Find the best estate agent near you Start here

Buying your first home? Read on for news about the best first time buyer mortgage rates for every deposit size, from 0% upwards.

We know things are hard for first time buyers in 2026 – so we want to make things easier. Every month we showcase the best deals for you, with input from the award-winning mortgage experts at L&C, who have given fee-free mortgage advice to over 2 million people.

Here’s an overview of the current best first time buyer mortgage rates for a number of deposit levels for 2 and 5 year fixed rate mortgages and 2 year tracker mortgages. Read on for the best mortgage rates for more deposit sizes and mortgage types.

| Loan-to-value | 2 year fixed rate (+fee) | 5 year fixed rate (+fee) | 2 year tracker (+fee) |

|---|---|---|---|

| 95% LTV |

5.50% (£499)

|

5.35% (£0)

|

4.74% (£999)

|

| 90% LTV |

5.15% (£999)

|

5.04% (£1,499)

|

4.38% (£999)

|

| 75% LTV |

4.77% (£1,499)

|

4.79% (£995)

|

3.98% (£999)

|

| 60% LTV |

4.71% (£999)

|

4.77% (£995)

|

3.96% (£1,599)

|

Here are this month’s best first time buyer mortgage rates if you’ve got a 40% deposit and want a fixed deal. This table shows the rates, any fees you’ll have to pay and the monthly cost of borrowing £200,000 over 30 years.

| Lender | Initial Rate | Fees | Monthly payment | APRC | Annual Cost | Max LTV |

|---|---|---|---|---|---|---|

| Nationwide | 4.71% | £999 | £1,038 | 6.2% | £12,961 | 60% |

| Natwest | 4.75% | £1,495 | £1,043 | 6.4% | £13,267 | 60% |

| Yorkshire BS | 4.76% | £995 | £1,045 | 6.4% | £13,032 | 60% |

| Natwest | 4.80% | £995 | £1,049 | 6.4% | £13,089 | 60% |

| Principality | 4.80% | £1,499 | £1,049 | 6.4% | £13,341 | 65% |

| Lender | Initial Rate | Fees | Monthly payment | APRC | Annual Cost | Max LTV |

|---|---|---|---|---|---|---|

| Yorkshire BS | 4.77% | £995 | £1,046 | 6.0% | £12,748 | 60% |

| Yorkshire BS | 4.79% | £995 | £1,048 | 6.0% | £12,776 | 75% |

| Yorkshire BS | 4.79% | £995 | £1,048 | 6.0% | £12,776 | 60% |

| Yorkshire BS | 4.81% | £995 | £1,051 | 6.0% | £12,805 | 75% |

| Yorkshire BS | 4.83% | £995 | £1,053 | 6.0% | £12,835 | 80% |

If you’ve got a 25% deposit, here are the best first time buyer mortgage rates available this month. This table shows the rates, any fees you’ll have to pay and the monthly cost of borrowing £200,000 over 30 years.

| Lender | Initial Rate | Fees | Monthly payment | APRC | Annual Cost | Max LTV |

|---|---|---|---|---|---|---|

| Yorkshire BS | 4.82% | £995 | £1,052 | 6.4% | £13,119 | 75% |

| Nationwide | 4.82% | £999 | £1,052 | 6.2% | £13,121 | 75% |

| Yorkshire BS | 4.87% | £995 | £1,058 | 6.4% | £13,191 | 75% |

| Nationwide | 4.88% | £999 | £1,059 | 6.2% | £13,208 | 80% |

| Nationwide | 4.88% | £999 | £1,059 | 6.2% | £13,208 | 85% |

| Lender | Initial Rate | Fees | Monthly payment | APRC | Annual Cost | Max LTV |

|---|---|---|---|---|---|---|

| Yorkshire BS | 4.79% | £995 | £1,048 | 6.0% | £12,776 | 75% |

| Yorkshire BS | 4.81% | £995 | £1,051 | 6.0% | £12,805 | 75% |

| Yorkshire BS | 4.83% | £995 | £1,053 | 6.0% | £12,835 | 80% |

| Yorkshire BS | 4.85% | £995 | £1,055 | 6.0% | £12,864 | 85% |

| Yorkshire BS | 4.85% | £995 | £1,055 | 6.0% | £12,864 | 80% |

If you’ve got a 20% deposit and you’re looking for the best first time buyer mortgage rates, here are your options this month. This table shows the rates, any fees you’ll have to pay and the monthly cost of borrowing £200,000 over 30 years.

