Find the best estate agent near you Start here

Research from Homeowners Alliance reveals homeowners in the UK may be leaving themselves at risk of financial misery by not staying informed when it comes to their mortgage. The findings also highlight a self-confessed lack of understanding of different mortgage products and confusion with some mortgage terminology.

A 2017 survey of more than 2000 UK adults, including 570 mortgage holders, finds the general public are confident in their ability to manage their money and of what is required to get a mortgage, but they are less sure of mortgage terminology, mortgage products and their ability to choose and secure the best mortgage to suit their needs.

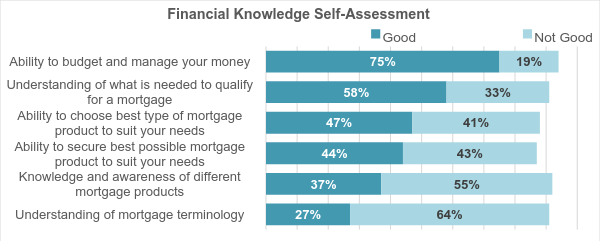

UK adults rate themselves highly for their ability to budget and manage their money (75% rate themselves as good). Most are confident that they understand what is required to qualify for a mortgage (58% rate this understanding as good).

However, people are less sure that they can do a ‘good job’ selecting (47%) and securing (44%) the best type of mortgage product to meet their needs.

Most rate their knowledge of different mortgage products (55%) or understanding of mortgage terminology (64%) as ‘not good’. Among the most common areas of confusion, are the differences between the base rate and short term variable rate and a tracker versus discounted rate mortgage.

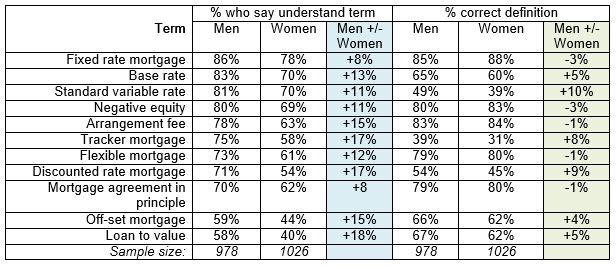

The survey found women tend to be less confident than men in rating their knowledge of mortgage terminology despite actually having similar or better knowledge than men on a number of areas.

Along with the confusion surrounding mortgages, there is also a lack of knowledge over mortgage advice. 38% claim they simply don’t know what it would cost for mortgage advice. Some borrowers (27%) expect advice from an independent mortgage adviser to be free, although this is much lower among aspiring homeowners (17%).

Among existing mortgage holders, more than a quarter (27%) do not know what interest rate they are paying on their mortgage.

The general public feel confident in their ability to manage their money and say they are aware of what is required to get a mortgage but are less sure of mortgage terminology, mortgage products and their ability to choose and secure the best mortgage to suit their needs.

Overall, UK adults rate themselves highly for their ability to budget and manage their money (75% rate themselves as good).

Most are confident that they understand what is required to qualify for a mortgage (58% rate this understanding as good).

But people feel less sure of themselves when selecting and securing the best type of mortgage product to meet their needs (47% and 44% respectively).

And most would rate their knowledge of different mortgage products (55%) or understanding of mortgage terminology (64%) as not good.

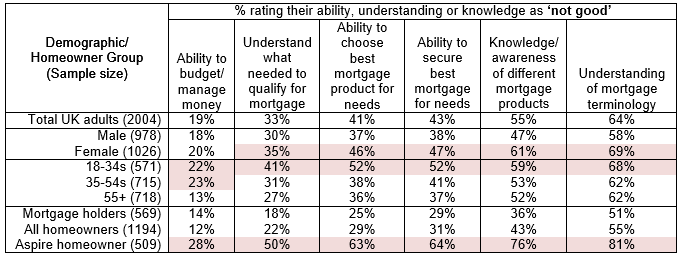

Those less sure of their knowledge of mortgages and ability to find and secure a mortgage include women, younger adults (18-34) and aspiring homeowners.

