Find the best estate agent near you Start here

Conveyancing is the process of legally transferring home ownership from you, the seller, to the buyer. It starts from accepting an offer and finishes when you hand over the keys to the buyer. We explain all of the legal stages in the conveyancing process when selling -- the conveyancing steps and the conveyancing process timeline.

Regardless of whether you’re selling or buying, it’s a solicitor or conveyancer who usually conducts the conveyancing process.

Both solicitors and licensed conveyancers manage the conveyancing process—the legal transfer of property ownership from the seller to the buyer. The main difference between a solicitor and a conveyancer is that a conveyancer is a specialist in property law whereas a solicitor is a fully qualified lawyer who can offer full legal services such as divorce proceedings or taking someone to court. Licensed conveyancers are usually cheaper.

This guide explains the steps in the conveyancing process when you are selling. If you are also buying, see our guide which explains the conveyancing process for buyers.

The first step in the conveyancing process for sellers is to instruct your conveyancing solicitor.

Once you have accepted an offer, you need to formally instruct your solicitor or conveyancer to begin the conveyancing process to allow the sale to progress effectively.

To reduce delays and speed up the conveyancing process, it’s probably best to choose which solicitor or conveyancer you want to use before you are under offer, around the time you choose your estate agent.

To help you choose your conveyancing solicitor for your house sale, see our advice guides on what conveyancing and solicitor fees to expect when selling, and compare quotes.

Get instant quotes from regulated and reviewed conveyancing solicitors that cover your area. Our customers save on average £490.

The next step in the conveyancing process for sellers, before the exchange of contracts, involves completing a number of detailed questionnaires about the property and what you intend to include with the sale, which will be provided to you by your solicitor/conveyancer. Ahead of completing the questionnaires, it’s a good idea to dig out documents you will need when selling your house.

You may be asked to complete:

You, the seller, must fill these forms out truthfully and to the best of your knowledge; if it later transpires that you have not been fully truthful you could be sued for compensation. Or, if they find out before exchange of contracts, it might make the buyers nervous that you are misleading them about other things and they may pull out.

Your solicitor/conveyancer will use the questionnaire information to draw up a draft contract. This is sent to the buyer for approval.

The conveyancing solicitor will lead negotiations over the draft contract. Things to agree include:

Before you can exchange contracts, you need to pay off your mortgage, by requesting a redemption figure from your mortgage company. This is how much you pay upon completion of the sale.

You and the buyer will have agreed on a date and time to exchange contracts. As part of the conveyancing process, your solicitor or conveyancer will exchange contracts for you. This is usually done by both solicitors/conveyancers making sure the contracts are identical, and then immediately sending them to one another in the post

If you or the buyers are in a chain, the solicitors/conveyancers will do the same thing, but will only release it if the other people in the chain are all happy to go ahead. This means if one person pulls out or delays, then everyone in the chain gets held up. For more, see how can I break the housing chain?

Once you’ve exchanged contracts, you will be in a legally binding contract to sell the property. This means that if the buyer does not complete the purchase, you will probably keep their deposit, and you can also sue them. If you pull out of the sale, they can sue you. Exchanging contracts also means that you can no longer accept another offer on your house.

Immediately after exchange you should receive the buyer’s deposit – usually 10% of the property price. Legally, you own the property until completion, and so there is no need to move out before then. However, it will be a lot less stressful if you can move out some days before, rather than leaving it to the last minute.

This is a good time to organise your move and get removals quotes and organise your removals company if you are using one.

You should go around the property before you complete, ensuring that everything that was on the fixtures and fittings inventory list is still in the property.

Occasionally things go wrong between exchange and completion – see our guide for more advice.

On completion day you will hand over the keys. In practice, the buyer normally gets the keys from the estate agent, and you leave any spare sets you have in the property.

You or your conveyancer/solicitor will receive the outstanding balance of the sale price, hand over the legal documents that prove ownership and pay off the mortgage with the proceeds of the sale.

You will have to pay your solicitor/conveyancer and the estate agent.

