Find the best estate agent near you Start here

Thinking about buying a second home? Whether it’s a seaside retreat or a city crash pad, there’s a lot to weigh up. This guide covers the costs, mortgage options, taxes and ways to offset expenses or earn from your property.

KEY INFORMATION

The first consideration is whether you can afford to buy a second home. Your next steps depend on whether you’re:

If you’re a cash buyer, you should already have a clear idea of what your budget is and can jump straight to the additional costs of buying a second home.

If you need a mortgage to buy a second home, the type of mortgage and how much you will be able to borrow will depend on how you plan to use the property.

Here’s how it typically works if you’re buying a second home for your personal use.

If you’re planning to buy a second home which you will also let out, you’ll usually need a holiday let mortgage. These mortgages are designed for fluctuating rental income and have different rules to standard Buy to Let mortgages.

Buying a second home? Speak to fee-free mortgage brokers L&C to help you find the best mortgage

Get fee free mortgage advice from our partners at L&C. Use the online mortgage finder or speak to an advisor today.

If you don’t have the cash for a second home mortgage deposit, one way to raise it is by remortgaging to release equity.

This means taking out a bigger loan against your current property in order to free up some of the cash you’ve built up in it.

For example:

You own a house worth £400,000 with an outstanding mortgage of £100,000. This means you have £300,000 equity in your house.

| House value | £400,000 |

| Outstanding mortgage amount | £100,000 |

| Equity in your house | £300,000 |

If you remortgage to release £100,000, you will now owe £200,000 on your mortgage and own £200,000 equity in your current home. You will also have freed up £100,000 as a deposit for your second home.

| House value | £400,000 |

| Outstanding mortgage amount | £200,000 |

| Equity in your house | £200,000 + you’ll have a £100,000 deposit for your second home. |

However, you’ll need to have enough equity in your home to be able to do this. And remortgaging to release equity means your debt will increase so it’s important to weigh up the pros and cons and to get expert advice from a mortgage broker.

The easiest way to calculate how much equity you have in your house is to use our free mortgage equity calculator tool.

Get fee free mortgage advice from our partners at L&C. Use the online mortgage finder or speak to an advisor today.

When you’re working out whether you can afford to buy a second home there are a number of extra costs you’ll need to factor in:

| Purchase price | Stamp duty rate | Stamp duty rate for additional properties |

| Up to £125,000 | 0% | 5% |

| £125,001 to £250,000 | 2% | 7% |

| £250,001 to £925,000 | 5% | 10% |

| £925,001 up to £1.5 million | 10% | 15% |

| Over £1.5 million | 12% | 17% |

There are different rates on additional homes in Wales and Scotland. Find out more with our guide to stamp duty on second homes or use our stamp duty calculator.

When you sell your main home (or only home) you don’t usually have to pay any capital gains tax (CGT), due to private residence relief.

But, you’ll usually need to pay capital gains tax on property if you’re selling a Buy to Let property or second home. The tax is payable on any gain in its value above your CGT allowance (after any deductions have been taken off). Find out more with our guide to capital gains tax when selling your home. If you’re buying a second home, it’s a good idea to speak to an independent financial adviser first.

Owning a second home could mean you’re stung with a much bigger council tax bill.

This is a highly contentious issue among second home owners, many of whom have commented on the issue in our guide to Second home council tax explained.

However, you may be able to get a reduction if your home meets certain criteria. See our guide to council tax reductions for more information.

If you own another home, you’ll need to cover the costs of running it. Depending on how often you stay in your second home, you may want to pay someone to keep on top of things, such as a gardener. You’ll also need to pay utility bills like gas and electricity.

If you’re renting it out as a holiday let and using a bookings site, you’ll also need to pay its fees.

So make sure you’re on the best deals to keep bills as low as possible. Use our free energy comparison tool to instantly check what deals are available and see if you can cut your energy bills.

If you own a second home, you’ll need to pay to insure it. You’ll usually need to take out special second home insurance – a standard home insurance policy won’t usually be suitable. Again, make sure you shop around for the best deal.

If you’re buying a second home with the intention of renovating it, make sure you’re fully aware of what the costs may be from the outset. You’ll also need to consider how you will pay for the work. Our guide on Home repairs and improvements is a good place to start.

Get fee free mortgage advice from our partners at L&C. Use the online mortgage finder or speak to an advisor today.

