Find the best estate agent near you Start here

If you sell your house now, you’ll benefit from increased house prices. But with house prices expected to rise further in 2026, we look at the pros and cons of selling now vs waiting.

KEY INFORMATION

Here are the reasons why it’s a good time to sell a house:

Yes. If you want or need to sell your house now, you should. People always need to move home for a myriad of personal reasons regardless of what’s happening in the housing market. These include:

Unlike investors driven by profits and house prices, a homeowner’s priority will be to act on what’s best for their personal circumstances.

Having said that, our homes are often our biggest financial asset, so it’s worth understanding what’s happening in the market when deciding whether to sell your house now.

Across the major indices, house prices are up on average 0.1% over the past month. Annual house price growth is also up to 1.5%, up from 1.1% last month. Stay up to date with our monthly House Price Report which includes the latest house price index reports from Land Registry, Halifax, Nationwide, Rightmove and Zoopla.

We’ve also compiled a report of the cheapest areas to buy at the moment.

Find out how much your house is worth with our online tool.

Here’s how average house prices have changed across the UK, according to the Land Registry’s November 2025 House Price Index:

| UK Region | Average price £ | Monthly change | Annual change |

|---|---|---|---|

| England | 291865 | -0.70% | 1.70% |

| Northern Ireland | 195936 | 1.40% | 7.50% |

| Scotland | 190649 | -1.70% | 4.90% |

| Wales | 214883 | 2.60% | 5.00% |

| North West | 217428 | -0.40% | 4.50% |

| Yorkshire and the Humber | 208447 | -0.50% | 3.30% |

| North East | 165257 | -1.40% | 4.60% |

| West Midlands | 246141 | -1.00% | 2.00% |

| East Midlands | 243632 | 0.40% | 2.40% |

| South West | 301226 | -1.70% | 0.30% |

| East of England | 338002 | -0.40% | 1.50% |

| South East | 378800 | -0.70% | 0.00% |

| London | 551294 | -0.80% | -1.00% |

UK house prices are expected to rise in 2026, with experts’ early forecasts in the 1.5%-4% range. Read more in our guide House price predictions: How much will prices go up by?

Keep up-to-date with the latest on house sale activity in our monthly House Price Watch.