| Lender | Initial Rate | Fees | Monthly payment | APRC | Annual Cost | Max LTV |

|---|---|---|---|---|---|---|

| Nationwide | 4.88% | £999 | £1,059 | 6.2% | £13,208 | 80% |

| Nationwide | 4.88% | £999 | £1,059 | 6.2% | £13,208 | 85% |

| Yorkshire BS | 4.90% | £995 | £1,061 | 6.4% | £13,235 | 80% |

| Yorkshire BS | 4.90% | £995 | £1,061 | 6.4% | £13,235 | 85% |

| Leeds | 4.94% | £999 | £1,066 | 7.2% | £13,295 | 85% |

| Lender | Initial Rate | Fees | Monthly payment | APRC | Annual Cost | Max LTV |

|---|---|---|---|---|---|---|

| Yorkshire BS | 4.83% | £995 | £1,053 | 6.0% | £12,835 | 80% |

| Yorkshire BS | 4.85% | £995 | £1,055 | 6.0% | £12,864 | 85% |

| Yorkshire BS | 4.85% | £995 | £1,055 | 6.0% | £12,864 | 80% |

| Yorkshire BS | 4.87% | £995 | £1,058 | 6.0% | £12,893 | 85% |

| Accord | 4.88% | £1,495 | £1,059 | 6.0% | £13,007 | 80% |

To talk through your options, get in touch with our fee-free mortgage broker partners at L&C.

If you’ve got a 15% deposit, here are the best first time buyer mortgage rates available this month if you’re looking for a 2 or 5 year fixed rate mortgage. This table shows the rates, any fees you’ll have to pay and the monthly cost of borrowing £200,000 over 30 years.

| Lender | Initial Rate | Fees | Monthly payment | APRC | Annual Cost | Max LTV |

|---|---|---|---|---|---|---|

| Nationwide | 4.88% | £999 | £1,059 | 6.2% | £13,208 | 85% |

| Yorkshire BS | 4.90% | £995 | £1,061 | 6.4% | £13,235 | 85% |

| Leeds | 4.94% | £999 | £1,066 | 7.2% | £13,295 | 85% |

| Yorkshire BS | 4.95% | £995 | £1,068 | 6.4% | £13,308 | 85% |

| Nationwide | 4.98% | £499 | £1,071 | 6.2% | £13,104 | 85% |

| Lender | Initial Rate | Fees | Monthly payment | APRC | Annual Cost | Max LTV |

|---|---|---|---|---|---|---|

| Yorkshire BS | 4.85% | £995 | £1,055 | 6.0% | £12,864 | 85% |

| Yorkshire BS | 4.87% | £995 | £1,058 | 6.0% | £12,893 | 85% |

| Accord | 4.90% | £1,495 | £1,061 | 6.0% | £13,036 | 85% |

| Accord | 4.94% | £495 | £1,066 | 6.0% | £12,895 | 85% |

| Yorkshire BS | 4.97% | £0 | £1,070 | 6.1% | £12,840 | 85% |

If you can save a 10% deposit, you’ll usually get access to better mortgage rates than if you’ve got a smaller deposit. But you’ll usually pay more than if you can save a bigger deposit.

| Deposit % | Interest rate | Monthly mortgage cost |

| 5% | 5.35% | £1,117 |

| 10% | 4.90% | £1,061 |

| 25% | 4.64% | £1,030 |

Here are the lowest mortgage rates this month if you’ve got a 10% deposit. The monthly mortgage cost examples are based on borrowing £200,000 over a 30 year term:

| Lender | Initial Rate | Fees | Monthly payment | APRC | Annual Cost | Max LTV |

|---|---|---|---|---|---|---|

| Leeds | 5.15% | £999 | £1,092 | 7.3% | £13,604 | 90% |

| Natwest | 5.18% | £745 | £1,096 | 6.5% | £13,522 | 90% |

| Yorkshire BS | 5.20% | £995 | £1,098 | 6.5% | £13,676 | 90% |

| Halifax | 5.22% | £1,099 | £1,101 | 6.9% | £13,758 | 90% |

| Lloyds | 5.22% | £1,199 | £1,101 | 6.9% | £13,808 | 90% |

| Lender | Initial Rate | Fees | Monthly payment | APRC | Annual Cost | Max LTV |

|---|---|---|---|---|---|---|

| Barclays | 5.06% | £899 | £1,081 | 5.5% | £13,152 | 90% |

| Nationwide | 5.09% | £999 | £1,085 | 5.9% | £13,216 | 90% |

| Leeds | 5.10% | £999 | £1,086 | 6.7% | £13,231 | 90% |

| Santander | 5.10% | £749 | £1,086 | 6.0% | £13,181 | 90% |

| Santander | 5.13% | £749 | £1,090 | 6.0% | £13,225 | 90% |

If you’ve got a 5% deposit and therefore need a 95% LTV mortgage, you’ll likely pay higher rates and have less choice of lenders because lenders see these mortgages as riskier.

