Find the best estate agent near you Start here

What is conveyancing? It's the legal process of transferring the ownership of property from the seller to the buyer. We explain everything you need to know about the stages of the conveyancing process when buying.

Conveyancing is the legal process involved when the ownership of a property is transferred from the seller to the buyer. When you are buying a house, the conveyancing process starts when an offer is accepted on a house and finishes when you complete on your purchase, you collect the keys and your conveyancer takes the final steps such as registering the property in your name at the Land Registry.

If you’re a cash buyer, you may consider DIY conveyancing. But this can be risky. In most cases you’ll need a conveyancing solicitor to act on your behalf.

Compare conveyancing quotes from regulated and reviewed conveyancing solicitors that cover your area.

What conveyancers and conveyancing solicitors do, is handle legal side of property transactions. They handle contracts, give legal advice, carry out searches and transfer the money to pay for your property. See our guide which explains the difference between a solicitor and a conveyancer. But, whether you use a conveyancer or solicitor to do the legal work, the stages of the conveyancing process are the same.

There are a number of stages of the conveyancing process. Here’s our step by step guide to the conveyancing process for buyers.

The first stage of the conveyancing process is to find the right solicitor or conveyancer and instruct them to start work on the legal side of your purchase.

If you’re considering using the conveyancing solicitor recommended by the estate agent for the house you’re buying, we’d advise you to compare conveyancing quotes first to check you’re getting a good deal. You’re not obliged to use the conveyancer the estate agent recommends and you may get a better service for a better price by shopping around.

Get instant quotes from regulated and reviewed conveyancing solicitors that cover your area. Our customers save on average £490.

See our guide on conveyancing fees to give you an idea of the costs and what conveyancing solicitors include in their fees. You may find that online conveyancing services are cheaper and offer the advantages of online case management and online document signing and verification which can speed up the process.

Once you’ve got a few conveyancing quotes from different firms, give them a ring to discuss how they work. Use our guide which lists the important questions to ask your conveyancing solicitor to cover the 10 key points you’ll want to know before proceeding.

Once you’ve instructed a conveyancing solicitor, they will undertake the relevant ID and Anti-Money Laundering checks. And they’ll write to your seller’s solicitor to confirm they are instructed and request a copy of the draft contract and any other details, such as the property’s title and the standard forms.

One of the first stages of the conveyancing process involves your solicitor examining the draft contract and supporting documents and raising enquiries with the seller’s solicitor. You will be expected to go through the paperwork and forms the seller has completed, including the TA6 form and TA10 form and let the solicitor know if you have any queries or concerns.

In particular, you will want to double check the tenure of your new home: is it leasehold or freehold? If you’re buying a leasehold property, see our guide on leasehold conveyancing and don’t rely solely on your solicitor to check for the length of the lease. This is a critical piece of information. Leases below 80 years can be a problem, can be costly to extend and you need to have owned the property for 2 years before you are eligible to do so. Leases under 60 years are best avoided.

When you’re buying a home, you’ll want the process to be as smooth as possible so make sure you respond promptly to queries and also ask for regular updates from your conveyancer and estate agent. Find more tips on keeping the conveyancing process on track in our guide on How to speed up conveyancing.

While it’s not a legal requirement, it’s a good idea to have a survey conducted. The survey report will highlight any major problems and may recommend extra investigations. What sort of survey you have done will depend on your specific circumstances. Depending on the results of the survey, you may want to go ahead with the purchase, renegotiate the price or even decide to pull out. So it’s a good idea to arrange your house survey at an early stage of the conveyancing process.

You can use our free tool to get instant quotes and find local Chartered Surveyors in your area:

Get instant house survey quotes from qualified surveyors in your area.

Once you’ve had a survey done, your conveyancing solicitor can advise on what to do next. Whether there are problems you want fixed before purchase or issues you want to investigate further, they can liaise with the sellers solicitor. If there are significant issues flagged up by the survey, you may want to renegotiate the price and your conveyancing solicitor will need to be looped in to get everything agreed in writing. See Red flags on a house survey: what to look for and what to do next.

There are things you may not know about the property just from viewing it with estate agents or even getting a survey. As part of the house conveyancing process, a conveyancing solicitor will do a set of legal property searches to ensure there are no other factors you should be aware of. Some searches will be recommended by the solicitor for all purchases and others will be required by the mortgage lender to protect them from any liabilities that the property may have.

These property searches include:

The cost of these property searches are often charged as extras, so make sure you factor them in to the conveyancing fees.

