Find the best estate agent near you Start here

Buying a house on your own can feel overwhelming - but you’re not alone. Nearly half of first time buyers in the UK bought a home on their own last year. Whether you’re single by choice or circumstance, getting a mortgage solo is now more common than ever.

Yes, you can get a mortgage on your own. The key difference compared to if you’re buying with someone else is that your borrowing power is based on one income, not two. This can affect:

Read on for more on these. But single person mortgages are not unusual. In fact, 47% of first time buyers bought a property on their own in 2024, research by Mortgage Advice Bureau found.

KEY INFORMATION

Lenders will usually lend up to 5 times your income.

Although, some of the best mortgage lenders will lend up to 6x your income, depending on your circumstances. So if you earn £50,000 you may be able to borrow up to £300,000.

However, lenders will also assess your affordability when deciding how much to lend. This takes into account household spending each month, such as:

To get tailored advice on how much you can borrow on a single person mortgage, the easiest course of action is to speak to a mortgage broker.

Get fee free mortgage advice from our partners at L&C. Use the online mortgage finder or speak to an advisor today.

If you think you can’t borrow enough on a mortgage to buy a house because of what you’ve been told in the past, it’s worth trying again:

You’ll usually need at least a 5% deposit to get a mortgage, this is the same as if you’re buying with someone else.

And the bigger the deposit you have, the bigger the choice of mortgages you will have. You’ll usually get access to better mortgage rates too.

In fact, the average deposit first time buyers paid in 2024 was £61,090 with deposits averaging 20% of the purchase price, according to Halifax. First time buyers in London paid an average deposit of £124,688.

Here’s an illustration of how much deposit you’ll need for different deposit levels, based on buying a £200,000 house.

| Deposit % | Deposit £ |

|---|---|

| 5% | £10,000 |

| 10% | £20,000 |

| 25% | £50,000 |

Yes, it’s possible to buy a house on your own with no deposit by taking out a 100% mortgage. We explain all your options and what to consider in our guide on how to get a mortgage with no deposit.

Find out about 0% deposit single person mortgages with fee-free mortgage brokers L&C.

If getting a big enough mortgage to buy a house on your own is proving difficult, there are some schemes designed to help you.

You’ll want to avoid these pitfalls if you’re trying to boost your chances of getting a single person mortgage.

Lenders will check your credit report. If you’ve got a history of bad credit, you may be able to borrow less and at higher rates. So it’s important to improve your credit score as much as possible before applying for a mortgage. Read our guide on 11 tips to improve your credit score for a mortgage.

Lenders will also consider your debt-to-income ratio, which is your monthly debt repayments (mortgage, loans, credit cards etc) compared to your gross monthly salary.

Your debt-to-income ratio is an important part of your overall mortgage affordability, since your monthly expenses include debt repayments. If you can reduce this, you could improve your affordability. Ultimately, however, lenders want to see that you’re managing your debt confidently, not missing payments, and not struggling to make ends-meet.

You’ll usually need at least a 5% deposit to get a mortgage but the bigger your deposit, the more options you will have. Having a bigger deposit usually means you’ll get access to better mortgage rates too.

Lenders will go through your outgoings when deciding how much to lend to you. So slash your unnecessary spending in the months before applying for a mortgage.

If you’re buying a house on your own, it’s critical to consider how you’d pay your mortgage if you had an accident or were too unwell to work. And if you’ve got anyone relying you financially, think about how they’d cope financially if you pass away.

Despite the benefits of these policies, new research from LifeSearch and HomeOwners Alliance reveals 36% of mortgage holders in the UK have no form of life insurance, income protection, or critical illness cover – equating to roughly 2.34 million* mortgage holders nationwide.

The research also found women were more vulnerable to sudden income loss than men:14% of women say they’d fall behind on mortgage payments immediately if their income stopped due to illness or injury, compared to just 6% of men.

If you’re applying for a single person mortgage, it’s crucial that you apply to the right lender. The easiest way to make sure you do this is by speaking to a fee-free mortgage broker. They’ll know each lender’s different lending criteria and will be able to match you to the lender most likely to accept your mortgage application.

Get fee free mortgage advice from our partners at L&C. Use the online mortgage finder or speak to an advisor today.

If you’re struggling to get a big enough mortgage on your own with a standard mortgage, there may be other options for you, such as:

Get fee free mortgage advice from our partners at L&C. Use the online mortgage finder or speak to an advisor today.

Here’s a step by step guide to getting a single person mortgage

The bigger your deposit, the easier you may find it to buy a house. If you haven’t done so already, you may want to consider a Lifetime ISA.

