Find the best estate agent near you Start here

If you're buying a house you'll need to budget for solicitor fees: the average cost in the UK is £1,474. But by following our tips, you could save hundreds of pounds.

KEY INFORMATION

A solicitor looks after the legal process of transferring ownership of a property from the seller to you as the buyer – this process is known as conveyancing. The process can also be handled by a licensed conveyancer.

Their responsibilities include:

Get instant quotes from regulated and reviewed conveyancing solicitors that cover your area. Our customers save on average £490.

Solicitors fees when buying a house are broken down into two parts:

| Fee | What it’s for | Amount |

| Anti-money laundering checks | Legal checks to verify your identity | £6 – £20 |

| Bankruptcy search | This verifies if the buyer is bankrupt or about to be bankrupt | £4 |

| Local authority searches | These can identify potential issues with the property | £250 – £450 |

| Property fraud check | Confirms the lawyer you’re sending money to is a real company | £10 |

| Bank transfer fees | You’ll pay the bank’s telegraphic transfer fee to guarantee funds reach an account on a certain day. Plus, your solicitor will charge a fee for performing the transfer. | £20 – £30 |

| Stamp Duty Land Tax | You’ll need to pay stamp duty if you buy a property over £125,000 in England & NI. It’s charged on a sliding scale and the rules are different for first time buyers and Buy to Lets. Different rates apply in Scotland & Wales. | 0 – 17% |

| Unregistered property supplement | If the property is unregistered it involves extra work for the conveyance. This fee covers the work. | £120 – £240 |

