume choosing a lender that is taking part in the mortgage guarantee scheme will be the best option for you. You should always speak to a mortgage broker.

In June 2021, the government launched the First Homes Scheme. The First Homes scheme works by offering newly built homes to first time buyers with a discount of at least 30% compared to the market value of equivalent properties. This discount stays on the First Home forever. This means that, every time the property is sold, the new buyer benefits from the discount. The scheme has extremely limited availability, so competition is high and the scheme is not as accessible to all first time buyers in all regions. The scheme was due to end in September 2023.

You can discover more including eligibility criteria and the pros and cons in our guide on the First Homes scheme.

With the end of the government’s Help to Buy scheme in 2023, house builders developed “Deposit Unlock” so that first time buyers and home movers could buy a new build home with just a 5% deposit from a participating house builder using a mortgage offered by a participating lender. There are pros and cons to the scheme and you can find out more in our guide Deposit Unlock explained.

Other government schemes include Help to Build, Rent to Buy and Right to Buy. The best way to buy a first home will depend on your circumstances. Find more information in our guide on Government home buying schemes.

Get fee-free mortgage advice from the award-winning expert advisers at Mortgage Advice Bureau.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Please note some branches of Mortgage Advice Bureau may charge a fee for mortgage advice if you go direct. The fee is up to 1% but a typical fee is 0.3% of the amount borrowed. So make sure you use this site, this form or phone number for fee-free advice.

When you’re buying a first home, knowing the difference between freehold and leasehold is crucial. In a nutshell, if you own the freehold, it means that you own the building and the land it stands on outright. Whereas leasehold means that you just have a lease from the freeholder (sometimes called the landlord) to use the home for a number of years. Find more information in our guide Leasehold vs Freehold – what’s the difference?

The term LTV stands for loan-to-value ratio, and tells you what percentage of the home’s value is borrowed. So if you buy a £100,000 house and pay a £20,000, your LTV is 80% because you’ve already paid 20% and borrowed the remaining 80%. You can work out your loan to value with our calculator.

Depending on the type of mortgage you choose, how much the house costs, and your personal circumstances including your income and outgoings, it may be possible to buy a house with a £10k deposit in the UK. Find helpful advice in our guide How much can you afford to borrow on a mortgage?

To find out whether you can buy a house with a £10k deposit, based on your personal circumstances, it’s a good idea to speak to an expert mortgage adviser.

It’s possible to buy a house with no deposit. For example, some lenders offer 100% mortgages. However, whether you’re eligible for these mortgages and whether it’s right for you will depend on your circumstances. So it’s a good idea to get fee-free expert advice from the Mortgage Advice Bureau.

Buying a house takes an average of 5 months from when your offer is accepted, according to government figures. But how long it takes to buy a house can vary a lot in the UK. If you’re a first time buyer and buying a property that is chain-free you should expect the buying process to be quicker. With no chain, it can be as little as 4 weeks if there are no mortgage, survey or conveyancing hold-ups.

HomeOwners Alliance Ltd is registered in England, company number 07861605. Information provided on HomeOwners Alliance is not intended as a recommendation or financial advice.

HomeOwners Alliance Ltd is an Introducer Appointed Representative of Mortgage Advice Bureau (Derby) Limited which is authorised and regulated by the Financial Conduct Authority.

HomeOwners Alliance Ltd is an Introducer Appointed Representative (IAR) of LifeSearch Limited, an Appointed Representative of LifeSearch Partners Ltd, authorised and regulated by the Financial Conduct Authority. (FRN: 656479).

Independent Financial Adviser service is provided by Unbiased, who match you to a fully regulated, independent financial adviser, with no charge to you for the referral.

HomeOwners Alliance Ltd is an Introducer Appointed Representative (IAR) of Fluent Money Limited, which is authorised and regulated by the Financial Conduct Authority. Calls may be monitored/recorded.

If you take out a mortgage or protection product through Mortgage Advice Bureau, they pay us a referral fee of 25%. You are not obliged to use their services.

{kind=link}