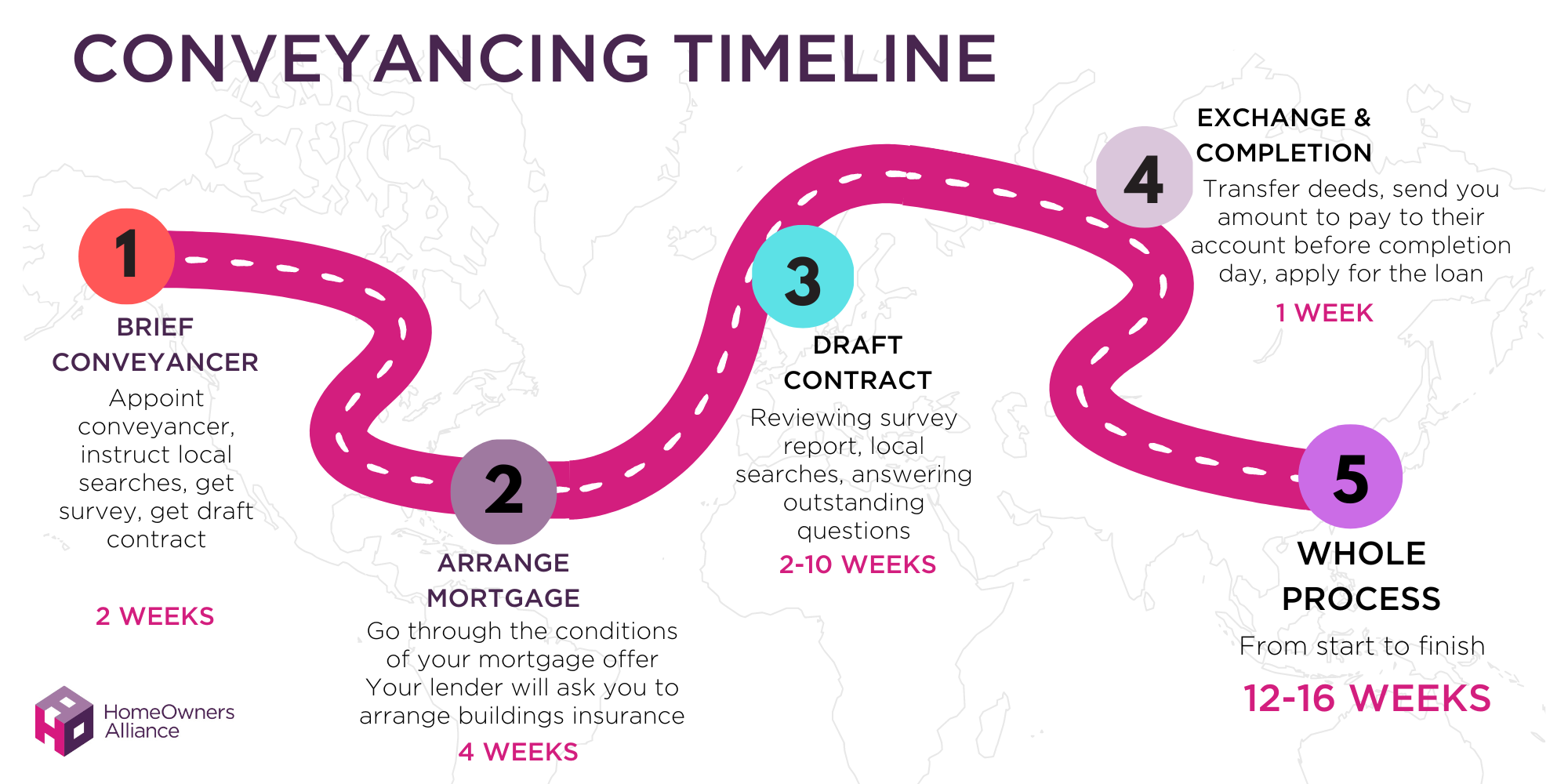

The conveyancing process when you are selling starts when you accept an offer on your home – and lasts until completion day when keys for the property are exchanged. The conveyancing process takes around 12-16 weeks.

| CONVEYANCING PROCESS – SELLING | APPROX TIME |

|---|---|

| Pre contract work: appoint conveyancer, instruct local searches, get survey, get draft contract | 2 weeks |

| Time for buyer to arrange mortgage | 4 weeks |

| Draft contract: reviewing survey report, local searches, answering outstanding questions | 2-10 weeks |

| Time between exchange and completion | 1 week |

| Total time from an offer being accepted to completion | 12-16 weeks |

For full details, see our guide: how long does conveyancing take

Get instant quotes from regulated and reviewed conveyancing solicitors that cover your area.

HomeOwners Alliance Ltd is registered in England, company number 07861605. Information provided on HomeOwners Alliance is not intended as a recommendation or financial advice.

Mortgage service provided by London & Country Mortgages (L&C), Unit 26 (2.06), Newark Works, 2 Foundry Lane, Bath BA2 3GZ, authorised and regulated by the Financial Conduct Authority (FRN: 143002). The FCA does not regulate most Buy to Let mortgages. Your home or property may be repossessed if you do not keep up repayments on your mortgage.

HomeOwners Alliance Ltd is an Introducer Appointed Representative (IAR) of LifeSearch Limited, an Appointed Representative of LifeSearch Partners Ltd, authorised and regulated by the Financial Conduct Authority. (FRN: 656479).

Independent Financial Adviser service is provided by Unbiased, who match you to a fully regulated, independent financial adviser, with no charge to you for the referral.

Bridging Loan and specialist lending service provided by Chartwell Funding Limited, registered office 5 Badminton Court, Station Road, Yate, Bristol, BS37 5HZ, authorised and regulated by the Financial Conduct Authority (FRN: 458223). Your property may be repossessed if you do not keep up repayments on a mortgage or any debt secured on it.