Find the best estate agent near you Start here

We take a look at conveyancing fees and what you can expect to pay in 2026.

KEY INFORMATION

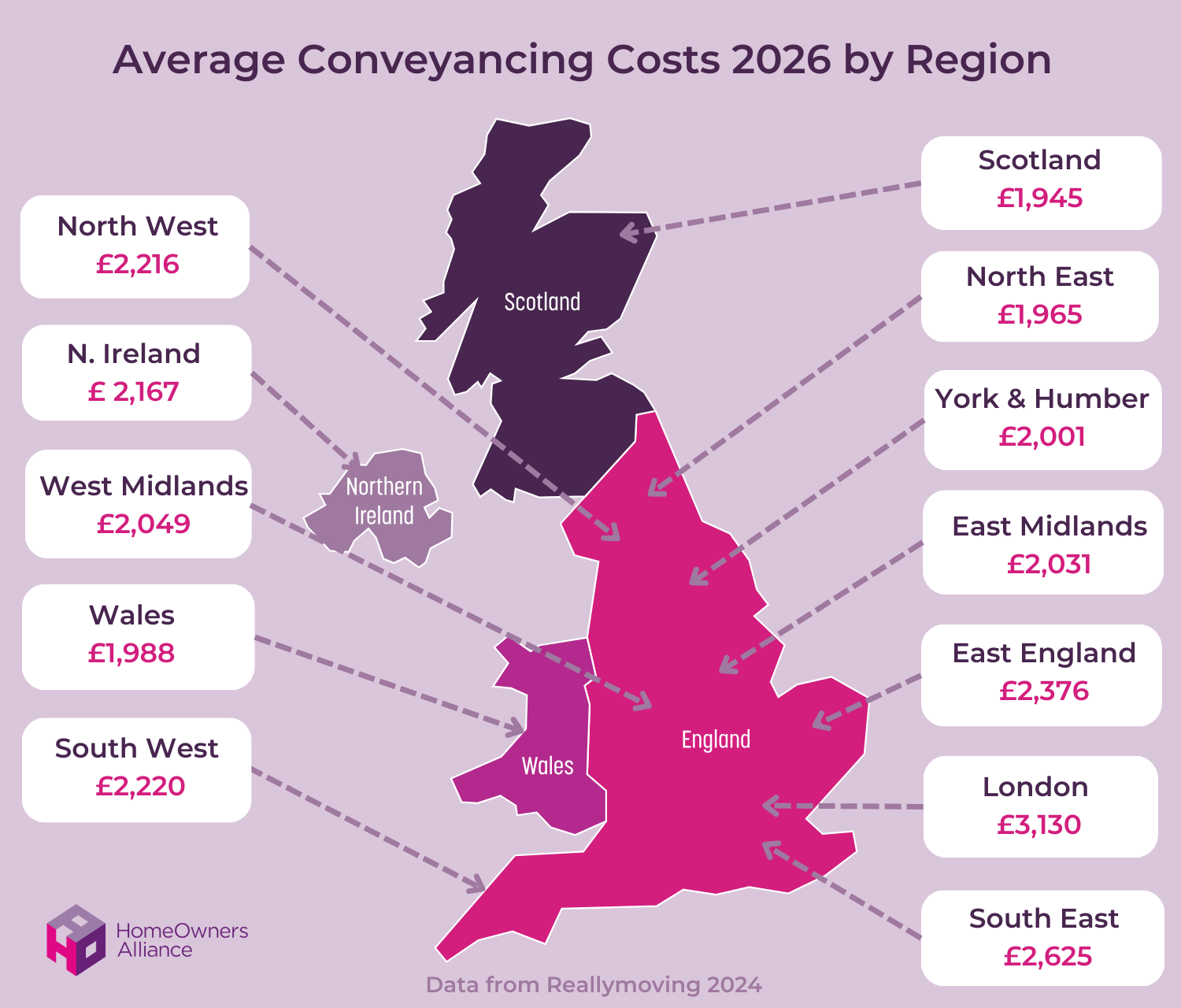

The image below shows how average conveyancing fees for buying and selling a home, including disbursements and expenses, vary by region. The data is based on analysis of approximately 34,000 conveyancing quote forms from our partners at Reallymoving.

