Find your best local estate agent Start here

There are literally thousands of different types of mortgages on the market, and choosing one can be daunting. But before deciding which mortgage to go for, you need to decide what type of mortgage to get – repayment, interest only, fixed, tracker or discounted. Which one is right for you depends on your circumstances.

Choosing the right type of mortgage is incredibly important – and getting it wrong can cost you a lot of money. Narrowing down the mortgage type that is best suited to your finances will help you to choose a lender and a mortgage product. We explain the different types of mortgage options and what to consider with each to help you find the best type of mortgage for you.

Repayment mortgages are when you repay the interest and the equity of the house each month. In contrast, an interest-only mortgage is when you repay the interest and then pay-off the equity at the end of the term.

For the vast majority, a repayment mortgage is the most appropriate choice – they guarantee you are paying off your debt, and ensure you will have repaid the mortgage at the end of its term.

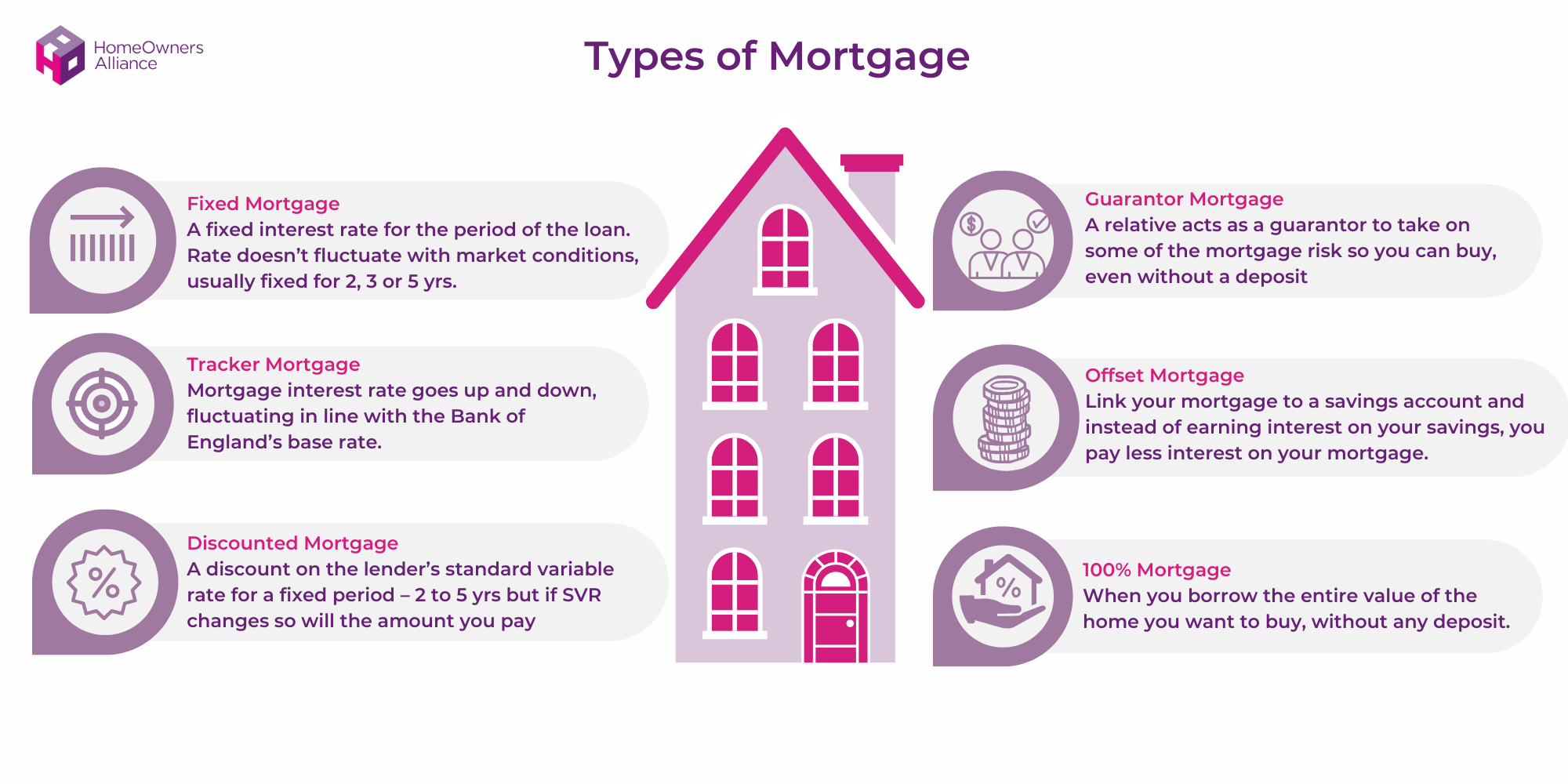

A fixed rate mortgage is when the rate is fixed for a set number of years, after which it reverts to the lender’s standard variable rate. More than 60% of homeowners chose a fixed rate mortgage in 2019, according to a survey conducted by Which.