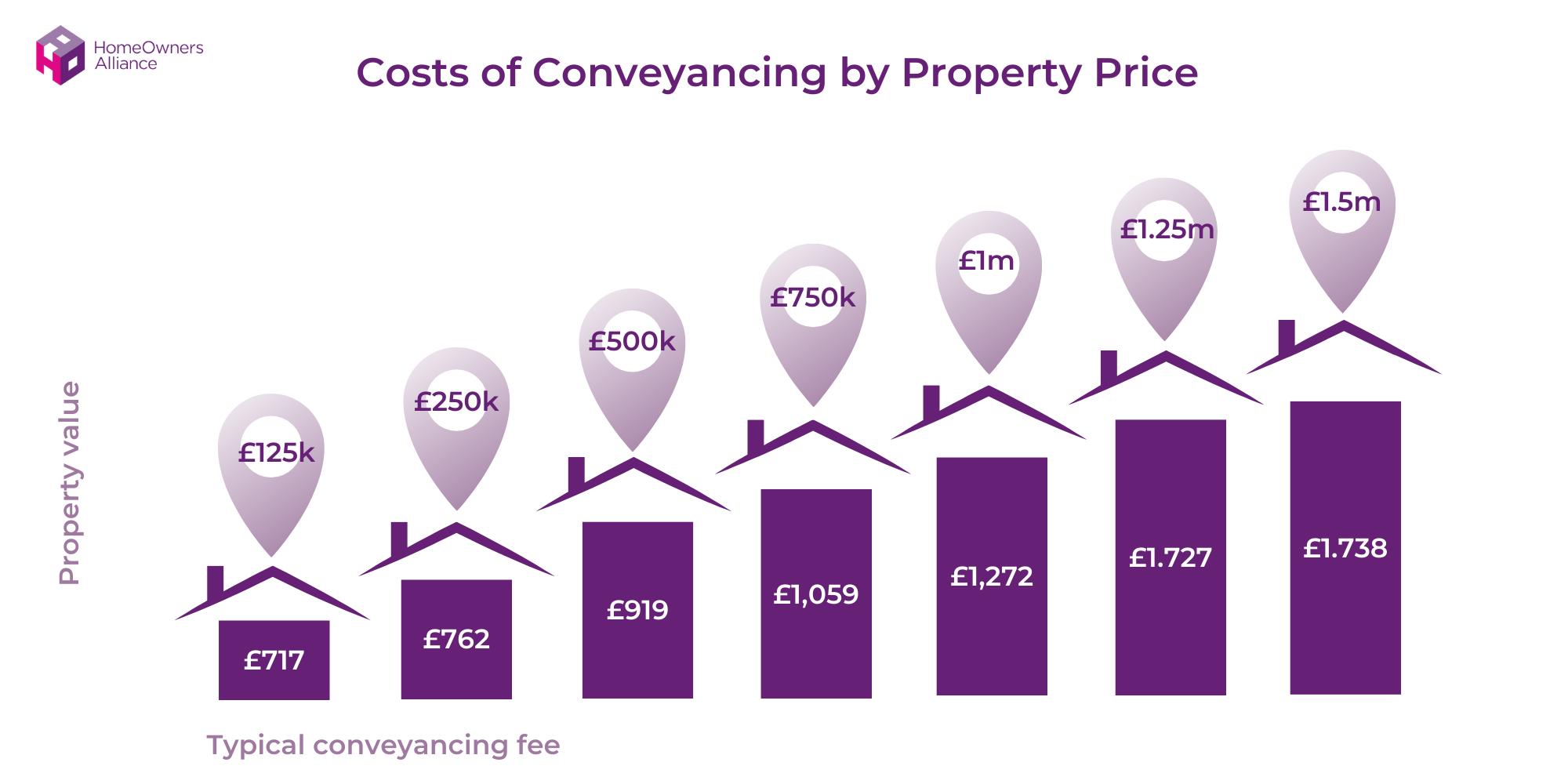

Although costs vary region by region, and depend on whether you’re buying with a government scheme or buying a leasehold, as these are often more complex, it’s helpful to see the average conveyancing solicitor costs according to the price of the house you’re buying. The table below lists the latest data from our conveyancing partners at Reallymoving.

| Property price | Average fees |

| Up to £125,000 | £717 |

| Up to £250,000 | £762 |

| Up to £375,000 | £842 |

| Up to £500,000 | £919 |

| Up to £750,000 | £1,059 |

| Up to £1,000,000 | £1,272 |

| Up to £1,250,000 | £1,727 |

| Up to £1,500,000 | £1,738 |

These figures include VAT but exclude disbursements and are based on buying a freehold property. You can get an exact cost of your legal fees with our conveyancing solicitor fee calculator

KEY INFORMATION

You can save money on solicitor fees by following these steps:

Shopping around and comparing quotes is key to saving money on solicitors fees. The quickest way to do this is by using online tools to find the best deal. Get quotes instantly.

Make sure you get a quote for fixed fee conveyancing. This is widely available and means you agree a price at the outset and avoids having to pay per hour. However, the ‘fixed’ fees relate to the legal work. The disbursement costs should be included in the quote but these costs could increase if, for example, you need more searches.

When using a solicitor offering a ‘no sale, no fee guarantee’, if your sale falls through, you won’t have to pay the full conveyancing bill. Some may waive the legal fees, but get a clear explanation of what the guarantee covers first. Find out more with our guide to no sale no fee conveyancing.

When you’re buying a house, the estate agent you’re buying it through may recommend a conveyancing solicitor. But they may be earning commission on this introduction and their conveyancing suggestion may not be the best choice for you. So get a quote, but always shop around.

Licensed conveyancers are specialised in property transactions and in most cases, a conveyancer will be able to handle your transaction from beginning to end. Solicitors can charge higher fees than licensed conveyancers because they can offer a full range of legal services. If however your transaction is more complex, such as if there’s a boundary dispute, instructing a solicitor may be the best bet.

Ask if all disbursements are included in the quote. If not, you could end up spending more than you’d anticipated.

This may be more likely to be successful if your property transaction is straightforward.

If you are buying a leasehold property then your legal fees will be higher.

| Fee | What it’s for | Amount |

| Notice of Assignment | Your conveyancer sends this to the landlord informing them you are the new owner | Up to £300 |

| Notice of Charge | If you’re buying with a mortgage, this is sent to the landlord telling them the lender has an interest in the property. | £50 – £200 |

| Deed of Covenant | A legally binding agreement between the buyer and landlord or management company about factors such as carrying out repair work. | £50 – £500 |

| Leasehold property supplement fee | This covers the additional work required if you’re buying a leasehold property. | £200 – £300 |

However, these fees vary from property to property and you may not need to pay all these fees. Your solicitor will provide you with more detailed information. Find more information in our guide on Leasehold conveyancing.

No, sellers have to pay for the Leasehold Management Pack which contains information about service charges etc. The cost for this is typically £500 but can vary significantly from £300 to as much as £800.

The average cost of solicitors fees for first time buyers is £1,314, according to Reallymoving. This is lower than the UK average solicitors fees of buying a house of £1,474. First time buyers don’t get discounts on solicitor fees but other factors may mean first time buyer solicitor fees may be lower such as buying cheaper properties.

Shop around and compare quotes now! Use our service and save £490 on average

New build conveyancing is more complicated than the standard conveyancing process when buying because the potential for something to go wrong is much higher. For example, some potential problems are:

This means that finding a good conveyancing solicitor to oversee the purchase of your new build property is essential. Read more in our guide New build conveyancing explained.

A lawyer may charge a fee to cover the additional work if you’re buying with a mortgage. If so, this mortgage handling fee may cost around £60-£200.