You will need to get your mortgage in place, which includes ensuring you have the financing available for a mortgage deposit.

As part of the process of getting a mortgage, you’ll need to get a mortgage valuation. This is carried out on behalf of the mortgage company so they know that the property you’re buying provides sufficient security for the loan. You normally have to pay for it, but a mortgage company might throw it in for free to attract business. But don’t let a free valuation sway you, it’s vital you pick the best mortgage for you. Our partners at award-winning brokers Mortgage Advice Bureau can help find you the best mortgage. Plus, unlike many brokers they don’t charge a fee so you could save even more.

Once the lender issues your mortgage offer, your solicitor will receive a copy of it and go through the conditions.

If you need a mortgage to buy the property, your lender will require you to get buildings insurance for your new home before exchange of contracts can take place. That’s because you are responsible for the property as soon as contracts have been exchanged. So shop around before you exchange to find the best policy at the best price. Get home insurance quotes now.

Since receiving the draft contract from the seller’s solicitor at the start of the house conveyancing process, your solicitor will have been in correspondence with you about what is covered. Before signing the contract your solicitor will need to ensure:

It’s a good idea to go to the property with the estate agent and the fixtures and fittings inventory list to ensure that everything you paid for is still there and the house has not been damaged in any way.

Get instant quotes from regulated and reviewed conveyancing solicitors that cover your area. Our customers save on average £490.

Exchanging contracts is one of the most important stages of the conveyancing process. You and the seller will agree on a date and time to exchange contracts. Your solicitor will exchange contracts for you, which is usually done by both conveyancing solicitors reading out the contracts over the phone (which is recorded) to make sure the contracts are identical, and then immediately sending them to one another in the post.

If you are in a housing chain your solicitor/conveyancer will do the same thing, but will only release it if the other people in the chain are all happy to go ahead. This means if one person pulls out or delays, then everyone in the chain gets held up.

Once you have exchanged contracts you will be in a legally binding contract to buy the property with a fixed date for moving. This means that:

You’re now in the final stages of the house conveyancing process. The period between exchange and completion involves your solicitor lodging an interest in the property, which will mean that the deeds to the property are frozen for 30 working days to allow your solicitor to process payment to the seller and lodge your application to the Land Registry to transfer the deeds into your name.

The seller may move out (although they may leave this to the day of completion).

You should get organised for your moving day and organise your removals company and broadband for your new home to ensure it’s set up on time for your moving-in day.

Get instant quotes from quality removal companies in your local area now

The solicitor will send you a statement showing the final figure to pay, which will need to be cleared into your solicitors bank account at least one day before completion. Your solicitor will apply to your mortgage lender for the mortgage loan.

Occasionally things can go wrong between exchange and completion resulting in delays.

Completion is normally set around midday on the specified date, although in practice takes place when the seller’s solicitor confirms that they have received all the money that is due. Once this happens, the seller should drop the keys at the estate agent for your collection. This means that the house conveyancing process is over, and you can move in.

After completion, your solicitor will tie up the last few stages of the house conveyancing process:

You will want to collect together all your paperwork from the purchase of your new home, including the estate agent’s brochure, to file away and keep safe for when you move again.