Fixed rate mortgages are a popular option, because you know exactly what your monthly repayments will look like over a set period. You are shielded from any increases in interest rates by the Bank of England during your fixed rate period.

However – you may pay more for a fixed rate mortgage than you would with a variable rate mortgage and you won’t benefit if interest rates fall – so you could be trapped in a higher rate mortgage. You also limit your ability to remortgage, as fixed rate mortgages almost always come with early redemption fees.

If you do decide to go for a fixed rate mortgage to guarantee your mortgage costs, you need to decide the term of it – normally two, three or five years.

Going with a five-year fixed mortgage will give you greater certainty, and can be appealing for people in stable but financially stretched circumstances who want to minimise any financial risks. But a lot can happen to your circumstances in five years, and you may end up feeling trapped by a longer term. Also, in five years your income may have increased, making any mortgage increases far more affordable.

Similarly, the huge expenses involved in moving house – such as buying furniture and building work – will normally be behind you after two or three years, giving you greater capacity for coping with changes in interest rates.

For these reasons, choosing to fix your mortgage for two or three years is recommended. And don’t forget that at the end of the term, you can always remortgage and move on to another fixed deal if you want to.

Although 25 years is the most common term chosen for mortgages but some stretch to 40 years, it’s important to remember that you can choose whatever term you feel comfortable with. More people are opting for 30 year mortgages to lower their monthly repayments as the debt is spread over more years which makes the mortgage more affordable day to day. However, it also means you’ll pay more interest over the life of your mortgage. See our guide on 30 year mortgages to weigh up the pros and cons of a longer mortgage term.

A tracker mortgage goes up and down with the Bank of England’s base rate. For example, you can have a tracker that is base rate plus 2%, meaning the interest you pay will always be 2% above the Bank of England base rate.

Tracker rates can be for the entire length of the mortgage, or just for an introductory period (between two and five years) after which the rates revert to the lender’s standard variable rate (which is invariably a lot more expensive).

This type of mortgage can sometimes present the best value option. It’s also the most transparent – you know that if the base rate increases by 0.25%, so will your repayments. On the other hand, if the base rate falls, anyone on a tracker mortgage will see their repayments fall too. This is important, because lenders have been accused of not passing on discounts to customers on standard variable mortgages when the base rate has fallen in the past.

However, because the base rate can change, a tracker mortgage is still unpredictable. If you’re on a tight budget, you may prefer to choose a fixed rate mortgage instead.

You should never choose a standard variable rate mortgage. They are the worst value mortgages on the market because they give lenders the total freedom to charge however much they want to.

Most people will end up on a standard variable rate mortgage because their existing mortgage deal has run out. Lenders rely on the inertia of homeowners to keep them on this type of mortgage once they have ended up on it.

You should consider remortgaging if you’re on a SVR – because there’s a high likelihood that you could save yourself some money.

A discounted mortgage is offered by lenders that want to attract you to their more expensive SVR by dropping their rates temporarily. The discount will be offered for an introductory period – usually between two and five years – after which you’ll be back on their more pricey mortgage.

If you’re struggling with the initially high costs of home ownership in the first few years of buying, a discounted mortgage can help significantly – but you need to consider whether this is the right option or if fixing your rates would be better. It’s also possible to find a discounted tracker mortgage, which can be very competitive.

If you choose a discounted mortgage, you need to be careful about what happens when the introductory period ends. It’s important to understand if and when you can remortgage, and anticipate how much your monthly repayments could increase by so that you are clear on what you can afford in the future.

Get fee free mortgage advice from our partners at L&C. Use the online mortgage finder or speak to an advisor today.

An offset mortgage is when your lender takes into account how much you have in a savings account with them, and knocks that amount off the debt that they charge interest on. For example, if you have £10,000 in savings, and a £100,000 mortgage, you would only pay interest on £90,000.

