Find the best estate agent near you Start here

5% deposit mortgages can speed up first time buyers getting on the property ladder and home movers can get them too. But you’ll usually pay higher mortgage rates. We look at the pros and cons of 5% deposit mortgages, the different types you can get and how to find the best deals.

KEY INFORMATION

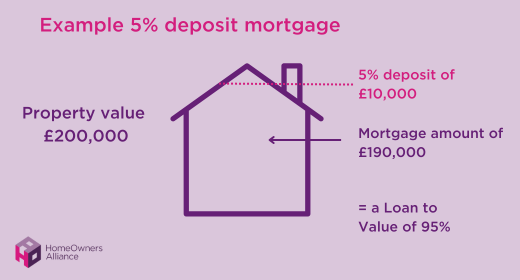

A 5% deposit mortgage means you can buy a house with a 5% deposit and take out a mortgage for the remaining 95%. These mortgages are also called 95% mortgages or 95% Loan to Value (LTV) mortgages (loan to value means the percentage of the property’s value that’s covered by the mortgage).

Here’s how it would work if you’re buying a £300,000 house with a 5% deposit:

| Purchase price | 5% deposit amount in £ | 95% mortgage amount in £ |

|---|---|---|

| £300,000 | £15,000 | £285,000 |

Get fee free mortgage advice from our partners at L&C. Use the online mortgage finder or speak to an advisor today.

If you take out a 5% deposit mortgage to buy a house you may be able to buy your own home much sooner than if you wait to save for a 10% deposit or more. Buying sooner also means you’ll avoid spending more money on spiralling rents.

Equity is the proportion of your home that you own. This includes the deposit you’ve paid. Every time you make a mortgage payment, you will increase the amount of equity in your home. You can also build up equity in your home if its value increases.

Depending on how much equity you build up while you have your 5% deposit mortgage, you may have a 10% deposit or bigger by the time you remortgage. This usually means you’ll then be able to access a wider range of mortgage options and at better rates.

Many mortgage lenders now offer 5% deposit mortgages so you may have a wide choice. More lenders started offering these 95% mortgages after the mortgage guarantee scheme launched 2021. But many lenders now offer these mortgages without using the scheme.

See the deals you qualify for and how much you could borrow:

Get fee free mortgage advice from our partners at L&C. Use the online mortgage finder or speak to an advisor today.

If you have a 5% deposit, lenders will generally view you as more risky than someone who is putting more of their own cash into the property purchase. As a result, mortgage rates on 5% deposit mortgages tend to be higher. So it’s extremely important to shop around. For the latest rates on 5% deposit mortgages (and for all deposit levels from 0%-40%) see our guide on the best First time buyer mortgage rates.

By way of illustration, the following table compares how much you’ll pay on your monthly mortgage payments if you’ve got a 5% deposit, 10% deposit and 25% deposit, using the mortgage rates available in March 2026 for each deposit level. The figures are based on taking out a £200,000 mortgage over 30 years and exclude any fees.

| Deposit % | Interest rate | Monthly mortgage cost |

| 5% | 4.49% | £1,012 |

| 10% | 3.99% | £954 |

| 25% | 3.66% | £916 |

The risk of negative equity (i.e. when the value of your home is lower than your outstanding mortgage balance) may be higher with a 5% deposit mortgage than if you put down a larger deposit. However, by taking out a repayment mortgage, you’ll be building up equity in your home and hopefully your house will increase in value over time too. But you should think carefully before committing.

Self-employed people may find it harder to get 5% deposit mortgages as some lenders only offer self-employed mortgages to people with a 10% deposit or more.

While each mortgage lender has its own criteria, here are some of the common criteria you’ll typically need to meet when applying for 5% deposit mortgages:

If you can buy a house you can afford with a 5% deposit mortgage, and the repayments are affordable, then yes, it may be right for you. Buying sooner rather than later means you’ll start paying off your mortgage earlier – and won’t be using your hard-earned cash paying off your landlord’s.