However, 95% mortgages are widely available, due to the mortgage guarantee scheme, which was launched to encourage lenders to offer these small deposit mortgages. Although many lenders now offer 95% mortgages without using the scheme.

So if you’ve got a 5% deposit and you’re looking at the best first time buyer mortgage rates, here are the lowest rates on 2 and 5 year fixed rate mortgages. This table shows the rates, any fees you’ll have to pay and the monthly cost of borrowing £200,000 over 30 years.

| Lender | Initial Rate | Fees | Monthly payment | APRC | Annual Cost | Max LTV |

|---|---|---|---|---|---|---|

| West Brom | 5.50% | £499 | £1,136 | 6.1% | £13,876 | 95% |

| Nationwide | 5.63% | £499 | £1,152 | 6.3% | £14,073 | 95% |

| Barclays | 5.65% | £0 | £1,154 | 5.7% | £13,854 | 95% |

| Halifax | 5.65% | £1,099 | £1,154 | 7.0% | £14,403 | 95% |

| Lloyds | 5.65% | £1,199 | £1,154 | 7.0% | £14,453 | 95% |

| Lender | Initial Rate | Fees | Monthly payment | APRC | Annual Cost | Max LTV |

|---|---|---|---|---|---|---|

| Marsden | 5.35% | £0 | £1,117 | 7.1% | £13,402 | 95% |

| Melton Mowbray | 5.40% | £199 | £1,123 | 7.0% | £13,517 | 95% |

| Barclays | 5.46% | £0 | £1,131 | 5.6% | £13,567 | 95% |

| Leek BS | 5.51% | £995 | £1,137 | 6.6% | £13,841 | 95% |

| Skipton | 5.53% | £995 | £1,139 | 6.0% | £13,871 | 95% |

It’s possible to get a mortgage with no deposit – these are known as 100% mortgages.

The best rate on a 100% mortgage this month is Skipton Building Society’s Track Record 5 year fix at 5.55% – but you’ll need to meet criteria including having a proven track record of paying rent.

There are other types of 100% mortgages available. For more details see our guide on 100% mortgages.

We’ve partnered with award-winning mortgage brokers L&C who search 90+ lenders to help find you the best mortgage. Plus, unlike other brokers, they don’t charge a fee for their service.