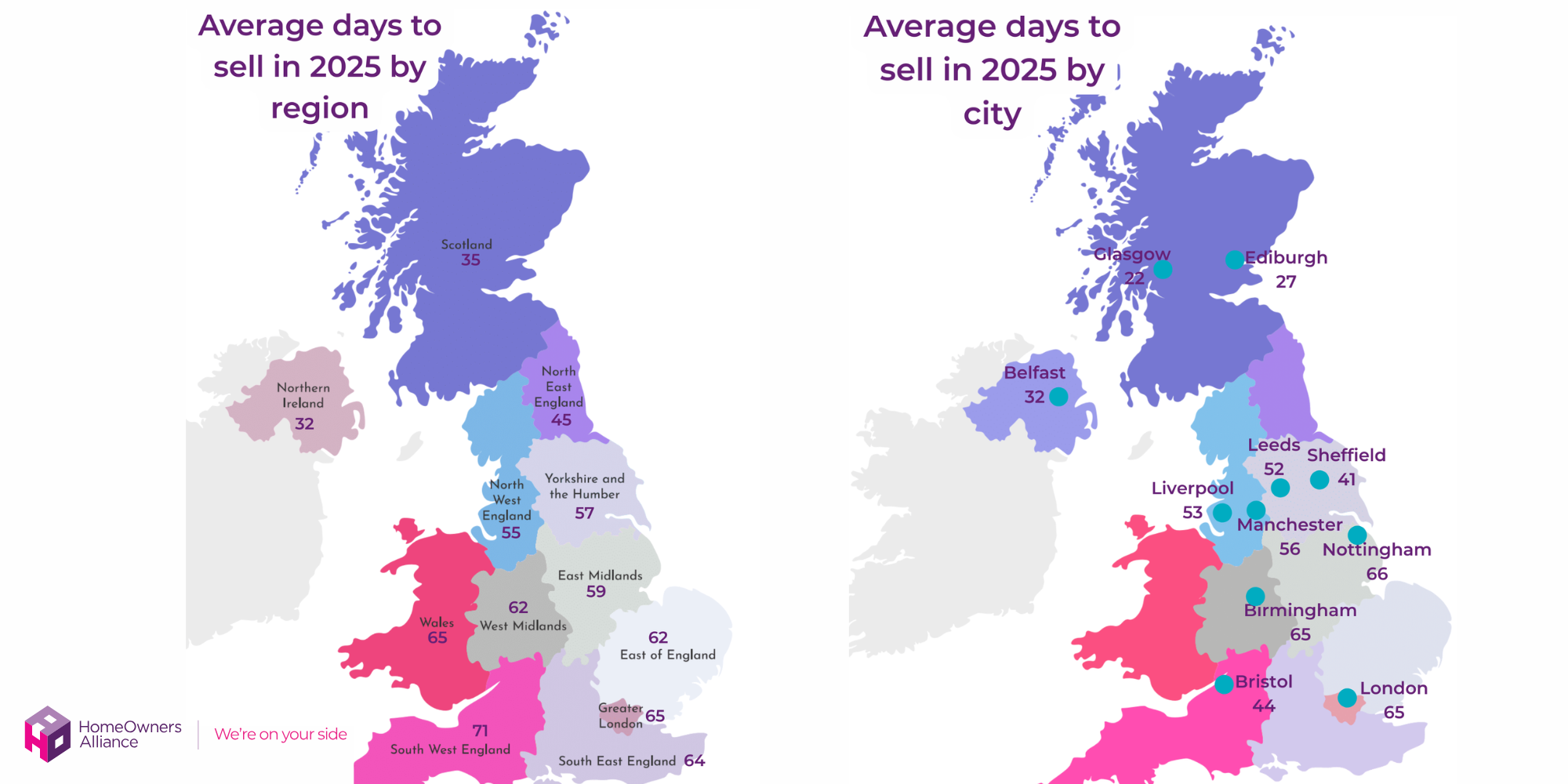

In terms of weighing up the timing of whether now is the right time to sell, bear in mind that it takes 8 weeks to get a sale agreed (58 days) on average. But how long it takes to sell depends on how competitively you’ve priced your house and your local market. Getting to completion can take as long as 5 months.

Speed of sale can give an indication of how hot or cold a local area is. According to data from our best estate agent finder, it currently takes an average of 58 days to agree a sale on a home in the UK but this varies regionally from a low of 32 days in Northern Ireland to a high of 71 days in the South West of England.

If you need to sell your house, perhaps because you need to relocate, then don’t let speculation over property prices delay you making this decision. No one really knows what will happen with house prices in the future so you need to do what is right for you.

And if you’re wondering whether to wait because you hope your property will increase in value, you may find the property you want to buy will also increase in value. So the gains are really relative unless you’re cashing out of the housing market altogether.

If you’re hoping to sell your home, it’s a good idea to get a handle on the costs to budget for. Use our simple cost of moving calculator to quickly get an idea of the costs involved.

And, if you want to act quickly, get your conveyancer lined up now. You can compare quotes from regulated and reviewed conveyancing solicitors to find the best service at the best price.

And if you’re looking for an estate agent, our free Best Estate Agent Finder lists your best local estate agents based on how quickly they sell, how often they achieve asking price, their success rate and more.

Find the best estate agent. Instantly find and compare the performance of local estate agents near you.

Looking for more evidence it’s the right time to sell? There is lots of research you can do to establish if now is a good time:

The optimum time you should own a property before selling it if you want a return on the investment is nine years, according to research by Middleton Advisors.

Middleton Advisors’ MD Mark Parkinson says, ‘Nine years is a long-enough time to allow markets to recover from a downward cycle. So, even if you buy at the peak – i.e. right before a price correction – in every housing cycle since December 1962, prices would have recovered sufficiently after nine years to give you a positive nominal return.’

However, the optimum time for you to sell your house will depend on a number of factors including local market conditions.

In separate research, Zoopla found that homeowners live in their home for an average of nine years before selling.

If an extension can give you the space you need instead of moving, you’ll avoid all the hassle of a move and the costs, not least conveyancing fees and stamp duty.

There’s a lot to consider: Will your extension plans add value to your home? Will you need planning permission? Should you engage an architect and if so what are their fees? Find out more in our guide Home Extension: where do I start?

Renting out your house may make sense if for example, you’re moving temporarily, perhaps for work, and you want to keep the option of moving back to your old house. Or if it’s an attractive rental property likely to generate good rental income. Our rental calculator can give you a good idea of how much.

There’s a lot to think about; unless you’re planning to let it out for a short period and your mortgage lender gives you ‘consent to let’ so you can rent it out, you’ll need to switch to a Buy to Let mortgage. There are tax implications too. Read more in our guide Should I sell my home or rent it out?

The most popular times to sell a house are traditionally spring or early autumn. Experts are predicting that March 2026 may be busier than usual, due to buyers who had put plans on hold to wait for the outcome of the autumn Budget getting on with their moving plans.

Also, people are moving all year round. You need to consider trends in your local market too so choose a good estate agent and ask them to show you the figures tailored to your area and your property type. See our guide when is the best time to sell my house?

Traditionally, August and December have been considered the worst months to sell a house. In August, many people are away on holiday while in December, people are gearing up for Christmas.

However, serious buyers are often around in these periods. Also, by being on the market in August or December, you’ll be in a good position and ready to go when the market picks up again.

Negative equity occurs when the market value of your house is below the outstanding mortgage secured on it.

