Find the best estate agent near you Start here

Spray foam roof insulation has become a popular way of increasing the energy efficiency of our homes. It's been promoted by industry and supported by government grants. But it now appears that homes with spray foam could face problems getting a mortgage. Alert to growing consumer concern, rogue removal companies are targeting homeowners and risk causing further damage and expense. Here's what you need to know and what you should do if your home has spray foam roof insulation.

“I’m attending a meeting with Ministers in March 2026 and we need to hear more about your experiences with spray foam roof insulation and getting a mortgage.

Please do let us know how it has affected you and give your thoughts in the comments section at the end. The more evidence we have of this problem, the harder it is for the government, lenders and manufacturers to ignore the need for action.

Thank you”

As we warm our homes, most heat is lost through our walls, windows and roofs. So it makes sense to stop heat escaping, to improve energy efficiency and spend less on heating bills. This is where spray foam roof insulation comes in: it is a chemical product containing two materials which when combined expand up to 30-60 times its liquid volume, filling every nook and cranny. It’s one way to provide extra insulation and warmth.

Spray foam insulation is promoted by the government as one of the energy efficient home improvements that are VAT-free, as a way of encouraging consumers to invest in energy efficient measures. And some households may be eligible for free or low-cost spray foam insulation as part of the Great British Insulation Scheme which is expected to run until March 2026. Spray foam insulation was also on the list of approved measures for the government’s Green Homes Grant (closed in March 2021).

And so while spray foam roof insulation has been around for 30 years, it has become more popular in the last decade thanks to these schemes and the drive for more energy efficient homes. In fact, according to the Property Care Association there may be as many as 250,000 homes with spray foam roof insulation in the loft.

