Find the best estate agent near you Start here

Learn how fixed rate mortgages work, the pros & cons, today’s best fixed mortgage rates, and how long to fix for.

KEY INFORMATION

Here’s an overview of what fixed rate mortgages are & how they work:

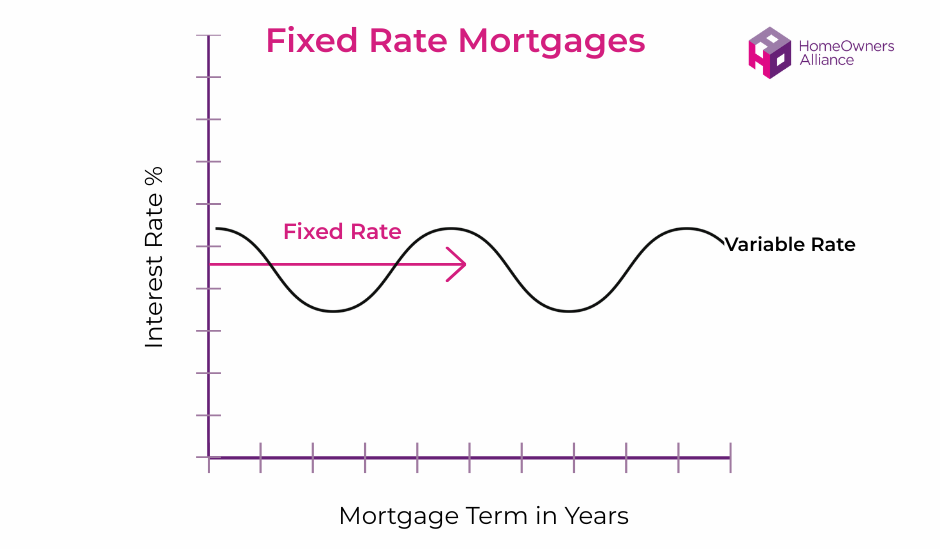

A fixed rate mortgage is a home loan where the interest rate and monthly payments stay the same for a set period, usually 2, 3, 5 or 10 years.

Fixed rate mortgages offer stability because the rate you’ll pay will remain the same even if the Bank of England base rate changes.

Once your fixed rate period ends, you’ll usually switch to your lender’s standard variable rate (SVR) unless you remortgage to a new deal.

Not sure whether to fix for 2 years or 5 years, see our guide on what to consider.

Get fee free mortgage advice from our partners at L&C. Use the online mortgage finder or speak to an advisor today.

“There’s plenty of jargon in mortgages but fixed rates do exactly what it says on the tin. They offer the chance to lock in the rate for a specified period of time, which can often be two to five years but can extend to ten years or even for the life of the mortgage. That gives borrowers the chance to know exactly where they stand and remove any worries about what may happen to interest rates in the wider economy. The peace of mind of knowing that monthly payments will not increase over a certain period is what will often attract borrowers to a fixed rate.

“Just as a fixed rate will buffer the borrower against any rise in interest rates, the downside could be that rates fall leaving the homeowner stuck on a higher rate until the end of the deal.

“The vast majority of fixed rates will tie the borrower in with Early Repayment Charges (ERCs) during the fixed rate period. That can limit the level of flexibility that fixed rates allow and if there was a need to repay the mortgage it can result in a substantial penalty.”

Fixed rate mortgage deals are by far the most common type of mortgage. UK Finance statistics from May 2025 show that 85% of outstanding mortgages are fixed rate mortgages compared to 7% on tracker mortgages and 6% on the SVR.

When you’re weighing up whether to take out a fixed rate mortgage you’ll need to consider the alternative – a variable rate mortgage. There are two main kinds when taking out a mortgage:

You can also get standard variable rate mortgages, but this is the deal you’ll usually roll onto when your current mortgage deal ends if you won’t remortgage. The lender sets the amount you pay and these are notoriously expensive.

| Feature | Fixed rate mortgage deals | Variable rate mortgage (inc trackers) |

|---|---|---|

| Monthly payments | Payments are fixed and do not change | Payments can rise and fall in line with a market rate, like the Bank of England base rate |

| Interest rate | Will stay the same | May increase or decrease |

| Flexibility | Usually have early repayment charge if you leave the deal early | Some deals let you leave with paying an ERC |

The best fixed mortgage rates today will depend on your deposit size and the length of your term. However, here are the best fixed mortgage rates currently available if you’re looking for a 2 or 5 year fixed deal.