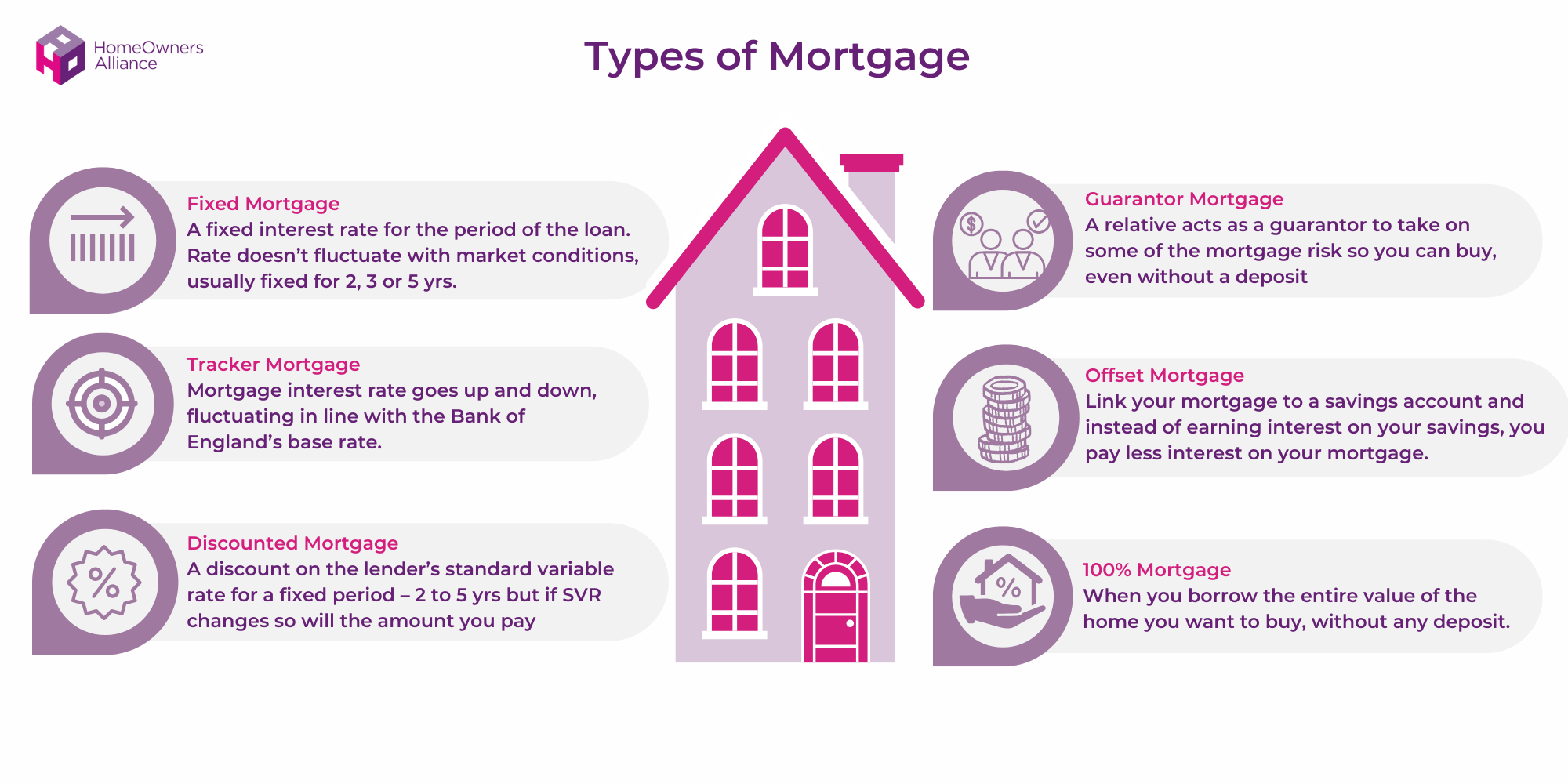

If you take out a variable rate mortgage, the amount you’ll pay on your mortgage can go up or down. This is different to a fixed rate mortgage where the rate you’ll pay remains the same during the initial term.

Here are the types of variable rate mortgages:

The main benefit of variable rate mortgages is that your mortgage payments may go down. Also, some trackers let you leave penalty-free during the term which means you could swap to a better deal if mortgage rates improve.

But if interest rates increase in the future, you’ll pay more. So make sure you get advice. For the best first time buyer mortgage rates and fee-free mortgage advice speak to our partners at L&C. Start online or give them a call today about your mortgage needs.

If you’re looking at first time buyer mortgage rates, here are the best rates on offer this month if you’re looking for a variable rate mortgage.

Just like with fixed deals, when you’re looking for a variable rate mortgage, the larger the deposit, the better the rate you can usually get. These are the best first time buyer mortgage rates this month if you have a 40% deposit.

This table shows the rates available, any fees you’ll have to pay the lender, and the monthly cost if you borrow £200,000 over 30 years. However, as these are variable rate mortgages, the rate and the amount you’ll pay may go up or down.

| Lender | Initial Rate | Fees | Monthly payment | APRC | Annual Cost | Max LTV |

|---|---|---|---|---|---|---|

| Halifax | 3.96% | £1,599 | £950 | 6.7% | £12,202 | 60% |

| Lloyds | 3.96% | £1,699 | £950 | 6.7% | £12,252 | 60% |

| Cumberland | 3.98% | £999 | £953 | 6.5% | £11,930 | 80% |

| Barclays | 4.01% | £999 | £956 | 5.4% | £11,971 | 60% |

| Lloyds | 4.08% | £1,699 | £964 | 6.7% | £12,418 | 75% |

| Lender | Initial Rate | Fees | Monthly payment | APRC | Annual Cost | Max LTV |

|---|---|---|---|---|---|---|

| Barclays | 4.35% | £999 | £996 | 5.2% | £12,147 | 60% |

| Barclays | 4.75% | £999 | £1,043 | 5.4% | £12,719 | 85% |

| Barclays | 4.85% | £1,749 | £1,055 | 5.4% | £13,014 | 75% |

| Earl Shilton | 5.14% | £1,350 | £1,091 | 6.5% | £13,360 | 75% |

| Earl Shilton | 5.19% | £125 | £1,097 | 6.5% | £13,189 | 90% |

If you’ve got a 25% deposit, here are the best first time buyer mortgage rates available this month if you’re looking for a 2 year variable rate mortgage or a 5 year variable rate mortgage.