Negative equity is more common when house prices are falling and it is a major concern when you want to sell your home. Whether you are at risk of this depends on your circumstances. Find out more in our guide What can I do about negative equity.

If you own a Buy to Let property, you may be asking should I sell my house now? Various factors may have made owning your Buy to Let property less profitable in recent years, such as increasing Buy to Let mortgage rates.

So if the figures don’t stack up for you anymore and you want to sell, read our guide Selling a Buy to Let Property. You’ll need to decide whether to sell your Buy to Let with sitting tenants or with vacant possession. Read more in our useful guide on Selling a house with tenants.

However, selling a house with vacant possession doesn’t mean you have to miss out on rental income if you think a short-term let is possible whilst you sell your home.

Our partners at Flyp.co offer a service where they will handle the sale of your vacant property and arrange a short-term let for you at the same time. They’ll also manage all the viewings and ensure that the property is cleaned and viewing-ready at all times.

Plus, they also offer a transformation service if the property needs some improvements or staging to help it sell (at no cost to you). Flyp’s selling service also provides access to multiple agents at a sole agency fee, so they are worth comparing against other local estate agents.

Get in touch with our partners at Flyp to find out more

See how our partners, Flyp, can help you earn rent and get your property sold.

Deciding to sell your house and rent is a big decision and not one to take lightly. House prices may increase by more than you expect by the time you come to buy, plus with strong demand for rental properties in many areas you may find you have to pay more in rent than on your mortgage payments.

So if you’re asking should I sell my house now and rent, do your research thoroughly.

If you’ve decided the answer to ‘Should I sell my house now?’ is yes – here’s how to do it as quickly as possible.

Use our Best Estate Agent Finder to find the best local estate agent based on how quickly they sell, how often they achieve asking price, their success rate and more.

Online estate agents offer an affordable and, as the name suggests, online service. Take a look at our online estate agent comparison table which compares all the main providers, from PurpleBricks to YOPA so you can choose the right package and price for your house sale. Some online agents like Strike even offer to sell your house for free.

You can compare quotes now from conveyancing solicitors and speak to them about the process and costs so you’re ready to instruct them.

They can complete transactions quicker. Find and compare quotes from conveyancing firms today.

Also known as an EPC this has to be included with a sale by law. It shows how energy efficient your new home is and if you moved in within the last 10 years, yours is still valid. Here’s how to check if you have one or how to get one if you still need to.

Locate certificates showing compliance with regulations of any works done from planning permissions to FENSA certificates for window replacements. If it’s a leasehold, find the lease. Don’t forget valid guarantees a home buyer will want to see. Here’s a list of essential documents for sale to get ready

If you are buying a property at the same time, start the mortgage process now by speaking to a mortgage broker about your options and getting a mortgage in principle.

Also, if you’re purchasing a new property, consider getting Home Buyers Protection Insurance which helps cover legal, survey and mortgage lending costs should your purchase fall through. Cover starts from just £74.

Cover for conveyancing, mortgage and survey costs, should your property purchase fall through.

When you’re house hunting you may face strong competition from buyers who have either already sold or don’t need to sell. So if your property is under offer at the very least, you’ll be in a good position. But be aware things can get tricky if you sell your house but then can’t find a new one.

Preparing your home for viewers is important. It will not only ensure your property sells faster but for a higher sale price; potentially adding thousands of pounds to its value. See our guide on the 12 Tips to make your home more valuable and sell faster

The amount you can sell your house for will depend on lots of factors including where you live and what’s happening in the local market. Take a look at our House Price Watch for house price averages in your area and read What price should I sell my house for?

While in an ideal world your home would look perfect, you need to prioritise spending money on essential repairs and on minor redecoration that will help your home sell faster. To help you prioritise what’s most important, see our guide to what not to fix when selling your house.

HomeOwners Alliance Ltd is registered in England, company number 07861605. Information provided on HomeOwners Alliance is not intended as a recommendation or financial advice.

Mortgage service provided by London & Country Mortgages (L&C), Unit 26 (2.06), Newark Works, 2 Foundry Lane, Bath BA2 3GZ, authorised and regulated by the Financial Conduct Authority (FRN: 143002). The FCA does not regulate most Buy to Let mortgages. Your home or property may be repossessed if you do not keep up repayments on your mortgage.

HomeOwners Alliance Ltd is an Introducer Appointed Representative (IAR) of LifeSearch Limited, an Appointed Representative of LifeSearch Partners Ltd, authorised and regulated by the Financial Conduct Authority. (FRN: 656479).

Independent Financial Adviser service is provided by Unbiased, who match you to a fully regulated, independent financial adviser, with no charge to you for the referral.

Bridging Loan and specialist lending service provided by Chartwell Funding Limited, registered office 5 Badminton Court, Station Road, Yate, Bristol, BS37 5HZ, authorised and regulated by the Financial Conduct Authority (FRN: 458223). Your property may be repossessed if you do not keep up repayments on a mortgage or any debt secured on it.