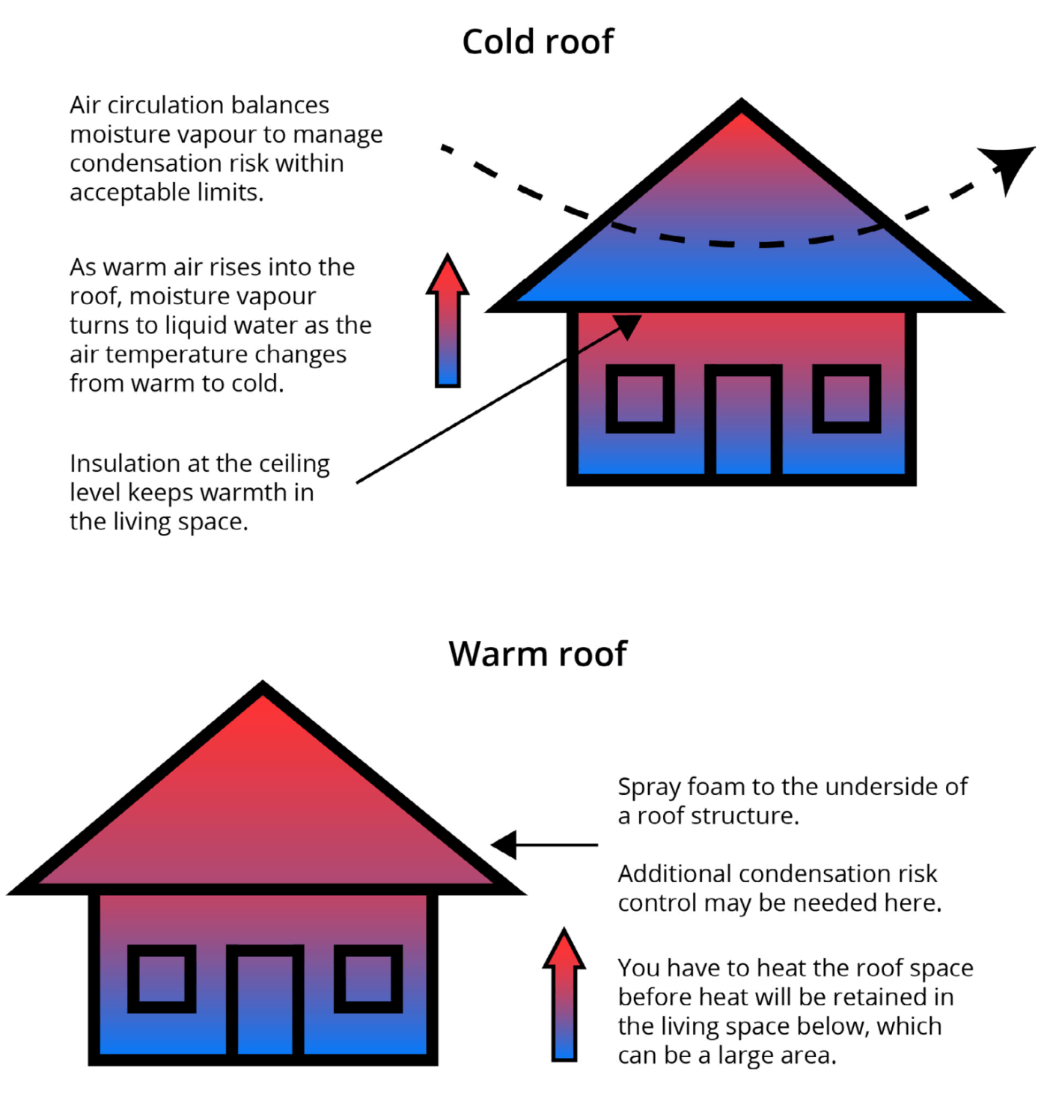

Firstly, there are two types of spray foam roof insulation and it’s important to know the difference:

There are however a few problems with spray foam insulation:

But the problems don’t end there. The increased media attention over spray foam insulation and subsequent consumer concern has led to an increase in homeowners being targeted by dodgy spray-foam removal firms and legal firms wanting to pursue cases of mis-selling.

Estate agents, surveyors and other property professionals are also increasingly likely to raise concerns if you have spray foam, with some estate agents refusing to list properties with the insulation installed.

We have also been told that these problems are tipping into the new build market where spray foam insulation legitimately installed when the homes were built are making prospective buyers worry, even though in these instances there is often no cause for concern. The same is happening with modern fully compliant loft conversions.

KEY INFORMATION

Our advice is don’t panic. If you have had spray foam in the roof for some years and have not experienced any issues, and you are not planning to sell your home in the near future, there is unlikely to be a good reason to get it removed at this stage. It is unlikely to be causing any problems.

Removing the roof insulation will mean a significant cost to you and could cause further damage to your roof so should be seen as a last resort.

If you are selling your home, dig out the paperwork. Read on for advice on your options – though sadly this isn’t straightforward.

If you are worried about the condition of your spray foam insulation, you should first get in touch with the spray foam installer. If the installer is not helpful, then contact the manufacturer. You can also get a spray foam evaluation specialist to take a look. (Jump to more on this)

You may find yourself targeted by cold callers offering to remove your spray foam insulation. It is likely that they have acquired your details illegally. Do not engage with them and report them to your local trading standards office if you are concerned.

Lenders are alert to the issues with spray foam roof insulation. As a result, spray foam roof insulation is one of many factors that can throw up a red flag to a mortgage lender. In fact, a quarter of the UK’s biggest mortgage providers will not lend against homes with spray foam in the roof, BBC research suggests.

The following video reports on the BBC investigation which we worked on with Lora Jones.

For a lender, your insulation matters because it affects important factors such as the home’s saleable value and energy efficiency rating. As valuers appointed by mortgage lenders are finding spray foam roof insulation in lofts they are having to report it. And even if it is well applied, because of its very nature it is very hard to assess the condition of the roof above the insulating foam. This means most surveyors recommend that further investigation is needed. But instead of investigating further, many mortgage lenders simply put these types of properties into a “too difficult” box and refuse to lend unless the spray foam roof insulation is removed.