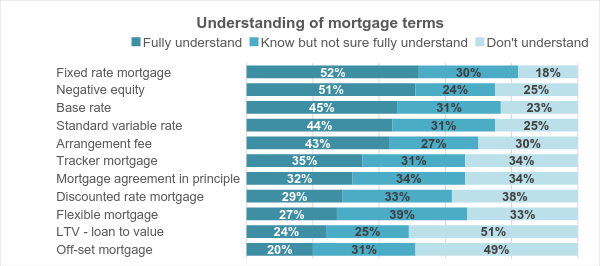

There is a self-confessed lack of knowledge when it comes to basic mortgage terminology.

More than half of UK adults (51%) say they don’t understand loan to value.

A quarter say they don’t know what standard variable rate (25%) or base rate (23%) means.

More than a third of UK adults report they don’t know different types of mortgages – flexible mortgage (33%), tracker mortgage (34%) and discounted rate mortgage (38%).

Thee is confusion as to the difference between the base rate and standard variable rate and tracker and discounted mortgages.

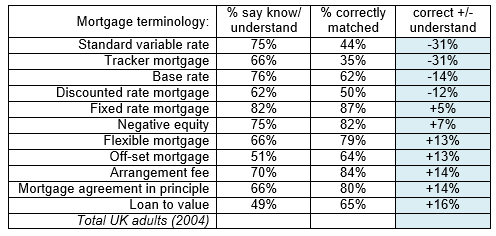

When asked to correctly match definitions with the same set of mortgage terms, there is confusion around some mortgage terms. Misunderstood terms include: the standard variable rate, base rate and the difference between a tracker and discounted rate mortgage. UK adults think they have a better understanding of these terms than they actually do.

Women tend to be less confident than men in rating their knowledge of mortgage terminology.

In reality, however, women have similar or better knowledge than men for some concepts. These include: fixed rate mortgage, negative equity, arrangement fee, flexible mortgage, and mortgage agreement in principle.

Men appear to have a better understanding of types of interest rates, tracker and discounted rate mortgages, offset mortgages and the concept of loan to value.

More than a quarter of mortgage holders have no idea what interest rate they are paying.

More than a quarter (27%) with a mortgage do not know the interest rate they are paying on their mortgage. This proportion rises to a third (33%) among mortgage holders aged 18 to 34.

Women mortgage holders (33%) are more likely than men with a mortgage (23%) to say they don’t know their mortgage rate.

The average interest rate recorded by mortgage holders is 2.4%.

Most people are not sure or expect they will pay for mortgage advice.

More than a third (38%) of UK adults simply don’t know what it would cost for mortgage advice from an independent advisor. The proportion who ‘don’t know’ is higher among women than men (41% vs 34%).

27% overall expect advice from an independent mortgage adviser to be free but this is much lower among aspiring homeowners (17%).

On average, people expect to pay approximately £130 for mortgage advice.

The fieldwork was conducted by Opinium Research 25-26 October, 2017. Sample consists of 2004 online interviews with UK adults; of which 569 have a mortgage, 509 are non-homeowners who aspire to own a home. The sample is weighted to reflect a nationally representative audience. Charts are based on total UK adults sample size unless specified otherwise

Consumers were provided with mortgage definitions and asked to match these with the correct term.

HomeOwners Alliance Ltd is registered in England, company number 07861605. Information provided on HomeOwners Alliance is not intended as a recommendation or financial advice.

HomeOwners Alliance Ltd is an Introducer Appointed Representative of Mortgage Advice Bureau (Derby) Limited which is authorised and regulated by the Financial Conduct Authority.

HomeOwners Alliance Ltd is an Introducer Appointed Representative (IAR) of LifeSearch Limited, an Appointed Representative of LifeSearch Partners Ltd, authorised and regulated by the Financial Conduct Authority. (FRN: 656479).

Independent Financial Adviser service is provided by Unbiased, who match you to a fully regulated, independent financial adviser, with no charge to you for the referral.

HomeOwners Alliance Ltd is an Introducer Appointed Representative (IAR) of Fluent Money Limited, which is authorised and regulated by the Financial Conduct Authority. Calls may be monitored/recorded.