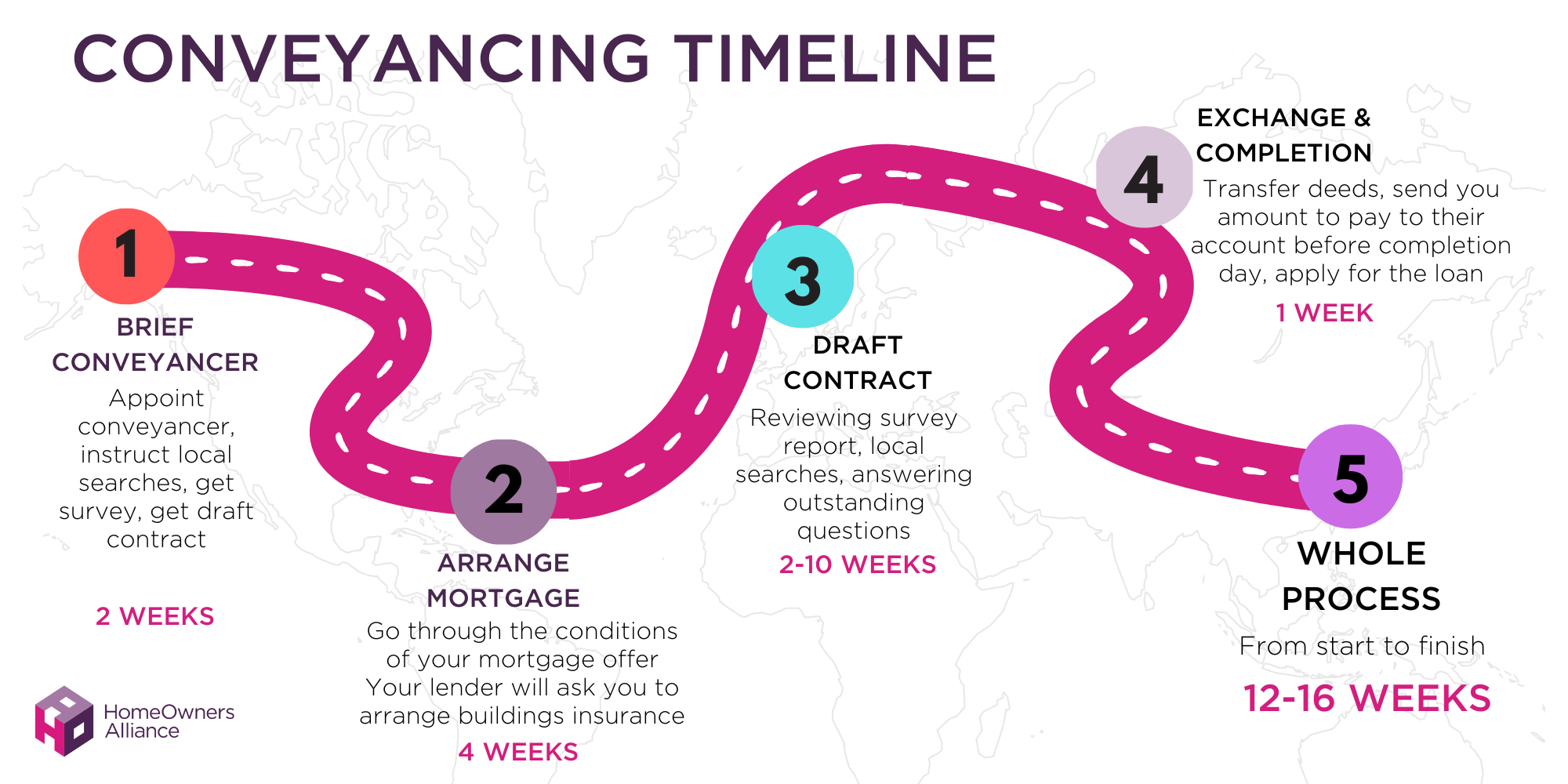

It takes on average 5 months in terms of the total length of time it takes to buy a house but can be shorter or longer depending on whether you are in a chain. The conveyancing process itself starts when you make an offer on a property – or accept an offer on your home – and lasts until completion day when keys for the property are exchanged. The conveyancing process may be shorter if you are a cash buyer. The conveyancing process takes around 12-16 weeks.

| Conveyancing Process Step | Approx Time |

| Pre contract work: appoint conveyancer, instruct local searches, get survey, get draft contract | 2 weeks |

| Time to arrange mortgage | 4 weeks |

| Draft contract: reviewing survey report, local searches, answering outstanding questions | 2-10 weeks |

| Time between exchange and completion | 1 week |

| Total time from an offer being accepted to completion | 12-16 weeks |

For full details, see our guide: how long does conveyancing take and further advice on how to speed up the conveyancing process.

Yes. If you’re buying a leasehold flat or house, there are additional steps to the leasehold conveyancing process. It will usually take longer because:

If you’re selling a house you’ll also want to know about the conveyancing process when selling. There are some stages of the conveyancing process for buyers that won’t apply to you. For example, you won’t need to apply for property searches. But there are some extra stages of the conveyancing process you’ll need to undertake, for example, you’ll be asked to complete a TA6 property information form, a TA10 fixtures and fittings form, and other forms, as well as collect together a number of documents required when selling. Find out everything you need to know in our guide Conveyancing process explained for sellers.

The first stage of the conveyancing process is finding the right solicitor or conveyancer and instructing them. You should shop around and compare conveyancing quotes to ensure you are getting the best service at the best price. It may take a few days to get the quotes in and make sure you’re comparing like for like, but it’s important you understand what you’re getting for your money. Once you have your quotes, give the firms a call to discuss anything you don’t understand and to ask how quickly hey can start.