| Lender | Initial Rate | Fees | Monthly payment | APRC | Annual Cost | Max LTV |

|---|---|---|---|---|---|---|

| Nationwide | 4.71% | £999 | £1,038 | 6.2% | £12,961 | 60% |

| Natwest | 4.75% | £1,495 | £1,043 | 6.4% | £13,267 | 60% |

| Yorkshire BS | 4.76% | £995 | £1,045 | 6.4% | £13,032 | 60% |

| Natwest | 4.80% | £995 | £1,049 | 6.4% | £13,089 | 60% |

| Principality | 4.80% | £1,499 | £1,049 | 6.4% | £13,341 | 65% |

| Lender | Initial Rate | Fees | Monthly payment | APRC | Annual Cost | Max LTV |

|---|---|---|---|---|---|---|

| Natwest | 4.79% | £1,454 | £1,048 | 6.4% | £13,304 | 60% |

| Principality | 4.80% | £1,808 | £1,049 | 6.4% | £13,496 | 65% |

| Natwest | 4.84% | £954 | £1,054 | 6.4% | £13,127 | 60% |

| Principality | 4.86% | £1,204 | £1,057 | 6.5% | £13,281 | 65% |

| Natwest | 4.87% | £1,454 | £1,058 | 6.4% | £13,421 | 75% |

| Lender | Initial Rate | Fees | Monthly payment | APRC | Annual Cost | Max LTV |

|---|---|---|---|---|---|---|

| Yorkshire BS | 4.77% | £995 | £1,046 | 6.0% | £12,748 | 60% |

| Yorkshire BS | 4.79% | £995 | £1,048 | 6.0% | £12,776 | 75% |

| Yorkshire BS | 4.79% | £995 | £1,048 | 6.0% | £12,776 | 60% |

| Yorkshire BS | 4.81% | £995 | £1,051 | 6.0% | £12,805 | 75% |

| Yorkshire BS | 4.83% | £995 | £1,053 | 6.0% | £12,835 | 80% |

| Lender | Initial Rate | Fees | Monthly payment | APRC | Annual Cost | Max LTV |

|---|---|---|---|---|---|---|

| Yorkshire BS | 4.80% | £995 | £1,049 | 6.0% | £12,791 | 60% |

| Nationwide | 4.80% | £808 | £1,049 | 5.8% | £12,754 | 60% |

| Yorkshire BS | 4.81% | £995 | £1,051 | 6.0% | £12,805 | 75% |

| Santander | 4.83% | £1,058 | £1,053 | 5.9% | £12,847 | 60% |

| Yorkshire BS | 4.85% | £995 | £1,055 | 6.0% | £12,864 | 60% |

If you’ve decided a fixed rate mortgage is right for you, the next step is to work out how long to fix for.

When considering whether to take out a 2 or 5 year fixed rate mortgage:

30 year fixed rate mortgages are much less common in the UK than in the US or Europe but there are some available.

Paula Higgins, CEO of HomeOwners Alliance, says:

“The vast majority of people who come to our site choose to take out 2 or 5 year fixed rate mortgages. Most recently people have slightly favoured 5 year fixed mortgage deals but this fluctuates. However, don’t just go with the majority. If you’re taking out a fixed rate mortgage you’ll need to decide how long to fix is best for you. A good mortgage broker will help you weigh up the pros and cons and help you decide which is best for you.“

Yes – many lenders allow you to ‘port your mortgage‘. This means you transfer your existing fixed rate mortgage to a new property, keeping the same rate and features.

Try our fixed rate mortgage calculator to compare monthly payments across different terms.

How much you can borrow on a fixed rate mortgage and lender criteria is based on these criteria:

Get fee free mortgage advice from our partners at L&C. Use the online mortgage finder or speak to an advisor today.

In theory, the best time to fix a mortgage rate is when the base rate is expected to increase. However, while it’s useful to understand what’s expected to happen to mortgage rates (see our guides to mortgage rate predictions and interest rate forecasts) no one really knows what will happen next with mortgage rates.

So instead of trying to second guess the market, focus on what options are available to you and what is best for your situation. An expert mortgage broker will help you with this.

