Find the best estate agent near you Start here

Buying a house? Find out how much you can afford to borrow without over-stretching yourself and what percentage of income should go to your mortgage.

KEY INFORMATION

A common rule of thumb is that no more than 28% of your gross income should go to your mortgage.

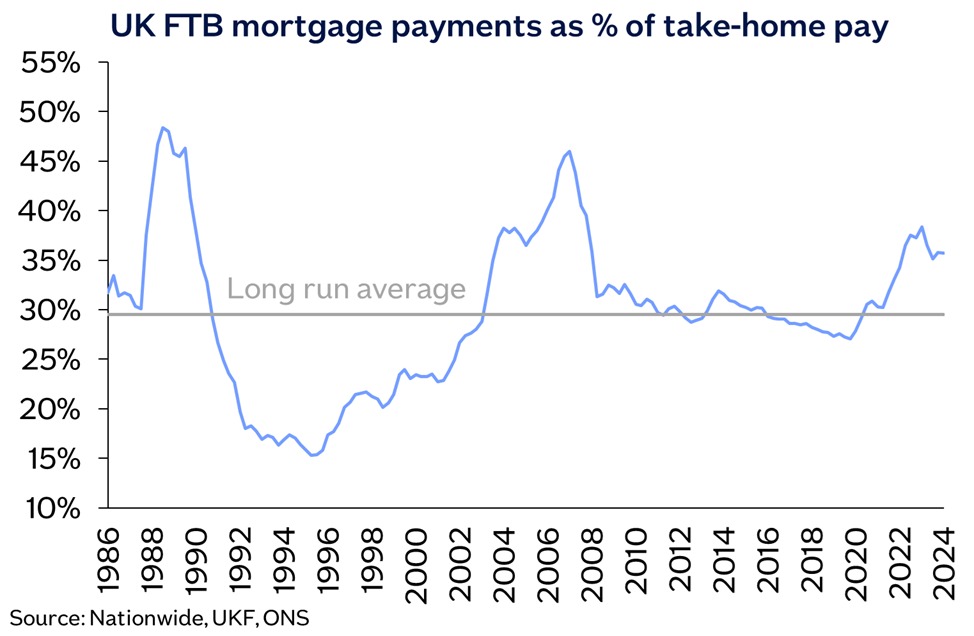

However, there’s no simple answer to this that applies to everyone. Also, many people spend a much higher proportion than this on their mortgage. Research by Nationwide in 2024 found that the average first time buyers spent around 37% of their take-home pay on mortgage payments.

Others choose to spend less so they have more money available each month for savings, bills and other living costs.

Lenders usually let you borrow up to 5 times your salary – although some lend as much as 6 times – or even higher in some cases.

Use this mortgage affordability calculator (which calculates lending based on 5x your salary) to get an idea of how much you might be able to borrow:

But lenders must also assess the monthly payment you can afford, after considering your outgoings as well as your income. This is called an affordability assessment.

The best mortgage depends on your personal circumstances. The award-winning expert advisers at Mortgage Advice Bureau will find the right mortgage for you.

Get fee-free mortgage advice from the award-winning expert advisers at Mortgage Advice Bureau.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Please note some branches of Mortgage Advice Bureau may charge a fee for mortgage advice if you go direct. The fee is up to 1% but a typical fee is 0.3% of the amount borrowed. So make sure you use this site, this form or phone number for fee-free advice.

When you apply for a mortgage, the lender will look at your personal circumstances when assessing how much you can afford to borrow on a mortgage, including:

Lenders will also consider your debt-to-income ratio, which is your monthly debt repayments (mortgage, loans, credit cards etc) compared to your gross monthly salary. To get this figure you divide your monthly debt payments by your gross monthly income and multiply by 100.

Get fee-free mortgage advice from the award-winning expert advisers at Mortgage Advice Bureau.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Please note some branches of Mortgage Advice Bureau may charge a fee for mortgage advice if you go direct. The fee is up to 1% but a typical fee is 0.3% of the amount borrowed. So make sure you use this site, this form or phone number for fee-free advice.

You’ll often come across different mortgage affordability rules online. These are general budgeting guides, not the rules mortgage lenders use when deciding how much they’ll lend.

The 28/36 rule is a budgeting guideline suggesting that no more than 28% of your gross monthly income goes towards mortgage payments and no more than 36% goes towards all debt repayments combined.

However, your debt-to-income ratio is more nuanced than this. Jump to more information on this.