It typically takes around 12-16 weeks, although it can take longer, for example, if there’s a delay on getting searches returned. And, the house conveyancing process may be shorter if you are a cash buyer. Take a look at our conveyancing timeline for more information.

This is a critical stage of the house buying process when the deal becomes legally binding. You’ll pay your deposit (about 10% of the purchase price) and the completion date will be set. The buyer is legally bound to buy and the seller to sell from this point. Have a look at our guide “What happens on exchange day?” for more information.

The buyer and seller should get the chance to agree the date of completion in advance, before they exchange contracts. Let your conveyancing solicitor and estate agent know as early as possible if there is a day you need to avoid or a date you have in mind for completion. If there is a chain, other parties will also be involved, making agreeing a date a bit trickier. See our guide for more information on what happens on completion day.

If you’re buying a property with a mortgage then it’s almost certain that the lender will insist that you use a conveyancer or solicitor to do the legal work. If you don’t need a mortgage to buy a property, it is possible to do the stages of the conveyancing process yourself but it can be complicated, comes with financial and legal risks and is time-consuming. For what to expect see our guide to solicitors fees when buying.

A draft contract is drawn up by the seller’s conveyancer when an offer is made on a property. It’s draft because it isn’t final and legally binding until it is agreed at exchange. It must include details such as the names of the buyer and seller and the price. As the conveyancing process progresses more information may be added to the contract ahead of exchange. For example, there may be changes to the terms or the agreed sale price as a result of the findings of the enquiries carried out by the buyer’s conveyancer.

A property survey is an inspection of a property’s condition conducted by a surveyor and will tell you if there are any issues to do with the state of the property from minor issues to significant structural problems. The detail the report goes into will depend on the type of survey you get. Find out more about house survey types in our guide House survey types and costs.

There are a number of steps in the house conveyancing process but they are all important to protect you. For example, ID and proof of funds checks are required so the solicitor knows you and the seller are who you say you are and that the funds come from a legitimate source. While local searches ensure you are aware of any issues that may have an affect on the property and your enjoyment of it.

If you’re considering using the solicitor recommended by the estate agent you’re buying the house through, we’d advise you compare conveyancing quotes first to check you’re getting a good deal. You’re not obliged to use the conveyancer the estate agent recommends and you may get a better service for a better price by shopping around. See our guide on why you might want to think twice before simply appointing the estate agents recommended solicitor.

Yes. Read our guide on New Build Conveyancing for why the new build process is often the most complicated, and what’s involved. And don’t simply appoint the developer’s recommended solicitor. With so many pitfalls to avoid – from non compliance with planning regulations to incomplete agreements for roads and sewers – you’ll want to make sure the solicitor works in your best interests only. Our guide on why you should avoid the developer’s conveyancing solicitor gives more details and explains what to do if you feel a victim of pressurised selling tactics.

Yes, the process of buying and selling a house is different in Scotland. So make sure you use a conveyancer that is experienced in the house conveyancing process in Scotland.

Choosing a conveyancing solicitor that uses an online conveyancing system can be cheaper and should speed things up. To find out more on the pros and cons read should I do my conveyancing online? With some online systems you can verify ID online, sign documents digitally and get real-time updates.

If you’re buying a house you’ll need to budget for solicitor fees: the average cost in the UK is £1,474. There are ways to cut your solicitors fees when buying a house. See our guide for our top tips.

HomeOwners Alliance Ltd is registered in England, company number 07861605. Information provided on HomeOwners Alliance is not intended as a recommendation or financial advice.

HomeOwners Alliance Ltd is an Introducer Appointed Representative of Mortgage Advice Bureau (Derby) Limited which is authorised and regulated by the Financial Conduct Authority.

HomeOwners Alliance Ltd is an Introducer Appointed Representative (IAR) of LifeSearch Limited, an Appointed Representative of LifeSearch Partners Ltd, authorised and regulated by the Financial Conduct Authority. (FRN: 656479).

Independent Financial Adviser service is provided by Unbiased, who match you to a fully regulated, independent financial adviser, with no charge to you for the referral.

HomeOwners Alliance Ltd is an Introducer Appointed Representative (IAR) of Fluent Money Limited, which is authorised and regulated by the Financial Conduct Authority. Calls may be monitored/recorded.

If you take out a mortgage or protection product through Mortgage Advice Bureau, they pay us a referral fee of 25%. You are not obliged to use their services.