There are a number of different types of buyers who pay want to consider fixed rate mortgages:

On top of your monthly payments, there are a number of mortgage fees you may need to pay when taking out a fixed rate mortgage.

| Mortgage Fees | What it is | Typical cost |

|---|---|---|

| Arrangement fee | Often charged by lenders to access their best mortgage rates | Up to £1,500 |

| Booking fee | This is a non-refundable fee that some lenders charge when you apply for a mortgage. | Up to £250 |

| Mortgage valuation fee | Cost of valuation to satisfy the lender the property is worth at least as much as you’ve offered to pay for it. Not all lenders charge this. | Up to £300 |

| Telegraphic transfer fee | CHAPS fee (Clearing House Automated Payment System) for transferring the money from the lender to your solicitor. | £25 to £50 |

| Mortgage account fee | This covers your lender’s administration costs for your mortgage. You usually either have an account fee on a mortgage or an exit fee but rarely both. | £100 to £300 |

| Mortgage broker fee | Some brokers charge for their service but others like L&C are fee-free. | £0- £1,000s |

Get fee free mortgage advice from our partners at L&C. Use the online mortgage finder or speak to an advisor today.

A fixed rate mortgage is a home loan where the interest rate stays the same for a set period — typically 2, 3, 5 or 10 years. This means your monthly repayments won’t change during the fixed term, making it easier to budget and protecting you from interest rate rises. Once the fixed period ends, you’ll usually move onto your lender’s standard variable rate (SVR) unless you remortgage.

Yes you can usually extend the term of your fixed rate mortgage to reduce your monthly payments. However, not all lenders offer this and you’ll need to meet their lending criteria.

It is usually possible to remortgage before your fixed rate ends but you may need to pay an early repayment charge if you do this. These are usually 1%-5% of the outstanding mortgage balance.

A fixed rate mortgage is better than a tracker if you want certainty over how much your mortgage payments will be during your mortgage deal.

Mortgage rates change frequently so the easiest way to find the best fixed rate mortgage is to speak to an expert mortgage broker.

The longest fixed rate mortgage in the UK is 30 years. However, fixed mortgage rates of this length are very uncommon. Most fixed rate mortgages are 2, 3, 5 or 10 years.

Most fixed rate mortgages allow overpayments of up to 10% of the outstanding mortgage balance each year. However, some lenders allow you to overpay more. But not all mortgages have this feature. It’s important to find out what your lender allows because if you overpay by more than the annual limit you may need to pay an early repayment charge.

Not sure what some of the terms mean? Here’s a quick guide to the most common mortgage phrases you’ll come across when comparing the best fixed rate mortgage deals.

| Term | What it is |

|---|---|

| Standard Variable Rate | The default rate you move onto when your mortgage deal ends. Usually higher and more expensive than a fixed mortgage or tracker deal. |

| ERC (Early Repayment Charge) | A fee charged by lenders if you remortgage or pay off your mortgage early, or make overpayments above your allowance during your fixed term. |

| LTV (Loan to Value) | The percentage of the property’s value you borrow. For example, a £180,000 mortgage on a £200,000 property is 90% LTV. |

| APRC (Annual Percentage Rate of Charge) | The total annual cost of your mortgage over its lifetime, including interest and fees, expressed as a percentage. Useful for comparing the best mortgage rates. |

| Base rate | The interest rate set by the Bank of England. |

| Initial interest rate | The interest rate you’ll be charged for the set period at the start of your mortgage. |

| Initial rate period | The length of your fixed or variable rate mortgage deal before you switch to the standard variable rate. |

| Mortgage term | The full length of your mortgage, including any introductory term. |

HomeOwners Alliance Ltd is registered in England, company number 07861605. Information provided on HomeOwners Alliance is not intended as a recommendation or financial advice.

Mortgage service provided by London & Country Mortgages (L&C), Unit 26 (2.06), Newark Works, 2 Foundry Lane, Bath BA2 3GZ, authorised and regulated by the Financial Conduct Authority (FRN: 143002). The FCA does not regulate most Buy to Let mortgages. Your home or property may be repossessed if you do not keep up repayments on your mortgage.

HomeOwners Alliance Ltd is an Introducer Appointed Representative (IAR) of LifeSearch Limited, an Appointed Representative of LifeSearch Partners Ltd, authorised and regulated by the Financial Conduct Authority. (FRN: 656479).

Independent Financial Adviser service is provided by Unbiased, who match you to a fully regulated, independent financial adviser, with no charge to you for the referral.

Bridging Loan and specialist lending service provided by Chartwell Funding Limited, registered office 5 Badminton Court, Station Road, Yate, Bristol, BS37 5HZ, authorised and regulated by the Financial Conduct Authority (FRN: 458223). Your property may be repossessed if you do not keep up repayments on a mortgage or any debt secured on it.