And as we explain above, there’s no such thing as a one size fits all rule when it comes to mortgages. What’s right for you will depend on your circumstances.

This rule works in a similar way but says your mortgage payment limit should be 35% of your gross monthly income or 45% of your net monthly income.

The best mortgage depends on your personal circumstances. The award-winning expert advisers at Mortgage Advice Bureau will find the right mortgage for you.

While lenders have their own methods of working out how much they’ll lend you, you’ll also need to figure out how much you feel you can afford on a mortgage.

Here are some of the key factors to consider when working out your ideal mortgage to income ratio:

Mortgage calculators are a good place to start to see how much you can afford to borrow. Our mortgage affordability calculator shows you instantly how much you may be able to borrow and afford based on your income. While our mortgage cost calculator will give you an idea of what your monthly mortgage costs are likely to be.

When you take out a mortgage, there are other costs to pay too, including:

These include the mortgage fees for taking out the loan such as arrangement fees and a mortgage valuation.

| Mortgage Fees | How much you may typically pay |

| Arrangement fee | Up to £1,500 |

| Booking fee | Up to £250 |

| Mortgage valuation fee | Up to £300 |

| Telegraphic transfer fee | £25 to £50 |

| Mortgage account fee | £100 to £300 |

| Mortgage broker fee | £0- £1,000s |

| Early repayment charge | 1% to 5% |

| Exit fee | £75 to £300 |

Read more in our guide Mortgage fees explained:

Get fee-free mortgage advice from the award-winning expert advisers at Mortgage Advice Bureau.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Please note some branches of Mortgage Advice Bureau may charge a fee for mortgage advice if you go direct. The fee is up to 1% but a typical fee is 0.3% of the amount borrowed. So make sure you use this site, this form or phone number for fee-free advice.

There are other costs involved with buying a house that you need to make sure you can afford including:

You’ll usually need at least a 5% deposit to get a mortgage, although you can get mortgages with a smaller or even no deposit.

However, the bigger the deposit you have, the bigger the choice of mortgages you will typically have and you’ll usually get access to better first time buyer mortgage rates too.

Saving a house deposit is one of the biggest hurdles many first time buyers face. The size of deposit you’ll be able to save depends on:

Once you’ve added these amounts together, you need to deduct any costs of buying a home, moving and renovating, as well as any savings safety-net you want to keep.

The final sum is the amount you have available as a deposit that you can put down towards the cost of your home. Read more in our guide How much deposit do I need to buy a house.

Here are the steps you need to take to get a mortgage:

Timeline: 30 minutes

A mortgage in principle, sometimes called an agreement in principle (AiP) or decision in principle (DiP), is a statement from a lender on how much they would lend you ‘in principle’ based on information you have provided about your income and outgoings.

You should get a mortgage in principle as early in the house-buying process as possible, ideally before you start house-hunting. This is because you can show the mortgage in principle to estate agents to show you’re a serious buyer.

You should be able to get a mortgage in principle for free. With our partners at Mortgage Advice Bureau, you can get a personalised Decision in Principle today. Getting a Decision in Principle from Mortgage Advice Bureau won’t impact your credit score. There’s no obligation to proceed with the deal they find you, but it gives you a good indication of how much you can borrow.

Arrange a Mortgage Decision in Principle today with the mortgage experts at Mortgage Advice Bureau

Timeline: 20 minutes+

Once you’ve found a property and had an offer accepted, you can start the formal mortgage application process. This stage is much faster if you use a mortgage broker as they’ll do the mortgage application for you.

When you apply for a mortgage, you’ll need to provide documents including bank statements and proof of earnings. If you’re employed, you’ll usually need to show your recent payslips and your P60. While if you’re getting a self-employed mortgage, you’ll usually need your last two years’ SA302 tax calculations and your tax year overviews for those years too.

The best mortgage depends on your personal circumstances. The award-winning expert advisers at Mortgage Advice Bureau will find the right mortgage for you.

Get fee-free mortgage advice from the award-winning expert advisers at Mortgage Advice Bureau.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Please note some branches of Mortgage Advice Bureau may charge a fee for mortgage advice if you go direct. The fee is up to 1% but a typical fee is 0.3% of the amount borrowed. So make sure you use this site, this form or phone number for fee-free advice.

Timeline: 2-4 weeks

It can take 2-4 weeks to get a mortgage offer once you’ve made your full mortgage application, providing your application is relatively straightforward.