To get an accurate idea of conveyancing costs for your purchase or sale, use our conveyancing fees calculator to instantly compare conveyancing quotes.

Conveyancing fees cover the amount you’ll pay to make sure the legal side of buying or selling a house is handled correctly. Conveyancing or Solicitor fees can be split into two parts:

Some conveyancing fees apply to sellers only while some only need to be paid by buyers.

The amount you’ll pay for the legal fee portion of your conveyancing fees varies due to a number of factors including:

You can compare conveyancing quotes now with our conveyancing fees calculator.

Get instant quotes from regulated and reviewed conveyancing solicitors that cover your area. Our customers save on average £490.

These are the typical costs for disbursements you can expect to pay. These costs are in addition to the legal fees:

The best way to get an idea of the cost of conveyancing is to compare conveyancing quotes. Use our free tool for instant results:

Get instant quotes from regulated and reviewed conveyancing solicitors that cover your area. Our customers save on average £490.

To get an idea of how much typical conveyancing fees are, see our table summarising the disbursements you’re likely to need when you’re buying and selling a house and their typical costs.

| Fee | What it’s for | Amount | Buying | Selling |

|---|---|---|---|---|

| Anti-money laundering checks | Legal checks to verify your identity | £6 – £20 | ✔ | ✔ |

| Bankruptcy search | This verifies if the buyer is bankrupt or about to be bankrupt | £4 | ✔ | |

| Title deeds copy | Proves the seller owns the property and has the right to sell it | £10 | – | ✔ |

| Local authority searches | These can identify potential issues with the property | £250 – £450 | ✔ | – |

| Property fraud check | Confirms the lawyer you’re sending money to is a real company | £10 | ✔ | – |

| Transferring of ownership | You have to pay the Land Registry a fee for transferring your name to your buyer’s on completion | £200 – £300 | – | ✔ |

| Bank transfer fees | You’ll pay the bank’s telegraphic transfer fee to guarantee funds reach an account on a certain day. Plus, your solicitor will charge a fee for performing the transfer. | £20 – £30 | ✔ | – |

| Stamp Duty Land Tax | You’ll need to pay this tax if you buy a property over £125,000. It’s charged on a sliding scale and the rules are different for first time buyers and Buy to Lets. | 0 – 17% | ✔ | – |

| Gifted deposit | Those getting a gifted deposit will likely need to pay more to cover the paperwork proving the money comes from a legitimate source. | £50 – £100 | ✔ | – |

| Lifetime/Help to Buy ISA | This covers the extra work for your conveyancer to redeem your ISA bonus | £60 | ✔ | – |

| Unregistered property supplement | If the property is unregistered it involves extra work for the conveyance. This fee covers the work. | £120 – £240 | ✔ | – |

| Leasehold property supplement fee | This covers the additional work required if you’re buying a leasehold property. | £200 – £300 | ✔ | – |

| Managing Agent packs | If you’re selling a leasehold property, this summarises the lease. | £300 – £800 | – | ✔ |

| Average legal fees | This is what the solicitor or conveyancer charges for doing their work. | Between £300 to £1500 |

Some of the main factors influencing conveyancing fees are:

The most common associated costs have been listed above, however there are occasions when you may need to pay for other fees. One example is that if a seller doesn’t have a FENSA or building regulation certificate for their double glazed windows, an insurance policy may be needed. This is known as indemnity insurance and you can normally negotiate who pays.

The conveyancing fees for leasehold properties will be much higher, as there are likely to be additional costs. You’ll usually need to pay around an extra £300 in legal fees and you may also need to pay for a Deed of Covenant, for example, which is a legally binding agreement between the buyer and landlord or management company about factors such as carrying out repair work.

Other work could include additional investigations into the length of the lease as well as liaising with the landlord to serve notices on them or the managing agent.

While sellers will have to pay for the Leasehold Management Pack which contains information about services charges etc. The cost for this can vary significantly from £300 to as much as £800.

And you’ll have to pay for a Notice of Assignment, also known as a Notice of Transfer, too. Your conveyancer sends this to the landlord informing them you are the new owner. However while some management firms don’t charge for this, others charge up to £300.

Compare conveyancing quotes and save on your solicitor fees:

Get instant quotes from regulated and reviewed conveyancing solicitors that cover your area. Our customers save on average £490.