Homeowners therefore may have difficulty selling to someone who needs a mortgage. See below the list of lenders who are willing to lend. Where homebuyers can secure a mortgage, they are likely to ask for the insulation to be removed at a cost to the seller or for the seller to reduce the sale price. Homeowners may find that they are limited to selling to cash buyers.

While your buyer may struggle to get a mortgage, lenders are telling us it’s not impossible.

The Residential Property Surveyors Association (RPSA) and Property Care Association, published an inspection protocol in March 2023 to help surveyors when they are inspecting spray foam as part of a mortgage valuation or building survey. These inspection guidelines should help surveyors and lenders accurately assess the risk that could be caused to a roof due to poorly installed or inappropriate use of spray foam.

We are seeing some lenders take a slightly more open approach recently – but it varies by lender.

For example:

This list is subject to change. In contrast, the BBC’s research found that TSB Bank, Skipton Building Society, Co-operative Bank, Principality and equity release lender Aviva said they did not lend against properties where spray foam is found in the roof space. While the Yorkshire Building Society and Metro Bank said they wouldn’t usually lend where there is a significant amount of spray foam.

If you are looking to sell your home, get advice from a mortgage broker and explain you have spray foam insulation. They should be able to tell you which lenders are comfortable with spray foam insulation and what other lenders require as next steps. You should pass this information onto any prospective buyers at an early stage so as not to waste yours or their time and money.

KEY INFORMATION

The “correct paperwork” being requested by lenders seems to differ from lender to lender.

It’s also worth noting that getting a specialist surveyor to check over the paperwork and thoroughly inspect the roof and structure for signs of damage could cost between £500 – £700.

If you don’t have any paperwork from the original installation, you may be able to get more information and even a free health check if you contact your original installer and/or manufacturer.

Currently there are no equity release lenders that will lend on a property if you have had spray foam roof insulation installed after the property was built. Equity release lenders are more risk-averse because they may end up having full ownership of the property years down the line.

However, we understand the company Responsible Lending will issue equity release on properties providing the foam was installed during construction. While equity release provider More 2 Life told the BBC it will only lend on properties with spray foam where it was fitted as part of an authorised new build and has the necessary documentation.

Many lending institutions, surveyors and property professionals, are rightly concerned about the risks of defects that can occur as a result of poorly or inappropriately installed sprayed foam.

Yes, you can remove spray foam roof insulation but it’s likely to cost thousands of pounds, more than the cost of the initial installation, and you may need to replace the entire roof.

So start by getting an independent assessment of your spray foam first. A spray foam evaluation specialist will provide you with a report detailing what action you need to take, or provide reassurance that it can stay without long-term risk.

If the report recommends that your spray foam roof insulation needs removing, they may be able to recommend a trusted specialist who can undertake the work for you.

Removal of open cell foam is easier as it comes away from timbers, underlay and ties more easily. Closed cell foam is more dense, has strong adhesive qualities and is rigid, making it more difficult to remove without causing damage to your roof covering. As closed cell foam was generally applied to old rotten roofs there is little advantage to removing it as it has probably given the roof some extra life and will need replacing.

Homeowners may also need to deal with the consequences in the event that the spray foam insulation was poorly installed – such as structural damage and rotting.

Whether this is right for you will depend on your circumstances. For example if your spray foam is fine in situ as far as you can tell and you want to sell your home and have the right paperwork, you should not need to remove it.

But if you do want to remove it, as with all building work, it’s important to find a reputable company to remove the spray foam.

Use our Find a Property Care Specialist tool to find spray foam evaluation experts near you today.

In the absence of a trade association or standards for removing spray foam, we are unable to recommend removal companies.

However, if you use a spray foam evaluation specialist (make sure they’re a member of the Property Care Association), they may be able to recommend a trusted expert who can remove your spray foam.