This type of mortgage can help you to reduce the amount of interest you pay on your loan. It also gives you the flexibility to pay off more of the mortgage when you have more money, but then to reduce your payments when you need a bit more to spend.

The downside of an offset mortgage is that you won’t earn interest on the savings that you have with the lender. They also tend to have slightly higher interest rates. Find out more about offset mortgages, the pros and cons and how they work.

Many mortgage companies have special deals for first time buyers, which are generally aimed at helping people get on the property ladder. These types of mortgages usually accommodate having lower deposits (ie the ratio of the mortgage to the value of the property can be higher) and have lower application fees.

These mortgages are often discounted as well, to make the early years cheaper (but you may pay it back later). In general, first time buyer mortgages can be very helpful at a difficult time – but do still check out the rest of the market in case there are some particularly good deals.

A guarantor mortgage is when a relative acts as a guarantor and agrees to make the mortgage repayments if you can’t. You can usually borrow a larger amount than you would be able to on your own. In fact some guarantor mortgages will let you borrow 100% of the property’s value.

If this is your first mortgage, see our steps to your first mortgage guide and, if your parents may be in a financial position to help you, see The Bank of Mum and Dad – how to help your child buy a home. We also have more information on how guarantor mortgages work, the risks and popular options such as Barclays Family Springboard.

Green mortgages reward you for saving energy in your property. Some lenders will give you lower interest rates or cashback and larger loans if your home meets a minimum energy-efficiency level. Other mortgage lenders will offer lower rates or cashback if you make energy-efficiency improvements. Or if you take out additional borrowing to pay for measures to improve your home’s energy efficiency. There are a number of lenders already offering green mortgages including Nationwide, Natwest, Barclays, Kensington and Saffron Building Society and more.

| Mortgage types | Pros | Cons |

|---|---|---|

| Fixed rate mortgage |

|

|

| Tracker mortgage |

|

|

| Standard variable rate mortgage |

|

|

| Discount mortgage |

|

|

| Offset mortgage |

|

|

| First Time Buyer mortgage |

|

|

| Guarantor mortgage |

|

|

| 100% mortgage |

|

|

| Green mortgage |

|

|

Mortgage lenders generally calculate the amount of interest you are due to pay daily, monthly or annually. It seems like a very detailed point, but understanding this will protect you from unfair lenders that may rely on borrowers’ confusion to make interest calculations that are blatantly unfair and add many thousands of pounds to a cost of a mortgage.

Without hesitation you should go for daily calculation, and avoid any mortgage with annual calculation.

With annual interest calculation, the lender will calculate the interest rate once for the entire year – and you risk being charged interest on debts you’ve already repaid. For example, if your interest rate is calculated on January 1st, and you pay off £5,000 on January 2nd, you’ll still be charged interest as if that payment never happened. It’s legal, but it is morally questionable and should be avoided at all costs.

Building societies are owned by their customers, which means they don’t have to pay regular dividends to shareholders. They claim this means they can give better value for money, and while it may be true, it’s no guarantee that a building society will have the best mortgage for you.

The secret to finding the best mortgage is a three-pronged approach:

HomeOwners Alliance Ltd is registered in England, company number 07861605. Information provided on HomeOwners Alliance is not intended as a recommendation or financial advice.

Mortgage service provided by London & Country Mortgages (L&C), Unit 26 (2.06), Newark Works, 2 Foundry Lane, Bath BA2 3GZ, authorised and regulated by the Financial Conduct Authority (FRN: 143002). The FCA does not regulate most Buy to Let mortgages. Your home or property may be repossessed if you do not keep up repayments on your mortgage.

HomeOwners Alliance Ltd is an Introducer Appointed Representative (IAR) of LifeSearch Limited, an Appointed Representative of LifeSearch Partners Ltd, authorised and regulated by the Financial Conduct Authority. (FRN: 656479).

Independent Financial Adviser service is provided by Unbiased, who match you to a fully regulated, independent financial adviser, with no charge to you for the referral.

Bridging Loan and specialist lending service provided by Chartwell Funding Limited, registered office 5 Badminton Court, Station Road, Yate, Bristol, BS37 5HZ, authorised and regulated by the Financial Conduct Authority (FRN: 458223). Your property may be repossessed if you do not keep up repayments on a mortgage or any debt secured on it.