Conveyancy is the area of law that draws the most complaints, according to the Legal Ombudsman – it accounted for a third of all issues reported in 2023/2024. This highlights how important it is to choose the right conveyancing solicitor. See our guide on important questions to ask your conveyancing solicitor before instructing.

And don’t just accept your estate agent’s recommendation for a conveyancing solicitor, they may be earning commission on this introduction and their suggestion may not be the best fit. You may prefer to avoid your estate agent’s in-house services for this reason. So always shop around. For local conveyancing fees and advice on Finding the best conveyancing solicitors in London, Birmingham or Manchester, see our local conveyancing pages. For costs and quotes for all areas, see our free tool and compare conveyancing quotes.

Here are the key qualities to look for in a conveyancing solicitor:

There are different types of conveyancers. Each has different levels of experience and will likely charge different fees.

You can find out more with our guide to the difference between a solicitor and conveyancer.

Fixed fee conveyancing means you agree a price at the outset that you will pay your conveyancer for their services. However, the ‘fixed’ fee relates to the conveyancer’s work. And while the cost of disbursements you’ll need to pay should be in your quote, this cost could increase if, for example, you need more searches.

Some conveyancing solicitors may offer a ‘no sale, no fee guarantee’. This means that if your sale falls through, you won’t have to pay the full conveyancing bill. Some may waive the legal fees, but it’s wise to get a clear explanation of what the guarantee covers before you hire their services. You can find out more with our guide to no sale no fee conveyancing.

Online conveyancing is when the legal process of buying or selling a property takes place solely online or over the phone. You won’t meet your conveyancer face to face. However, some High Street conveyancers offer online aspects to the conveyancing process which can speed things up.

Here are some of the ways online and traditional conveyancing compare:

Local knowledge: A traditional estate agent may have good relationships with local estate agents. Although a good conveyancer should offer an excellent service whether or not they have local connections.

Cost: Online conveyancing quotes may be cheaper but don’t fall into the trap of seeing a cheap headline quote, then discover later on that you need to pay for lots of add-ons that push up the cost of conveyancing. Read more in our guide on What to expect from online conveyancing.

Speed: Online conveyancing can be faster due to the efficiency of online document management.

Service: Traditional conveyancing typically offers a more personal service and you’ll usually have one point of contact. With online conveyancing, you may speak to a different person each time.

Find the right conveyancing solicitor for you – compare quotes & ratings instantly

You can save on conveyancing fees by:

Get instant quotes from regulated and reviewed conveyancing solicitors that cover your area. Our customers save on average £490.

Whether or not you have to pay remortgaging conveyancing fees depends on:

Find out more in our guide: Remortgaging: Do I need a conveyancing solicitor? and if you need a conveyancing solicitor use our tool to compare quotes for remortgage conveyancing.

When you instruct a conveyancer or solicitor, you’ll usually need to send them an upfront payment on account. This is typically £250-£500 but may be more depending on the conveyancer and if you’re buying a leasehold property.

This payment on account covers costs such as anti-money laundering checks, getting a copy of the title deeds from the Land Registry and applying for local authority searches. You’ll usually then pay the rest of your conveyancing fee on completion.

Remember: if you are not satisfied with the service from your conveyancing solicitor, it is usually possible to change solicitors. If you are unhappy with your final bill and think you have been overcharged, you have a right to complain.

The average conveyancing fee when buying and selling a house is £2,434, according to Reallymoving’s Conveyancing Costs Index Q1 2025. This is an increase of 11.9% between Q1 2024 and Q1 2025. Reasons for the rise of conveyancing fees include the rush to beat the stamp duty deadline and fierce competition for conveyancing services which drove prices to a record high.

The best way to save on conveyancing fees is to shop around and compare quotes. Users of our panel save on average £490 on their conveyancing fees.

When you purchase an investment property, you’ll have to pay Buy to Let solicitors fees to cover the costs of the conveyancer handling the legal site of your purchase. Buy to Let conveyancing costs depend on a number of factors such as the property value, the location and whether additional work is required, such as searches due to a nearby river or coal mine. Average solicitor fees for a Buy to Let are around £850-£1,500 but they can be higher for leasehold properties.