When your mortgage deal ends, you’ll hopefully be able to remortgage onto a better deal. For example, if you have 10% equity in your home at the end of your mortgage deal due to the mortgage repayments you’ve made and any house price increases, you may have a better choice of mortgages at better mortgage rates.

But you’ll need to weigh that up against the downsides listed above. And get advice from the experts before making a decision.

David Hollingworth of L&C Mortgages says having a good supply of mortgage options for buyers with a small deposit ‘could be invaluable in accelerating their ability to get on the housing ladder. Mortgage rates will be higher than for those with a bigger deposit but that has to be balanced against the chance to buy sooner or even at all.’

Use these handy online tools to see instantly how much you may be able to borrow and how much your mortgage will cost. Our how much can I borrow for a mortgage calculator looks at how much you may be able to borrow based on your income while our mortgage cost and repayment calculator will give you an idea of what your monthly mortgage costs are likely to be.

You can then find out exactly what you can borrow by speaking to our fee-free mortgage broker partners at L&C. They can give you no-obligation mortgage advice and set out your options today, fee-free.

Here are the best 5% deposit mortgage rates in March 2026. The table shows the rate you’ll pay in the initial term, fees you’ll have to pay the lender and then the monthly cost you’ll pay if you borrow £200,000 over a 30 year mortgage term.

| Lender | Initial Rate | Fees | Monthly payment | APRC | Annual Cost | Max LTV |

|---|---|---|---|---|---|---|

| TSB | 5.24% | £495 | £1,103 | 6.9% | £13,486 | 95% |

| Barclays | 5.35% | £0 | £1,117 | 5.7% | £13,402 | 95% |

| Bank of Ireland | 5.39% | £0 | £1,122 | 6.7% | £13,462 | 95% |

| Santander | 5.40% | £-250 | £1,123 | 6.3% | £13,352 | 95% |

| HSBC | 5.44% | £-250 | £1,128 | 6.1% | £13,412 | 95% |

For the best mortgage rates on 5 fixed rate and variable rate mortgages, read our guide to the best first time buyer mortgage rates.

To find the best mortgage tailored to your circumstances, get advice from award-winning brokers L&C. Start the process online or over the phone now.

Get fee free mortgage advice from our partners at L&C. Use the online mortgage finder or speak to an advisor today.

Here’s the step-by-step process to finding and applying for 5% deposit mortgages.

Get fee free mortgage advice from our partners at L&C. Use the online mortgage finder or speak to an advisor today.

When you take out a 5% deposit mortgage you’ll need to decide what type of mortgage to take out.

| Mortgage type | Pros | Cons |

|---|---|---|

| Fixed rate mortgage | You’ll pay a fixed rate during your initial term, usually 2-5 years. So there’s no risk that you’ll have to pay more on your monthly mortgage payments if interest rates increase. | If interest rates fall, you won’t see a reduction in the amount you pay on your mortgage. |

| Tracker mortgages | The rate you’ll pay will go up and down in line with the base rate. This means if the Bank of England cuts interest rates, your mortgage payments will go down. | If interest rates increase, your mortgage payments will go up. |

| Discounted mortgages | Discounted mortgages track under the lender’s standard variable rate. So your mortgage rate could go down. | The rate you’ll pay is linked to the lender’s SVR and it will decide whether to pass on all – or any – of an interest rate cut. Also, the rate you pay could increase. |

A new, permanent mortgage guarantee scheme launched in July 2025 to replace the previous, temporary mortgage guarantee scheme which closed in June 2025.

The scheme is basically the same though, working behind the scenes to encourage lenders to offer 95% mortgages. Here’s how it works for:

It’s worth noting that the mortgage guarantee scheme offers benefits to lenders but there aren’t specific benefits to you as a borrower if the lender is using the scheme. And with so many 95% mortgages available you don’t need to worry about this scheme too much.

95% mortgage guarantee scheme eligibility criteria includes:

More than 50,000 95% LTV mortgages have completed using the mortgage guarantee scheme since it launched in 2021 according to Gov.uk stats. Some 86% of these were first time buyers taking out 5% deposit mortgages.

The mean value of a property bought or remortgaged via this scheme was £208,400, compared with the national average of £292,000.