This table shows the rates available, any fees you’ll have to pay the lender, and the monthly cost if you borrow £200,000 over 30 years. However, as these are variable rate mortgages, the rate and the amount you’ll pay may go up or down.

| Lender | Initial Rate | Fees | Monthly payment | APRC | Annual Cost | Max LTV |

|---|---|---|---|---|---|---|

| Cumberland | 3.98% | £999 | £953 | 6.5% | £11,930 | 80% |

| Halifax | 4.08% | £1,599 | £964 | 6.7% | £12,368 | 75% |

| Lloyds | 4.08% | £1,699 | £964 | 6.7% | £12,418 | 75% |

| Barclays | 4.11% | £999 | £968 | 5.5% | £12,110 | 75% |

| Lloyds | 4.13% | £1,699 | £970 | 6.7% | £12,488 | 80% |

| Lender | Initial Rate | Fees | Monthly payment | APRC | Annual Cost | Max LTV |

|---|---|---|---|---|---|---|

| Barclays | 4.75% | £999 | £1,043 | 5.4% | £12,719 | 85% |

| Barclays | 4.85% | £1,749 | £1,055 | 5.4% | £13,014 | 75% |

| Earl Shilton | 5.14% | £1,350 | £1,091 | 6.5% | £13,360 | 75% |

| Earl Shilton | 5.19% | £125 | £1,097 | 6.5% | £13,189 | 90% |

| Earl Shilton | 5.59% | £1,069 | £1,147 | 6.7% | £13,977 | 90% |

If you’ve got a 20% deposit and you’re looking for the best first time buyer mortgage rates, here are your options this month.

This table shows the rates available, any fees you’ll have to pay the lender, and the monthly cost if you borrow £200,000 over 30 years. However, as these are variable rate mortgages, the rate and the amount you’ll pay may go up or down.

| Lender | Initial Rate | Fees | Monthly payment | APRC | Annual Cost | Max LTV |

|---|---|---|---|---|---|---|

| Cumberland | 3.98% | £999 | £953 | 6.5% | £11,930 | 80% |

| Halifax | 4.13% | £1,599 | £970 | 6.7% | £12,438 | 80% |

| Lloyds | 4.13% | £1,699 | £970 | 6.7% | £12,488 | 80% |

| Nationwide | 4.24% | £999 | £983 | 6.1% | £12,292 | 80% |

| Bath BS | 4.24% | £999 | £983 | 6.7% | £12,292 | 80% |

| Lender | Initial Rate | Fees | Monthly payment | APRC | Annual Cost | Max LTV |

|---|---|---|---|---|---|---|

| Barclays | 4.75% | £999 | £1,043 | 5.4% | £12,719 | 85% |

| Earl Shilton | 5.19% | £125 | £1,097 | 6.5% | £13,189 | 90% |

| Earl Shilton | 5.59% | £1,069 | £1,147 | 6.7% | £13,977 | 90% |

| Earl Shilton | 5.94% | £1,069 | £1,191 | 6.8% | £14,511 | 90% |

If you’ve got a 15% deposit, here are the best first time buyer mortgage rates available this month if you’re looking for a 2 or 5 year variable rate mortgage.

This table shows the rates available, any fees you’ll have to pay the lender, and the monthly cost if you borrow £200,000 over 30 years. However, as these are variable rate mortgages, the rate and the amount you’ll pay may go up or down.

| Lender | Initial Rate | Fees | Monthly payment | APRC | Annual Cost | Max LTV |

|---|---|---|---|---|---|---|

| Halifax | 4.26% | £1,599 | £985 | 6.7% | £12,620 | 85% |

| Lloyds | 4.26% | £1,699 | £985 | 6.7% | £12,670 | 85% |

| Cumberland | 4.28% | £999 | £987 | 6.5% | £12,348 | 85% |

| Nationwide | 4.29% | £999 | £989 | 6.1% | £12,362 | 85% |

| Cumberland | 4.38% | £999 | £999 | 6.6% | £12,489 | 90% |

| Lender | Initial Rate | Fees | Monthly payment | APRC | Annual Cost | Max LTV |

|---|---|---|---|---|---|---|

| Barclays | 4.75% | £999 | £1,043 | 5.4% | £12,719 | 85% |

| Earl Shilton | 5.19% | £125 | £1,097 | 6.5% | £13,189 | 90% |

| Earl Shilton | 5.59% | £1,069 | £1,147 | 6.7% | £13,977 | 90% |

| Earl Shilton | 5.94% | £1,069 | £1,191 | 6.8% | £14,511 | 90% |

Meanwhile, if you’re buying a house and looking for the best first time buyer mortgage rates this month, here are the lowest mortgage rates if you’ve got a 10% deposit.