If you have concerns about your spray foam, you should first get in touch with the spray foam installer. If the installer is not helpful, then contact the manufacturer.

There are six certified (BBA or KIWA Agreement) manufacturers and distributors in the UK:

If you are unsure of who the manufacturer is, you can contact the Insulation Manufacturers Association and they should be able to help. Each manufacturer should be able to provide information about your installation and may even send out a surveyor to independently inspect the property for free.

As we mentioned above there have been a worrying increase in the number of scam and cold-calling cases. If this happens to you, think about how they obtained your information and how they know that you have spray foam. It is likely that they have acquired your details illegally or may even be linked to the original installation company. Do not engage with them and report them to your local trading standards office if you are worried.

This depends on factors like location, access and how much needs to be removed. But experts say it’s likely to cost more than installation. That’s because it gets into all the crevices and the gaps behind timbers making it difficult to get to and get rid of it. Also bear in mind that damage to your home may already have been done.

According to Checkatrade, the cost of removing spray foam insulation can cost around £40 per square metre but you also need to factor in the cost of the skips as well as the safe disposal of the insulation.

One of our readers who is buying a property with open cell spray foam has received quotes to remove the foam for £17,000 when the original installation cost £12,000. Although she is a cash buyer, she hopes to take advantage of equity release in the future.

Read the comments below for more homeowner experiences and feel free to add your thoughts.

This situation with spray foam insulation is very concerning for homeowners – but also very confusing. Has it been fitted correctly? Has the right type been used? Do you have the right paperwork? What paperwork is that exactly? There are so many variables and the advice on what to do is sadly not straightforward.

It is known that some spray foam installers employ sales agents to generate leads and they use pushy sales and social media post tactics. Often, these sales teams carry out the initial survey which is supposed to be undertaken by a properly trained surveyor and then use high pressure sales techniques to close the sale and get the work done as fast as possible. We are very critical of these practices and yet the major parties in the industry have not enough to discourage this activity. Whilst we support the manufacturers coming together to support those with spray foam, much more needs to be done to improve how spray foam is being marketed.

We are calling on the industry to ensure health warnings about the risks to your property and getting a mortgage are added to foam installation company guidelines, websites and marketing material. We also ask that they do not work with any firm employing direct sales and they should adopt an ethical code which should include:

Our CEO, Paula Higgins, was on the ITV Tonight programme in early December 2025, highlighting the growing spray foam roof insulation crisis. The case study featured on the programme, Cathy, came directly from us. She visited our site and shared her experience, helping to highlight the real impact this issue is having on homeowners.

![]() Watch Paula and hear her advice on ITV

Watch Paula and hear her advice on ITV

We are also urging government to step in and help solve the spray foam insulation mortgage problems, high removal costs facing homeowners, and set out the best approach to removal. You can read about our joint letter with the Property Care Association to Ministers here.

And until this is done, we recommend homeowners do not install spray foam insulation.

If you or a loved one have been misled or bullied into getting spray foam roof installation, highlighting the problem in the media or by reporting it to Trading Standards via Citizens Advice may yield results.

For example in June 2025, the director of a home insulation company who encouraged his sales staff to “systematically” bully and lie to vulnerable customers was jailed for six and a half years.

John Beckett, whose businesses were investigated by the BBC’s Rip Off Britain programme in 2018, was found guilty at Bournemouth Crown Court of two counts of fraudulent trading.

Det Insp Jamie Halford, of Dorset Police, said: “Our investigation found that Beckett was operating two corrupt and fraudulent businesses.

“He encouraged his sales staff to persistently and systematically lie in order to deceive, mislead and bully customers who were known to be vulnerable in order to make as much money as possible.

“The work of Beckett’s companies had a lasting effect on some victims, who encountered difficulties when trying to sell their properties due to the spray foam that was installed when it was not required.” Find out more about the case here.