Before you start viewing properties, decide exactly what you want the home for – this will shape the mortgage you need and location you choose.

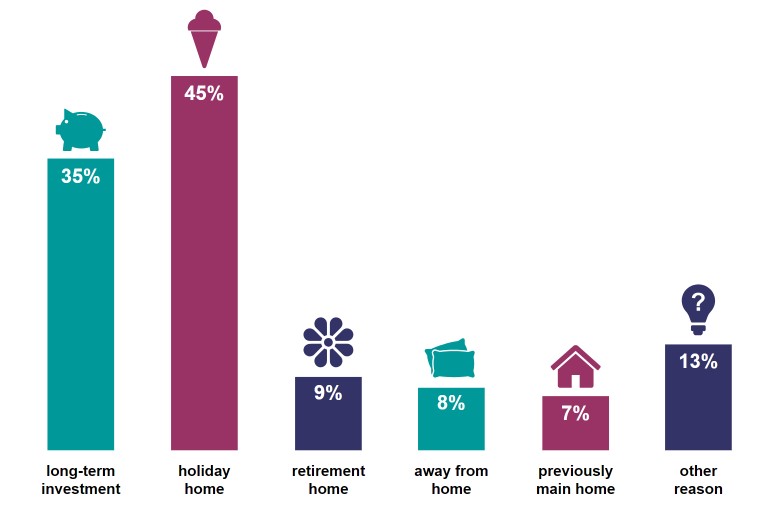

There are a number of reasons for buying a second home including:

It is important you know exactly what you want to get from buying a second home so you can find the right one.

There were 809,000 second homes in England, according to the most recent English Housing Survey for 2021 to 2022. This was an increase of 13% compared to 2010-11.

Here are the most common reasons for buying a second home, according to the Government’s English Housing Survey 2021 to 2022.

If your goal is to earn income from your second home, you’ll need to decide whether to let it short-term as a holiday let or long-term as a Buy to Let.

| Type of rental | Buy to Let | Holiday Let |

| Can you use as a second home? | No. Once your property has been let you won’t be able to use it as a second home. | Yes. You can choose when it will be available to let out to holidaymakers so that you can still use it. |

| Income potential | You’ll usually get less per week/ month than with a holiday let but when the property is let your income will be regular. | You may achieve a higher rate per week/ month. But bookings may be seasonal and you may earn less over the course of the year. |

| How much management will it need? | Once your tenants are in place, you’ll usually only need to get involved if there are problems to resolve. You may get an estate agency to handle this for you but you’ll pay for this service. | The property will need to be cleaned in between lets and other upkeep will need to be done such as gardening. You may get a holiday let company to do this for you but you’ll pay for this. |

There are other things you’ll need to consider before letting out your second home.

You don’t have to make life’s big financial decisions alone. Get the right IFA for you today with our partners at Unbiased.

Choosing the right location and property is key, and it’s even more important if you’re planning to let it out as you’ll want to make sure it’s going to be a desirable place to rent out.

When you’re choosing the right house you’ll need to:

Make an offer and get it accepted: Once you’ve found the second home you want to buy, making an offer for the right amount is key. Find out how to calculate how much to offer in How do I know I’m not paying too much?

Then get ready for negotiations – see our guide Making an offer – and haggling over the price. If you are worried about negotiating, you can appoint a Buying Agent.

Having an offer accepted is exciting but it’s not a done deal until you exchange contracts. It’s common for sales to fall through: more than 4 in 10 sales collapsed April-June 2025, according to Quick Move Now’s data.

So consider buying Home Buyers Protection Insurance, which helps cover elements of your legal, survey and mortgage costs should your purchase fall through.

Cover for conveyancing, mortgage and survey costs, should your property purchase fall through.

If you’re buying a second home with a mortgage, you’ll need to make your application without delay.

The type of mortgage you’ll need depends on how you plan to use the property. Will it be for your sole use as a holiday home or will you let it out as a holiday let? The quickest way to find the right second home mortgage for you and the best rates is to speak to a fee-free mortgage broker.

Once your mortgage offer is in place (if you need one), your pre-contract enquiries have been answered, and the survey and searches have been sorted out, you are ready to exchange contracts. At this point a completion date should be set. Completion is when you pay for the property and take ownership of it. You are now free to move in.