This table shows the rates available, any fees you’ll have to pay the lender, and the monthly cost if you borrow £200,000 over 30 years. However, as these are variable rate mortgages, the rate and the amount you’ll pay may go up or down.

| Lender | Initial Rate | Fees | Monthly payment | APRC | Annual Cost | Max LTV |

|---|---|---|---|---|---|---|

| Cumberland | 4.38% | £999 | £999 | 6.6% | £12,489 | 90% |

| Furness | 4.54% | £749 | £1,018 | 7.4% | £12,592 | 90% |

| Halifax | 4.57% | £1,599 | £1,022 | 6.8% | £13,060 | 90% |

| Lloyds | 4.57% | £1,699 | £1,022 | 6.8% | £13,110 | 90% |

| Nationwide | 4.69% | £999 | £1,036 | 6.2% | £12,932 | 90% |

| Lender | Initial Rate | Fees | Monthly payment | APRC | Annual Cost | Max LTV |

|---|---|---|---|---|---|---|

| Earl Shilton | 5.19% | £125 | £1,097 | 6.5% | £13,189 | 90% |

| Earl Shilton | 5.59% | £1,069 | £1,147 | 6.7% | £13,977 | 90% |

| Earl Shilton | 5.94% | £1,069 | £1,191 | 6.8% | £14,511 | 90% |

If you’ve got a 5% deposit and you’re looking at the best first time buyer mortgage rates, here are the lowest rates on 2 year variable rate mortgages.

This table shows the rates available, any fees you’ll have to pay the lender, and the monthly cost if you borrow £200,000 over 30 years. However, as these are variable rate mortgages, the rate and the amount you’ll pay may go up or down.

| Lender | Initial Rate | Fees | Monthly payment | APRC | Annual Cost | Max LTV |

|---|---|---|---|---|---|---|

| Bath BS | 4.74% | £999 | £1,042 | 6.8% | £13,005 | 95% |

| Furness | 4.84% | £-250 | £1,054 | 7.4% | £12,525 | 95% |

| Nationwide | 4.89% | £499 | £1,060 | 6.2% | £12,972 | 95% |

| Nationwide | 4.95% | £0 | £1,068 | 6.2% | £12,810 | 95% |

| Nationwide | 4.99% | £-500 | £1,072 | 6.2% | £12,619 | 95% |

Get fee free mortgage advice from our partners at L&C. Use the online mortgage finder or speak to an advisor today.

When you take out a mortgage, you don’t just need to look at best first time buyer mortgage rates, you’ll need to decide which type of mortgage to choose too.

If you take out a fixed rate mortgage, the rate you’ll pay will stay the same during the initial term. So if you take out a 2 year fixed rate mortgage, your repayments will be the same for the first 2 years.

If you take out a variable rate mortgage, the amount you’ll pay can go up and down. If you take out a tracker mortgage, the amount you’ll pay is affected by what happens to the base rate it tracks, which is usually the Bank of England base rate. If the base rate rises or falls, your mortgage rate will follow suit.

| Base rate | Mortgage rate (base rate + 0.21%) | Mortgage payment |

|---|---|---|

| 3.50% | 3.71% | £922 |

| 3.25% | 3.46% | £884 |

But while interest rates are expected to go down, this isn’t guaranteed. And if interest rates increase, so will your mortgage payments. Read more in our guide on Mortgage rate predictions.

| Base rate | Mortgage rate (base rate + 0.21%) | Mortgage payment |

|---|---|---|

| 4.00% | 4.21% | £979 |

| 4.25% | 4.46% | £1,009 |

While if you’re on a discounted variable rate, you’ll pay a rate that’s lower than the lender’s Standard Variable Rate. If your lender decides to pass on a cut in interest rates, your mortgage payments will fall. But it won’t necessarily pass on all or any of the cut.

Just like with any mortgage, if you want the best first time buyer mortgage rates, having a bigger deposit usually helps.

| Deposit | Best 2 year fixed rate | Best 5 year fixed rate |

|---|---|---|

| 40% (LTV 60%) | 4.47% | 4.62% |

| 25% (LTV 75%) | 4.64% | 4.70% |

| 20% (LTV 80%) | 4.67% | 4.83% |

| 15% (LTV 85%) | 4.73% | 4.83% |

| 10% (LTV 90%) | 4.90% | 4.93% |

| 5% (LTV 95%) | 5.35% | 5.28% |

According to Halifax, the average deposit first time buyers paid in 2024 was over £61,000. This is why so many first time buyers look for financial help.

| Cost of property | Deposit % | Deposit needed |

|---|---|---|

| £200,000 | 5% | £10,000 |

| £200,000 | 10% | £20,000 |

| £200,000 | 15% | £30,000 |

Here are some examples of how much your first time buyer mortgage will cost you each month, based on deposit size and whether you take out a fixed rate or variable rate mortgage.

Here’s a selection of practical gadgets and tools to help keep things simple.

You’re typically a first time buyer if you’ve never owned a home previously, either in the UK or abroad.

Unless you’re lucky enough to have the cash to buy your first home outright, getting a first time buyer mortgage will be essential to owning your own home. Here’s how to do it.

Get fee FREE mortgage advice from award-winning brokers L&C. Start online or speak to an expert about your mortgage needs. No hidden costs, just great service.

