Find the best estate agent near you Start here

Downsizing to a smaller house may become appealing as you get older. It can free up cash, save you money on your bills and mean you live in a property better suited to your needs. But it’s vital to consider the pros and cons of downsizing your house first.

According to data from Reallymoving, 25% of UK home movers in September 2025 reported that they are buying a property for less than they are selling for.

From downsizing your house to save money to having a more manageable property to look after, there are a range of benefits of downsizing your home including:

Releasing equity: One of the main advantages of downsizing your house is that by selling your current home and buying a smaller, less expensive property you can free up equity locked in your property. You can use the proceeds to pay off your mortgage if you are coming to the end of your mortgage term, fund retirement or help children or grandchildren to buy their own home.

Cheaper bills: Downsizing your house can reduce the cost of bills. According to Ofgem data analysed by Uswitch, the estimated average monthly dual fuel bill for a 1-2 bedroom house is £115.14 compared to £228.74 for a house with 5 bedrooms or more. This saving amounts to more than £100 a month.

Less maintenance: Smaller homes generally require less general maintenance. So while you might be fine with the current level of cleaning and maintenance, it’s wise to look to the future and consider how you would cope in future years.

Move to a better served location: If you live in a rural area and depend heavily on driving to get to local amenities, you might want to consider downsizing your house and moving somewhere with good transport links and a well-serviced high street in close proximity with local arts, leisure facilities and doctors surgery.

Closer to family: Downsizing your house may mean you can move closer to children or other family members.

When weighing up the pros and cons of downsizing your home you’ll also need to think about the reasons not to downsize. These may include:

You’ll need to factor in the costs of downsizing your house because the cost of moving house can be considerable.

Use our cost of moving calculator to get a rough idea of the costs to budget for when considering whether to move and downsize your home:

Whether or not you should downsize your home and pay off your mortgage will depend on your circumstances such as can you afford to buy a property that will suit you long term if you downsize your house now? Will you have any fees to pay if you pay off your mortgage, such as an early repayment charge?

If you’re downsizing your house and buying a new home outright, these are some of the main property types you may choose:

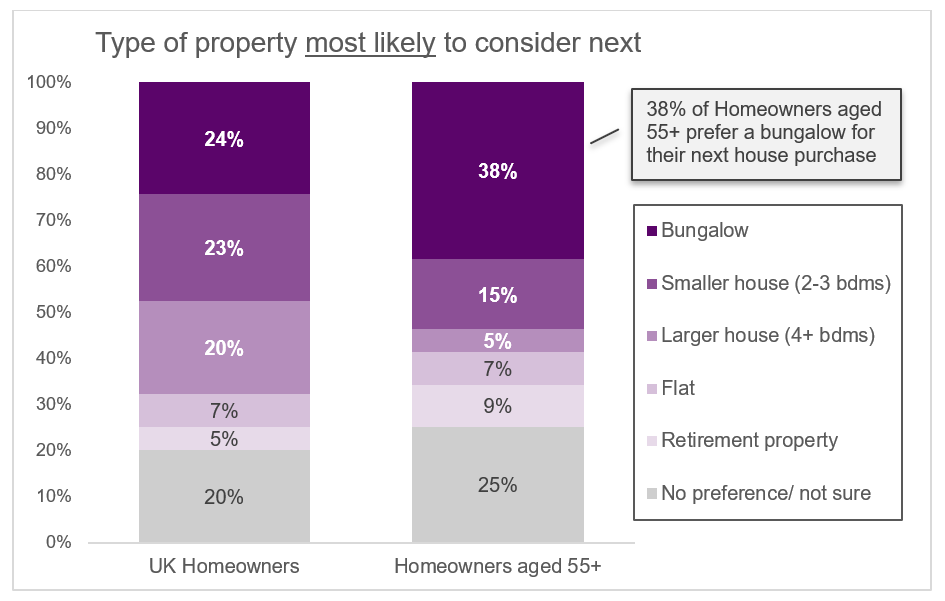

Our 2025 Homeowner survey found that bungalows are the preferred property type for potential downsizers with 38% of homeowners aged 55+ favouring this type of property for their next move.

Many downsizers will sell their current property and buy their new property in the traditional way. But there are other options when downsizing your house in the UK including:

Shared ownership: If you can’t afford a property or want to put your equity elsewhere, then you could consider shared ownership. This allows you to buy a share of a property from a housing association, retirement village or private developer (typically from 25% to 75%) and pay rent on the remaining share. Larger shares can be bought over time.

Although a key difference with Older Person Shared Ownership, is that the maximum share that you can buy is normally 75%, rather than the usual 100%. There’s a lot to consider before opting for shared ownership – read our guide What is Shared ownership? Is it worth it? Also, if you’re considering a retirement village, also read our guide Hidden costs of retirement properties.