On top of this you will need to pay additional fees such as for local authority searches. Read more in our guide on Buy to Let conveyancing.

Make sure you get a number of Buy to Let conveyancing quotes. Use our handy tool to get instant quotes from regulated and reviewed conveyancing solicitors that cover your area.

Get instant quotes from regulated and reviewed conveyancing solicitors that cover your area. Our customers save on average £490.

New build conveyancing can be more complex as you’ll be buying a property that hasn’t been completed yet. There’s a reservation fee to deal with, usually a short deadline to get to exchange of contracts, then there will be more work to be done to get you to completion once your home is ready.

New build solicitor fees will vary depending on for example the value of the property, whether it’s leasehold and whether you use a solicitor or a licensed conveyancer.

Developers will sometimes offer to cover your new build solicitor fees. But before agreeing to have the house builder contribute to or pay your legal fees, make sure this doesn’t come with strings attached. Often the house builder will have an arrangement with a legal firm. But you should not feel obliged to use them. Shop around for the best legal firm. A good place to start is our guide to new build conveyancing.

And as the process of buying a new build is different to buying an older property, it’s advisable to use a conveyancer who is experienced in this type of property.

If you’re buying a new build leasehold flat, you’ll find useful information in our guide Leasehold conveyancing: Fees, process and how long it takes.

Conveyancing is the legal process to transfer the ownership of a property from one person to another. The conveyancing process starts when an offer on a house is accepted and finishes when the buyer receives the keys. Find out more in our guide Conveyancing process explained for buyers

Average conveyancing fees when buying a house range from around £500-£1150 plus disbursements. These disbursements could add on up to £700 or even more. While conveyancing costs when selling average between around £610-£950. But fees can vary widely so make sure you compare conveyancing quotes. Use our conveyancing fees calculator to get instant quotes from quality assured firms in your local area.

Fixed fee conveyancing means you’ll pay a fixed price for conveyancing fees that you are quoted at the outset. But ‘fixed’ usually relates to the legal services provided not disbursements. Disbursements should be included in the quote but for example if more searches are required this cost will increase. So make sure you compare conveyancing quotes. Get instant quotes from quality assured firms in your local area with our handy tool.

Licensed conveyancers are specialised in property transactions and it’s their main focus. In most cases, a conveyancer will be able to handle your transaction from beginning to end. Solicitors can charge higher fees than conveyancers as they are able to offer a full range of legal services. But in some circumstances, for example where you are selling as part of a divorce, instructing a solicitor may be the best bet. Find out more in Find the right solicitor or conveyancer.

While it’s not a legal requirement that you hire a conveyancing solicitor, it’s a very specialised skill and your mortgage lender may insist that you use a professional. However, it is possible to do conveyancing yourself if you don’t have a mortgage.

It’s highly likely that you’ll need to hire a conveyancing solicitor if you’re transferring equity on a property. For example if a relationship ends and the property is transferred to one of the couple. The typical activities that you could be charged for include a bankruptcy search, Land Registry search, identification search and transfer fees as well as the legal costs. And if you’re planning to remortgage you’ll face other conveyancing costs associated with this.

HomeOwners Alliance Ltd is registered in England, company number 07861605. Information provided on HomeOwners Alliance is not intended as a recommendation or financial advice.

Mortgage service provided by London & Country Mortgages (L&C), Unit 26 (2.06), Newark Works, 2 Foundry Lane, Bath BA2 3GZ, authorised and regulated by the Financial Conduct Authority (FRN: 143002). The FCA does not regulate most Buy to Let mortgages. Your home or property may be repossessed if you do not keep up repayments on your mortgage.

HomeOwners Alliance Ltd is an Introducer Appointed Representative (IAR) of LifeSearch Limited, an Appointed Representative of LifeSearch Partners Ltd, authorised and regulated by the Financial Conduct Authority. (FRN: 656479).

Independent Financial Adviser service is provided by Unbiased, who match you to a fully regulated, independent financial adviser, with no charge to you for the referral.

Bridging Loan and specialist lending service provided by Chartwell Funding Limited, registered office 5 Badminton Court, Station Road, Yate, Bristol, BS37 5HZ, authorised and regulated by the Financial Conduct Authority (FRN: 458223). Your property may be repossessed if you do not keep up repayments on a mortgage or any debt secured on it.