Here are the steps you need to take to get a first time buyer mortgage:

Timeline: Instant

A mortgage in principle, sometimes called an agreement in principle (AiP) or decision in principle (DiP), is a statement from a lender on how much they would lend you ‘in principle’ based on information you have provided about your income and outgoings.

You should get a mortgage in principle as early in the house-buying process as possible, ideally before you start house-hunting. This is because you can show the mortgage in principle to estate agents to show you’re a serious buyer.

You should be able to get a mortgage in principle for free. With our partners at L&C, you can get a personalised Decision in Principle in just a matter of minutes. And unlike some other lenders, getting a Decision in Principle from L&C won’t impact your credit score. There’s no obligation to proceed with the deal they find you, but it gives you a good indication of how much you can borrow.

Arrange a Mortgage Decision in Principle today with the mortgage experts at L&C

Timeline: 20 minutes+

Once you’ve found a property and had an offer accepted, you can start the formal mortgage application process. This stage is much faster if you use a mortgage broker as they’ll do the mortgage application for you.

When you apply for a mortgage, you’ll need to provide documents including bank statements and proof of earnings. If you’re employed, you’ll usually need to show your recent payslips and your P60. If you’re getting a self-employed mortgage, you’ll usually need your last two years’ SA302 tax calculations and your tax year overviews for those years too.

Timeline: 2-4 weeks

It can take 2-4 weeks to get a mortgage offer once you’ve made your full mortgage application, providing your application is relatively straightforward.

During this time there are a number of stages that will happen before the mortgage offer can be approved:

However, delays could be caused if the lender is particularly busy or if you haven’t submitted the right paperwork. It can also take longer to get a mortgage offer if you’re self-employed or have a poor credit score.

You’ll need to sign the contract with your lender. Your conveyancer will then continue the legal work to get you ready to exchange contracts. At this point a completion date should be set and your conveyancer will liaise with your lender to release the funds to buy the house. Read more about the conveyancing process in our guide Conveyancing timeline: How long does it take?

There are lots of reasons why your mortgage application may have been rejected such as having a poor credit history, too much debt or not being registered to vote. We always recommend you use a mortgage broker. This is especially true if you have had a mortgage application declined.

Brokers know the market and know what lending criteria every firm has. This means they can match you to the right lender for your personal circumstances. A broker can also help you assess your previous application and work out where you went wrong. Read more in our guide Mortgage declined: Here’s what to do next

When buying your first home, there are a number of schemes that can help you get on the property ladder in 2026.

| Scheme | Pros | Cons | Where can I find more information? |

|---|---|---|---|

| Lifetime ISA | These are savings accounts for people to save for their first home or their retirement. You can save up to £4,000 each tax year into your LISA and the government will give you a 25% bonus on your contributions, up to a maximum of £1,000 per year. | Can only open a Lifetime ISA if you’re aged 18-39 years old. Can’t use your LISA savings to put towards a house if it costs over £450,000. You’ll pay a penalty if you withdraw funds. | Read our guide on the Best Lifetime ISAs |

| Deposit Unlock | You can buy a new build house with a 5% deposit. | Limited mortgage lenders use the scheme. Can only buy from selected housebuilders. | Read our guide on the Deposit Unlock scheme explained |

| Shared ownership | You buy a share of a property (10%-75%) and pay rent on the rest, so you’ll need a smaller mortgage and smaller deposit than if you buy on the open market. Can increase the share you own by ‘staircasing’. | Many potential downsides including: service charges can spiral, staircasing can be expensive, limited mortgage choice. | Read more in Shared Ownership: What is it? Is it worth it? |

| First Homes Scheme | Offers newly built homes to local first time buyers, including keyworkers, with a discount of at least 30%. This discount stays on the First Home forever. | Extremely limited availability. | Read more in our guide on the First Homes scheme explained |

| Own New Rate Reducer scheme | You can buy a new build home with a mortgage and pay a lower mortgage rate than if you buy on the open market with a traditional mortgage | Limited choice of properties and lenders. Rates could rocket once your initial deal ends. Could risk overpaying for your house. | Read more in our guide Own New Rate Reducer scheme explained |

| Help to Buy Equity Loan scheme (2021-2023) | You could buy a new build home with a 5% deposit and borrow an equity loan from the government of up to 20% of the property’s value, which was interest-free for the first five years. And you’d get a mortgage for the rest. | Not available anymore. This scheme closed on 31 March 2023. | N/A |

While you can’t make a full mortgage application until you’ve had an offer accepted on a property, it’s advisable to start your mortgage research as soon as possible.

This means you’ll find out about the best first time buyer mortgage rates and be able to get a Mortgage Agreement in Principle, also known as Decision in Principle. This is a statement from a lender saying the amount it would lend you ‘in principle’ based on information you have provided and they can be useful to show to estate agents when house-hunting.