And can you get support from your family? Getting a gifted deposits can make buying a home much easier.

Getting expert advice means you’ll understand how much you may be able to borrow if you take out a mortgage on your own.

They’ll also explain different mortgage types available and how much your monthly repayments will be.

There are lots of documents you’ll need to provide in the mortgage application process so start gathering them up. These may include:

Once you have shopped around for the best mortgage deal, see if you will qualify by getting a mortgage in principle, sometimes called an agreement in principle (AiP) or decision in principle (DiP). This is a statement from a lender on how much they would lend you ‘in principle’ based on information you’ve provided about your income and outgoings.

Getting a mortgage in principle as early in the process as possible is advisable, ideally before you start house-hunting.

You can get a Mortgage in Principle in just a few minutes with this Mortgage Finder powered by the mortgage experts at L&C.

Once you’ve found a property and had an offer accepted, you can start the formal mortgage application process. Your mortgage broker can take this forward for you. The lender will carry out a full credit check, undertake a mortgage valuation of the property and once happy with your application will issue a formal mortgage offer.

It can be harder for some people to get a mortgage as a single person as the lender will assess affordability on one income instead of two. And you may find it harder to save a deposit on your own.

But there’s no one size fits all for mortgages. The best course of action is to speak to a fee-free mortgage broker who can explain your mortgage options to you if you want to buy a house on your own.

Get fee free mortgage advice from our partners at L&C. Use the online mortgage finder or speak to an advisor today.

Having bad credit doesn’t mean you can’t get a mortgage. But it’s important to get expert mortgage advice first to make sure you apply to the right lender.

If your credit issues were fairly minor, a mainstream lender may lend to you. But if your situation is more complex, you may need to go to a specialist bad credit mortgages lender.

Using the right specialist mortgage broker is crucial. Our partners at Chartwell Funding will check whether a High Street lender is the best option for you first. Whereas some specialist mortgage brokers will only look at impaired credit lenders – this could mean you have to pay a higher mortgage rate. Read more in our guide on Bad credit mortgages.

If you’re buying a house on your own you’ll also need to factor in the additional costs you’ll need to pay, including:

Use our stamp duty calculator to work out how much you’ll need to pay

Based on buying an averagely priced property, the estimated cost to buy a house can be broken down as follows.

| Costs of Buying a House | Estimate |

|---|---|

| Stamp duty | £4,600 |

| Building Survey | £650 |

| Conveyancing | £1,050 |

| Mortgage fees | £1000 |

| Mortgage valuation fees | £150 |

| Homebuyers Protection Insurance | £74 |

| Buying Total | £7,519 |

| General moving house costs | Estimate |

|---|---|

| Removals | £550 |

| Mail redirection | £39.50 |

| General moving costs total | £589.50 |

Total average cost to buy a house is £8,108

Find out more in our guide on The costs of buying a house.

The size of deposit required doesn’t change if you’re applying by yourself. So you’ll need at least a 5% deposit, unless you’re applying for a 100% mortgage.