If you’re buying a property, you should ask your surveyor to check for it in the loft and if present, you’ll want to think carefully about next steps. Flag it with your conveyancer as part of the buying process so that they can ensure they obtain copies of the right guarantees and paperwork.

Get instant house survey quotes from qualified surveyors in your area.

But the presence of spray foam roof insulation is likely to cause problems for you getting a mortgage.

Our Mortgage Expert Sarah Tucker notes that, “Mortgage lenders are becoming more familiar with spray foam insulation, but there is still no consistent approach across the market. Having the right paperwork, including installation certificates, warranties and details of who carried out the work, can help reassure lenders and surveyors. However, buyers may still find they have fewer mortgage options available, which can make a sale more difficult.”

It’s worth noting that if the foam has been used to help stabilise a roof in need of repair this will usually mean the mortgage application will be declined.

Buying a house with spray foam roof insulation? Get fee-free mortgage advice from the award-winning expert advisers at Mortgage Advice Bureau.

Get fee-free mortgage advice from the award-winning expert advisers at Mortgage Advice Bureau.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Please note some branches of Mortgage Advice Bureau may charge a fee for mortgage advice if you go direct. The fee is up to 1% but a typical fee is 0.3% of the amount borrowed. So make sure you use this site, this form or phone number for fee-free advice.

If you are keen to proceed with the purchase regardless of spray foam insulation, you could ask the seller to remove the insulation or get a quote for removal yourself and ask them to drop the price so that you can pay for the removal after moving in. Although there may be damage underneath the foam that also needs rectifying. Get advice from your surveyor.

For most homes, it may be more cost effective and efficient to insulate the floor of the roof space rather than insulating the roof itself. See our guide to loft insulation costs.

The Residential Property Surveyors Association suggests that for most homeowners putting 300mm of fibre insulation on the floor of their loft will provide the same thermal performance as spray foam, but at a fraction of the cost and with minimal risk of causing damage. There are also potential risks to using spray foam to older roofs with no underfelt or have the black bitumen underfelt where there is not suitable ventilation.

In fact, you may find roof spray foam has the opposite effect if you are looking to make your living space warmer as you will now be heating your loft space as well. Of course, this could be considered an advantage to some homes, especially if you are storing valuable belongings in the loft or have solar panels or other machinery that needs to be kept at a more constant temperature all year round.

RICS has published a guide for those wanting to install spray foam roof insulation which highlights some of the complexities involved with installing it correctly.

If you want to make your home more energy efficient we recommend you research all the various ways to do this to find the approach suitable for your type of home and budget. Our guide on How to make your home more energy efficient is a good place to start.

Please share your experience with spray foam insulation in the comments below. Your views will help strengthen our campaign for better regulation and compensation.

Thank you to the Property Care Association, RICS and Geoff Hunt, Property Mentoring for their contributions.

HomeOwners Alliance Ltd is registered in England, company number 07861605. Information provided on HomeOwners Alliance is not intended as a recommendation or financial advice.

HomeOwners Alliance Ltd is an Introducer Appointed Representative of Mortgage Advice Bureau (Derby) Limited which is authorised and regulated by the Financial Conduct Authority.

HomeOwners Alliance Ltd is an Introducer Appointed Representative (IAR) of LifeSearch Limited, an Appointed Representative of LifeSearch Partners Ltd, authorised and regulated by the Financial Conduct Authority. (FRN: 656479).

Independent Financial Adviser service is provided by Unbiased, who match you to a fully regulated, independent financial adviser, with no charge to you for the referral.

Bridging Loan and specialist lending service provided by Chartwell Funding Limited, registered office 5 Badminton Court, Station Road, Yate, Bristol, BS37 5HZ, authorised and regulated by the Financial Conduct Authority (FRN: 458223). Your property may be repossessed if you do not keep up repayments on a mortgage or any debt secured on it.