The final stages involve your conveyancer sending you an account, covering all their costs and disbursements, as well as the purchase price of the house and stamp duty. Your conveyancer will normally pay the stamp duty for you, and make sure the change of ownership is registered with the Land Registry.

If you’re interested in buying a second home, another route to consider may be Let to Buy, which involves renting out your current home and buying a new house to live in.

You won’t have a second home to enjoy as a holiday home but it may offer a long-term investment as well as a monthly income.

Let to Buy involves having two mortgages:

Read more about how this works in our guide Let to Buy mortgages explained

Here are some of the tax implications of Let to Buy

You don’t have to make life’s big financial decisions alone. Get the right IFA for you today with our partners at Unbiased.

If you’re considering buying a second home to help a family member such as your children, you should be aware of the additional costs involved and compare this to other ways of helping them get on the property ladder.

There are some other ways you can help your child buy a house including

Considering buying a second home as an investment? Here are the pros and cons to weigh up:

| Pros | Cons |

|---|---|

| Long-term investment growth potential | High set-up costs including the property price, stamp duty and buying costs. As an investment, it could take a couple of years before you break even. |

| Rental income potential if you let it out as a Buy to Let or a holiday let. | How will you fund it? You’ll usually need at least a 15% deposit and if you’ll have two mortgages you’ll need to prove you can afford both. |

| Lifestyle benefits: Having a second home means you’ll be able to enjoy spending time in it and use it for holidays or weekends away. | Selling costs: As well as having the usual costs of selling a house, you may also need to pay capital gains tax |

| Your money is tied up in property and will be difficult to access if you need it quickly. |

If you’re buying a second home, there are a number of responsibilities you’ll need to make sure are covered including:

Get fee free mortgage advice from our partners at L&C. Use the online mortgage finder or speak to an advisor today.

– Buying a second home can give you a holiday home you can enjoy, can provide rental income if you let it out as a holiday let and may be a good long-term investment too.

– But there are drawbacks to consider. Buying a second home can be expensive and there are additional costs to meet such as the higher rate of stamp duty, maintenance costs and potentially a higher rate of council tax too.

If you need to get a mortgage to buy a second home you’ll usually need at least a 15%-25% deposit, meet affordability criteria, have a good credit score and if you plan to let out the second property, you will need to give lenders details of the likely rental income.

Some second homeowners in England have been registering their property as a business and letting it out to avoid council tax and access small business rates relief instead. But there has been a tightening of the rules to crack down on this second home council tax loophole. Read more in our guide on Second home council tax.

You’ll usually need at least a 15%-25% deposit to get a mortgage to buy a second house.

Gifted deposits are given with the understanding that the money doesn’t need to be repaid. The person gifting the money has no rights or legal interest in the property being purchased. Any gifts must be declared to a mortgage lender. And the person gifting the money may also need to provide bank statements to show the origin of the funds, as part of anti-money laundering checks. Find out more in our guide on Gifted deposits.

A mansion tax, officially called the High Value Council Tax Surcharge, will be introduced on homes worth over £2 million. The mansion tax will apply to homeowners with properties valued at more than £2 million in 2026, and be collected alongside council tax from April 2028.

HomeOwners Alliance Ltd is registered in England, company number 07861605. Information provided on HomeOwners Alliance is not intended as a recommendation or financial advice.

Mortgage service provided by London & Country Mortgages (L&C), Unit 26 (2.06), Newark Works, 2 Foundry Lane, Bath BA2 3GZ, authorised and regulated by the Financial Conduct Authority (FRN: 143002). The FCA does not regulate most Buy to Let mortgages. Your home or property may be repossessed if you do not keep up repayments on your mortgage.

HomeOwners Alliance Ltd is an Introducer Appointed Representative (IAR) of LifeSearch Limited, an Appointed Representative of LifeSearch Partners Ltd, authorised and regulated by the Financial Conduct Authority. (FRN: 656479).

Independent Financial Adviser service is provided by Unbiased, who match you to a fully regulated, independent financial adviser, with no charge to you for the referral.

Bridging Loan and specialist lending service provided by Chartwell Funding Limited, registered office 5 Badminton Court, Station Road, Yate, Bristol, BS37 5HZ, authorised and regulated by the Financial Conduct Authority (FRN: 458223). Your property may be repossessed if you do not keep up repayments on a mortgage or any debt secured on it.