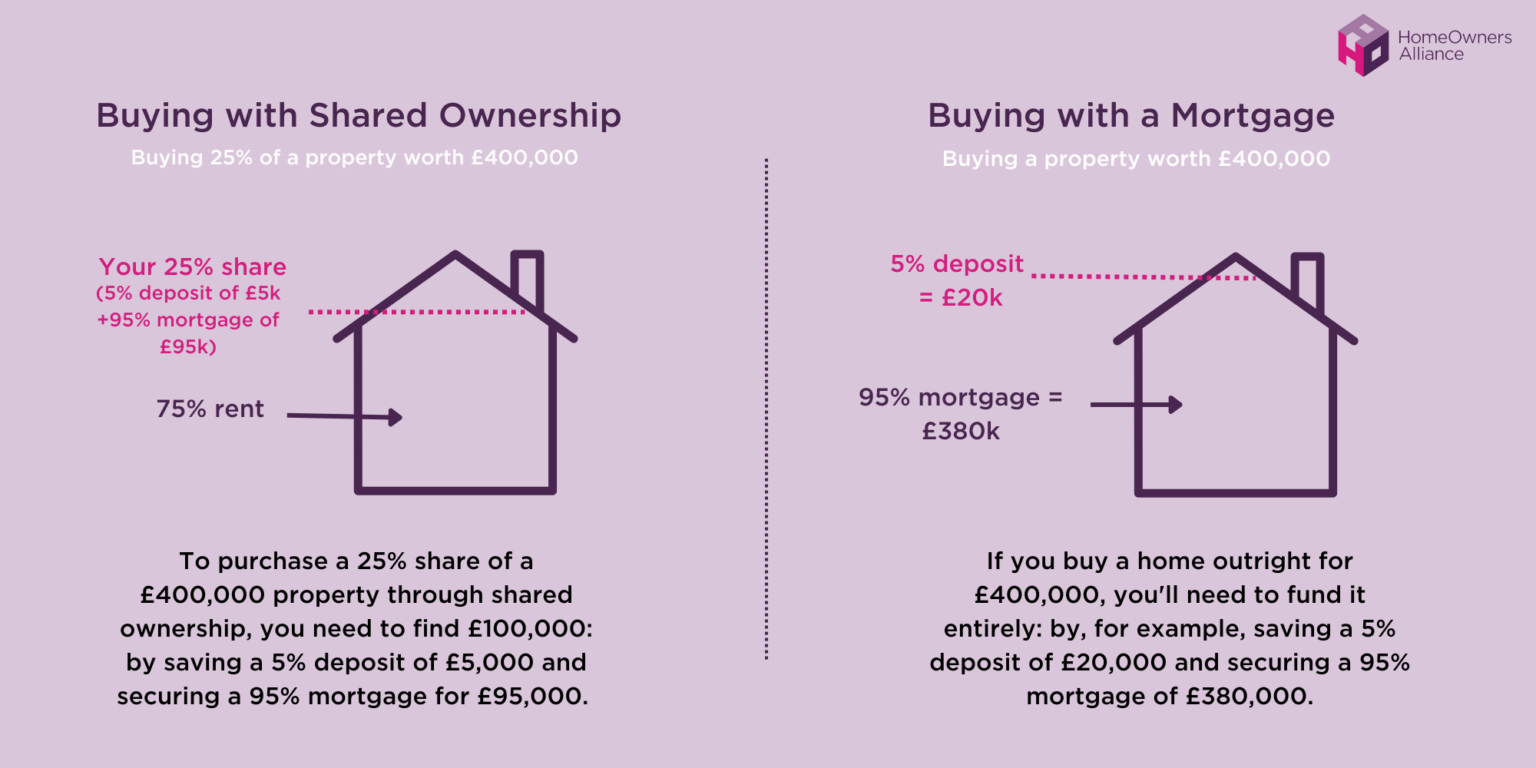

If you’re eligible to apply for the shared ownership scheme you can apply as a single person.

To remove your partner’s name from a joint mortgage they must also be removed from the title deeds, this involves applying for a “transfer of equity”. However, in order to agree to this, your lender will want to be confident that you can afford the mortgage on a single income instead of the previous two. Read more in Who gets the house in a divorce?

There are lots of documents you’ll need to provide in the mortgage application including:

– Proof of ID like a passport or driving licence

– Your last three months’ payslips and most recent P60.

– Bank statements of your current account for the last three to six months

– Statement of two to three years’ accounts from an accountant if self-employed

Yes, mortgage lenders typically check your bank statements as part of the mortgage application process. This is to verify your income, assess your ability to afford the mortgage payments and to see your spending habits.

A six times income mortgage is when a lender agrees to lend you six times your annual salary. Most lenders offer up to 5 times your salary but some lenders will offer 6 times your income, depending on your circumstances. Read more in our guide to the Best Mortgage Lenders.

HomeOwners Alliance Ltd is registered in England, company number 07861605. Information provided on HomeOwners Alliance is not intended as a recommendation or financial advice.

Mortgage service provided by London & Country Mortgages (L&C), Unit 26 (2.06), Newark Works, 2 Foundry Lane, Bath BA2 3GZ, authorised and regulated by the Financial Conduct Authority (FRN: 143002). The FCA does not regulate most Buy to Let mortgages. Your home or property may be repossessed if you do not keep up repayments on your mortgage.

HomeOwners Alliance Ltd is an Introducer Appointed Representative (IAR) of LifeSearch Limited, an Appointed Representative of LifeSearch Partners Ltd, authorised and regulated by the Financial Conduct Authority. (FRN: 656479).

Independent Financial Adviser service is provided by Unbiased, who match you to a fully regulated, independent financial adviser, with no charge to you for the referral.

Bridging Loan and specialist lending service provided by Chartwell Funding Limited, registered office 5 Badminton Court, Station Road, Yate, Bristol, BS37 5HZ, authorised and regulated by the Financial Conduct Authority (FRN: 458223). Your property may be repossessed if you do not keep up repayments on a mortgage or any debt secured on it.

{kind=link}