During this time there are a number of stages that will happen before the mortgage offer can be approved:

Delays could be caused if the lender is particularly busy or if you haven’t submitted the right paperwork. It can also take longer to get a mortgage offer for other reasons, including if you’re self-employed or have a poor credit score.

You’ll need to sign the contract with your lender. Your conveyancer will then continue the legal work to get you ready to exchange contracts. At this point a completion date should be set and your conveyancer will liaise with your lender to release the funds to buy the house. Read more about the conveyancing process in our guide Conveyancing timeline: How long does it take?

There are lots of reasons why your mortgage application may have been rejected, such as having a poor credit history, your employment history or too much debt.

If your application has been rejected, we advise speaking to a mortgage broker.

Brokers know the market and know what lending criteria different firms have. This means they can match you to the right lender for your personal circumstances. A broker can also help you assess your previous application and try to work out where you went wrong. Read more in our guide Mortgage declined: Here’s what to do next

Get fee-free mortgage advice from the award-winning expert advisers at Mortgage Advice Bureau.

Mortgage Advice Bureau search over 100 lenders so you don’t have to.

Get fee-free mortgage advice from the award-winning expert advisers at Mortgage Advice Bureau.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Please note some branches of Mortgage Advice Bureau may charge a fee for mortgage advice if you go direct. The fee is up to 1% but a typical fee is 0.3% of the amount borrowed. So make sure you use this site, this form or phone number for fee-free advice.

The amount of your income that should go on a mortgage will vary depending on circumstances. If your outgoings are low and you’re happy to take on the risk of a larger amount of debt, you may be happy taking out the biggest mortgage a lender offers you.

Alternatively, you may prefer to be more cautious in the amount you borrow to keep your mortgage payments lower.

See our mortgage cost calculator to see how much your mortgage could cost each month and to check that the cost of your mortgage is affordable for you.

If you have bad credit you may need a bigger deposit and you may not be able to borrow as much. But this will depend on your circumstances including what your credit issues were and how recent they were. Find out more in our guide on Bad credit mortgages. Also, it’s a good idea to get expert mortgage advice.

Lenders generally offer up to 5 times your annual salary, so if you earn £50,000, you may be able to borrow up to £250,000 on a mortgage. However, some lenders may offer more.

If you’re buying with someone else their income will also be taken into account. Our mortgage affordability calculator lets you see instantly how much you might be able to borrow based on your income.

However, don’t assume that the maximum income multiples the lender offers is what you’ll get. The lender will carry out its own affordability assessment of you when deciding whether and how much to lend.

To get a clearer idea of how much you may be able to borrow based on your salary it’s a good idea to get expert mortgage advice.

House prices increased on average 3.8% in 2024. House prices are expected to rise gradually in 2026. Find out more in our House price forecast and see our guide to the cheapest places to buy a house now in the UK.

One mortgage affordability rule of thumb in the UK is that your monthly mortgage payment should be no more than 28% of your gross monthly income.

But this is a very rough guide. The right amount for you will depend on your personal circumstances.

Ways to lower your mortgage payments include remortgaging if you’re on the Standard Variable Rate, extending your mortgage term, or switching to an interest-only mortgage. What’s right for you will depend on your circumstances. Find out more in our guide 10 ways to lower mortgage payments.

Homeowners with mortgages in England paid approximately 18.7% of their income on their mortgage in 2024, according to research by Statista. By comparison, private renters in the UK paid an average of 34% of their income on rent.

HomeOwners Alliance Ltd is registered in England, company number 07861605. Information provided on HomeOwners Alliance is not intended as a recommendation or financial advice.

HomeOwners Alliance Ltd is an Introducer Appointed Representative of Mortgage Advice Bureau (Derby) Limited which is authorised and regulated by the Financial Conduct Authority.

HomeOwners Alliance Ltd is an Introducer Appointed Representative (IAR) of LifeSearch Limited, an Appointed Representative of LifeSearch Partners Ltd, authorised and regulated by the Financial Conduct Authority. (FRN: 656479).

Independent Financial Adviser service is provided by Unbiased, who match you to a fully regulated, independent financial adviser, with no charge to you for the referral.

HomeOwners Alliance Ltd is an Introducer Appointed Representative (IAR) of Fluent Money Limited, which is authorised and regulated by the Financial Conduct Authority. Calls may be monitored/recorded.

If you take out a mortgage or protection product through Mortgage Advice Bureau, they pay us a referral fee of 25%. You are not obliged to use their services.