It can be harder to get 5% deposit mortgages if you’re buying a new build because many lenders are reluctant to offer high LTV mortgages, especially if you’re buying a new build flat, to protect themselves from the risk of the property falling in value in the early years. Read more in our guide on New build mortgages explained.

However, there are schemes that allow you to buy a new build home with 5% deposit mortgages including “Deposit Unlock”. Although there are disadvantages to using this scheme such as having a limited choice of property and mortgage lender, so do your research carefully first. Read more in our guide Deposit Unlock scheme explained

Get fee free advice on all your first time buyer mortgage options with mortgage brokers L&C

Get fee free mortgage advice from our partners at L&C. Use the online mortgage finder or speak to an advisor today.

Remortgaging a house with a 5% deposit works in the same way as if you have a larger amount of equity in your home. Although you may have a smaller choice of lenders and have to pay higher mortgage rates.

You can work out your home equity by taking away your outstanding mortgage balance and any outstanding secured loans from the value of your property.

For example, if your home is valued at £200,000 and you have £190,000 left to pay on your mortgage, the amount that’s left is your equity in the property – in this case £10,000.

If you have a small deposit, there are alternatives to 5% deposit mortgages that you may want to consider including:

Don’t just focus on your deposit, there are other costs of buying you’ll need to factor in. See the summary below or use our cost of moving calculator to get an estimate of the costs to budget for:

Get fee free mortgage advice from our partners at L&C. Use the online mortgage finder or speak to an advisor today.

There are many reasons why you may have a mortgage application declined, such as if you have poor credit history, you’re not registered to vote, you have too much debt or the lender’s calculations say you won’t meet its affordability criteria. Find more information in our guide Mortgage declined? Here’s what to do next.

Yes, you can get a mortgage with no deposit. Skipton Building Society offers a 100% mortgage for renters who have a proven track record of paying rent. While mortgage lender April offers a 100% mortgage to borrowers willing to tie into a 10 or 15 year fixed rate mortgage. Other types of no deposit mortgages include guarantor mortgages, which is when a loved one takes on some of the mortgage’s risk by acting as a guarantor.

This will depend on your circumstances. But don’t assume you’ll have to wait to save a bigger deposit without getting advice from an expert mortgage broker first. Once you know what you can afford to borrow on a mortgage, you’ll be better placed to decide whether you should buy now or wait.

The amount of deposit you’ll need for an interest-only mortgage will vary by lender but you’ll usually need a bigger deposit than for a repayment mortgage as banks view them as riskier. When you take out an interest-only mortgage, your monthly repayments will only cover the interest on your loan, you won’t pay off any of the capital you have borrowed. So you’ll need to have a plan from the outset of how you will repay the loan at the end of the term. Read more in our guide What is an interest-only mortgage? However, you can’t get an interest-only mortgage with 5% deposit mortgages backed by the mortgage guarantee scheme.

HomeOwners Alliance Ltd is registered in England, company number 07861605. Information provided on HomeOwners Alliance is not intended as a recommendation or financial advice.

Mortgage service provided by London & Country Mortgages (L&C), Unit 26 (2.06), Newark Works, 2 Foundry Lane, Bath BA2 3GZ, authorised and regulated by the Financial Conduct Authority (FRN: 143002). The FCA does not regulate most Buy to Let mortgages. Your home or property may be repossessed if you do not keep up repayments on your mortgage.

HomeOwners Alliance Ltd is an Introducer Appointed Representative (IAR) of LifeSearch Limited, an Appointed Representative of LifeSearch Partners Ltd, authorised and regulated by the Financial Conduct Authority. (FRN: 656479).

Independent Financial Adviser service is provided by Unbiased, who match you to a fully regulated, independent financial adviser, with no charge to you for the referral.

Bridging Loan and specialist lending service provided by Chartwell Funding Limited, registered office 5 Badminton Court, Station Road, Yate, Bristol, BS37 5HZ, authorised and regulated by the Financial Conduct Authority (FRN: 458223). Your property may be repossessed if you do not keep up repayments on a mortgage or any debt secured on it.