The easiest way to get the best quotes is to use our handy conveyancing solicitor fees calculator.

Get instant quotes from regulated and reviewed conveyancing solicitors that cover your area. Our customers save on average £490.

Your solicitor will ask for a deposit up front or ‘payment on account’ to cover costs such as anti-money laundering checks, getting a copy of the title deeds from the Land Registry and applying for local authority searches. This means you can typically expect to pay £250-£500 at the start of the process.

You’ll usually then pay the rest of your solicitor fees at the end of the process.

There may be some additional fees to pay when buying a house depending on your circumstances.

| Fee | What it’s for | Amount |

| Gifted deposit | Those getting a gifted deposit will likely need to pay more to cover the paperwork proving the money comes from a legitimate source. | £50 – £100 |

| Lifetime/Help to Buy ISA | This covers the extra work for your conveyancer to redeem your ISA bonus | £60 |

| Shared Ownership | You may pay higher legal fees if buying a via a government scheme like Shared Ownership due to the additional work involved | £300- £400 |

See how much you could save on conveyancing solicitors fees: Compare quotes now!

Get instant quotes from regulated and reviewed conveyancing solicitors that cover your area. Our customers save on average £490.

If your property sale falls through, some conveyancers offer a ‘no sale, no fee’ service, meaning you won’t have to pay their legal fees. However, you may still need to cover any disbursements already incurred.

You might want to consider getting Home Buyers Protection Insurance. It allows you to claim back some of your solicitor/ conveyancing fees, survey costs/mortgage valuation fees and mortgage/lender fees in the event of your purchase falling through. And with around 1 in 3 property purchases falling down, getting Home Buyer Protection Insurance in place could prove a wise investment. It costs from just £69.

Cover for conveyancing, mortgage and survey costs, should your property purchase fall through.

If you’re a cash buyer you can do your own conveyancing but if you’re buying or selling with a mortgage, the lender will almost certainly insist that you instruct a conveyancer.

However, be warned: the conveyancing process is time-consuming and complex and you shouldn’t consider DIY conveyancing if you don’t fully understand all the steps and the risks involved. Find out more in our guide Can you do your own conveyancing

Choosing the right conveyancer or solicitor is key to getting the best service at the best price.

Here are the key qualities to look for in a conveyancing solicitor:

Also, see our guide on important questions to ask your conveyancing solicitor before instructing.

No, you cannot add conveyancing fees to your mortgage.

Conveyancing solicitor fees need to be paid by both the buyer and the seller of the property. Each will pay their own conveyancer or solicitor for the work carried out. However, some fees will only apply to the buyer like property searches and other costs will only apply to the seller.

The amount of stamp duty you’ll pay depends on the value of the property you’re buying, where in the UK you live, whether you’re a first time buyer, whether it’s an additional property and whether you’re a UK resident. If you’re buying a house for £300,000 in England, stamp duty costs £5,000 in most cases. If you’re a first time buyer, your stamp duty bill will be £0. But if you’re buying an additional property your stamp duty will cost £20,000.

Find out more in our guide Stamp duty: Who pays it? When? And how much?

A conveyancer is a specialist in property law whereas a solicitor is a fully qualified lawyer who can offer full legal services such as divorce proceedings or taking someone to court. Because of their broader legal expertise, solicitors are almost always more expensive than licensed conveyancers. See our guide to the difference between a solicitor and conveyancer.

HomeOwners Alliance Ltd is registered in England, company number 07861605. Information provided on HomeOwners Alliance is not intended as a recommendation or financial advice.

Mortgage service provided by London & Country Mortgages (L&C), Unit 26 (2.06), Newark Works, 2 Foundry Lane, Bath BA2 3GZ, authorised and regulated by the Financial Conduct Authority (FRN: 143002). The FCA does not regulate most Buy to Let mortgages. Your home or property may be repossessed if you do not keep up repayments on your mortgage.

HomeOwners Alliance Ltd is an Introducer Appointed Representative (IAR) of LifeSearch Limited, an Appointed Representative of LifeSearch Partners Ltd, authorised and regulated by the Financial Conduct Authority. (FRN: 656479).

Independent Financial Adviser service is provided by Unbiased, who match you to a fully regulated, independent financial adviser, with no charge to you for the referral.

Bridging Loan and specialist lending service provided by Chartwell Funding Limited, registered office 5 Badminton Court, Station Road, Yate, Bristol, BS37 5HZ, authorised and regulated by the Financial Conduct Authority (FRN: 458223). Your property may be repossessed if you do not keep up repayments on a mortgage or any debt secured on it.