And if you still need some more time to save up your deposit before you can buy your first home, speaking to an expert mortgage broker should help you understand how far off you are from being able to get on the property ladder.

The easiest way to find the best first time buyer mortgage rates and compare them is to speak to a fee-free mortgage broker. They’ll search the market for you and find you the best first time buyer mortgage. Compare today’s best mortgage deals and speak to a fee free mortgage advisor today.

Get fee free mortgage advice from our partners at L&C. Use the online mortgage finder or speak to an advisor today.

The average first time buyer mortgage term is 31 years, according to the UK Finance Household Finance Review for Q1 2025.

Your deposit is likely to be your biggest cost when buying a house but there are other costs you’ll need to budget for when you’re buying your first home such as:

For more information, read our guide on the Costs of buying a house.

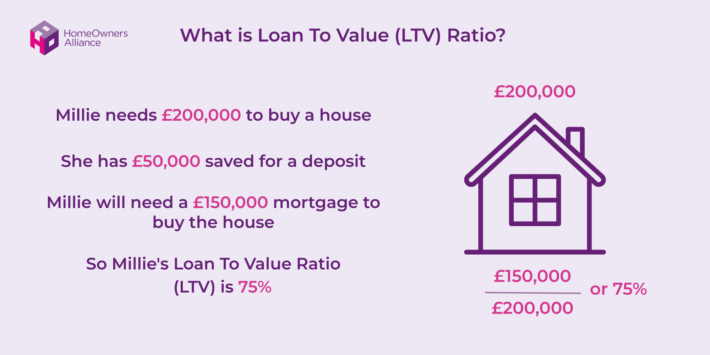

The term LTV stands for loan-to-value and tells you what percentage of the home’s value is borrowed. For example, if you buy a £200,000 house and you pay £50,000 as the deposit, your LTV is 75% because you’ve already paid 25% when you put down the deposit and borrowed the remaining 75%.

At HomeOwners Alliance the best mortgage rates in our tables are from fee-free mortgage brokers L&C and updated regularly. These best mortgage rates do not take into account fees and are for illustration only. The average mortgage rate figures we use are from sources including Rightmove and Moneyfacts.

When you take out a mortgage there are a number of mortgage fees you may need to pay such as an arrangement fee, a mortgage valuation fee, an exit fee and an early repayment charge. Find out more in our guide on Mortgage fees and costs.

This is a charge you pay if you repay all or part of your mortgage earlier than the agreed mortgage term. But not all mortgages have an early repayment charge. But if they do they can be hefty and they’re usually charged as a percentage of the loan. So, if you have a £100,000 mortgage with a 3% early repayment charge you’d pay £3,000. Find out more in our guide on Mortgage fees and costs.

When your fixed deal ends, unless you remortgage onto a new deal you will roll onto your lender’s standard variable rate which can be much more expensive. It’s a good idea to start looking at your remortgage options six months before your initial period ends. For a detailed look at what to do, read our guide on How to remortgage.

This will depend on the type of mortgage you have. If you’re on a tracker mortgage and the Bank of England increases interest rates, your repayments will increase. But if you’re on a fixed rate mortgage your repayments will stay the same until you reach the end of your initial period. Find out more in our guide on Mortgage rate predictions.

A ‘decision in principle’, ‘agreement in principle’, or ‘mortgage in principle’ are all terms that refer to much the same thing. It’s the amount a lender will lend you ‘in principle’ based on some basic information you provide. Find out more in our guide When do I need a mortgage in principle?

There can be more hoops to jump through if you’re looking for a self-employed mortgage but providing you meet the lender’s criteria then you can still get a mortgage. But whenever your situation is less than straight forward it’s always a good idea to speak to an expert about your options. They’ll find the best first time buyer mortgage rates available to you.

If you have a bigger deposit, and therefore a lower loan to value ratio, you’ll be considered less risky by the lender because you’re stumping up more of your own money and they aren’t having to lend as much.

HomeOwners Alliance Ltd is registered in England, company number 07861605. Information provided on HomeOwners Alliance is not intended as a recommendation or financial advice. Mortgage service provided by London & Country Mortgages (L&C), Unit 26 (2.06), Newark Works, 2 Foundry Lane, Bath BA2 3GZ, authorised and regulated by the Financial Conduct Authority (FRN: 143002). The FCA does not regulate most Buy to Let mortgages. Your home or property may be repossessed if you do not keep up repayments on your mortgage. If you complete on a mortgage through L&C, L&C will be paid a commission by the chosen lender. L&C will share a percentage of this commission with HomeOwners Alliance, the referring third party. The commission L&C receives doesn’t affect the product or rate recommended to you.