Developers’ downsizing schemes: Some developers have ‘downsize schemes’ where they will help you find a buyer for your current property so that you can buy a new build property from them. This may make the process of downsizing your house easier but there are downsides to consider such as having less choice or properties. Also, you may be able to get more for your property if you sold on the market. Using any scheme from a developer can also make it harder to negotiate a better price on the property you are buying too.

Part exchange: Some developers offer part exchange schemes that offer downsizers the opportunity to trade in their house against the value of a new build property bought from a developer or builder. However, as well as issues such as property valuation offers often equating to a lower than achievable market price, most homebuilders will only consider homes worth up to a certain amount of the new build value (usually around 70-75%), so downsizers will have to take on a more expensive property. Read mroe in our guide to Buying a Part Exchange House from a Developer

Renting: You could decide to invest the equity from your home and use the income to cover the cost of renting a property. But there are other considerations to take into account with renting as you may not have the guarantee of a long term lease and there could be the possibility of rent rises over time.

Get instant quotes from regulated and reviewed conveyancing solicitors that cover your area. Our customers save on average £490.

Some people are put off downsizing because they don’t want the stress of buying and selling a house at the same time. One way to avoid this is to take out a bridging loan so that you can buy your new property before selling your current one.

By doing this, you’ll be a chain-free buyer which will make you more appealing to many sellers. Also, you can take your time selling your property if you want to, so you may be able to hold out and sell it for a higher amount. Find out more in our guide Bridging loans explained.

Use the experienced team of specialist brokers at Chartwell Funding for FREE advice when securing your bridging loan. Click here or call them on 01454 809 300.

Smaller houses are not necessarily less expensive but can be cheaper to run. If you want to move to be closer to family, you may be restricted in where you can move to and may end up competing with first time buyers, landlords and new families who are also looking for smaller properties with gardens, amenities within walking distance and good transport links.

With low stocks of suitable housing helping to push property values upwards, it may be difficult when you are downsizing your home for retirement to find a suitable home at a price which will make moving worthwhile.

Decluttering to downsize can be very time consuming. Here’s how to get started:

There is no set right time when it comes to downsizing your house to a smaller home, but there may be another life event that triggers you thinking about downsizing your house, such as retirement, the final payment on your mortgage or moving nearer to grown children and grandchildren.

It makes sense to consider downsizing your house before you get too old, as the accumulated stress, hassle and sheer timescale of negotiating and completing a house move should be easier to deal with at this stage, when you are still relatively fit and healthy, as opposed to later in life when illness or mobility issues potentially start to take their toll. For some, downsizing at 55 is a good time of life, but others will be older or younger.

The psychological or emotional upheaval of moving from a family home, full of poignant memories, or of saying goodbye to friends and family is another significant obstacle to factor in, but the sooner you move, the sooner you are likely to make new friends and feel settled.

If you are considering selling, see our step-by-step guide to selling to get you started

You may decide that moving and downsizing your house to release equity isn’t for you, so what other options exist? There are a few other options available to you in retirement if you have equity locked in your home.

Get fee-free advice on retirement mortgages from award-winning mortgage brokers L&C

Downsizing your house usually means moving to a smaller or less valuable property and is most commonly associated with retirees or those whose children have left home.

If you have a repayment mortgage and you come to the end of the mortgage term, often 25, 30 or 35 years, you will usually have paid off your mortgage and own your home outright. If you have an interest-only mortgage. If you have an interest-only mortgage, you must repay the full amount borrowed at the end of your interest-only mortgage term. If you can’t repay the lump sum, your options include extending your mortgage term, remortgaging, selling your property or downsizing to release equity and pay off the mortgage.

HomeOwners Alliance Ltd is registered in England, company number 07861605. Information provided on HomeOwners Alliance is not intended as a recommendation or financial advice.

Mortgage service provided by London & Country Mortgages (L&C), Unit 26 (2.06), Newark Works, 2 Foundry Lane, Bath BA2 3GZ, authorised and regulated by the Financial Conduct Authority (FRN: 143002). The FCA does not regulate most Buy to Let mortgages. Your home or property may be repossessed if you do not keep up repayments on your mortgage.

HomeOwners Alliance Ltd is an Introducer Appointed Representative (IAR) of LifeSearch Limited, an Appointed Representative of LifeSearch Partners Ltd, authorised and regulated by the Financial Conduct Authority. (FRN: 656479).

Independent Financial Adviser service is provided by Unbiased, who match you to a fully regulated, independent financial adviser, with no charge to you for the referral.

Bridging Loan and specialist lending service provided by Chartwell Funding Limited, registered office 5 Badminton Court, Station Road, Yate, Bristol, BS37 5HZ, authorised and regulated by the Financial Conduct Authority (FRN: 458223). Your property may be repossessed if you do not keep up repayments on a mortgage or any debt secured on it.