Find the best estate agent near you Start here

April 15, 2024

5 minute read

Homeowning parents worry about the prospects of their adult children who do not currently own their home being able to buy a home and get on the property ladder. Our latest research shows that parents play a pivotal role in helping their children get a foot on the housing ladder and worry about their children who do not currently own their home being able to buy.

Among this group, 59% worry about their children’s chances of owning in the future. Half of parents with adult children who do not yet own a home wish they could do more to support their children financially to buy and a quarter feel a real sense of guilt about the level of support they are able to provide.

Amongst home owning parents with adult children who do not own their home:

Do you feel any sense of guilt because you can’t help more? Let us know in the comments below.

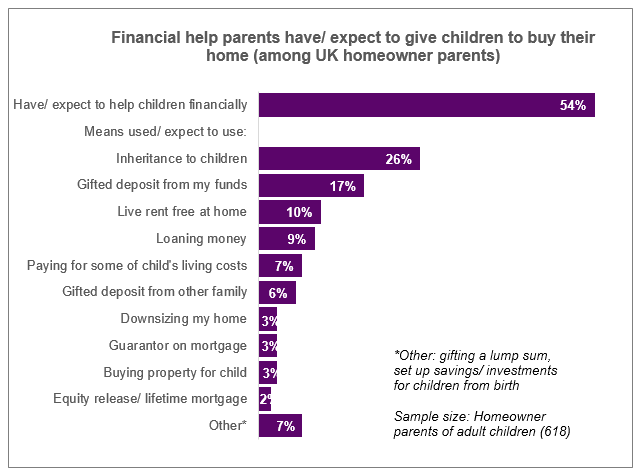

More than half (54%) of parents with adult children (age 18+) have either helped or expect to help their children with financial support to buy a home. Not all parents can afford to offer a gift of a deposit to help their loved ones save for their first home, so financial help comes in many ways. Whether parents are offering to be a guarantor on a mortgage or allowing their adult children to live rent-free while they save, our data shows exactly how parents have or expect to financially support them.

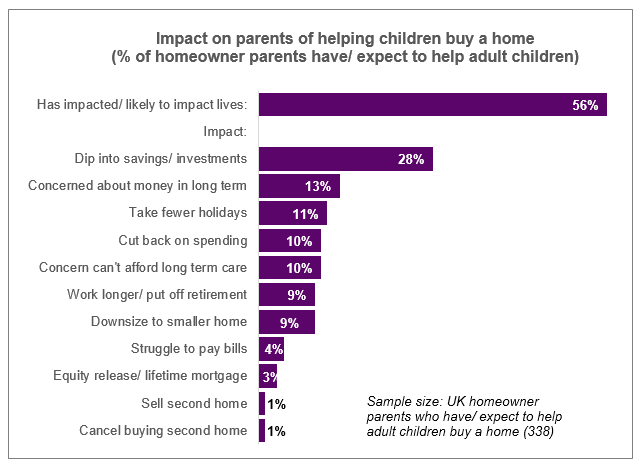

By providing financial support, the majority of parents (56%) expect this to have a direct impact on their own financial position.

Among those who expect to support their children, 28% say this will mean dipping into savings or investments; leaving 13% concerned they won’t have enough money for the long term and 10% worried they might not have enough money should they need long term care. One in ten (9%) parents lending support say they may need to work longer and delay retirement and a similar proportion (9%) say they may need to downsize their home. But this is the price parents are paying to secure their children’s future.

Commenting on the findings, Chief Executive of the HomeOwners Alliance, Paula Higgins said:

While we all know that the Bank of Mum and Dad is supporting many people’s first steps onto the housing ladder, what our survey shows is the emotional and financial strain it puts on families in today’s Britain. Parents with adult children understand the importance of homeownership but are overwhelmingly worried, want to help more and feel guilty they can’t. Beyond the emotional burden, there is a worrying picture emerging of the impact this is having on older parents’ life. Our survey finds that many people are worried that helping may leave them financially short. And 1 in 10 may even delay their retirement and work longer into old age in order to help their child buy a house.

The system is just too pressurised. At one end of a lifetime we have young people giving up on the dream of homeownership unless they’re lucky enough to have access to the bank of mum and dad, while in later life, we see parents using savings and delaying their retirement to help them. We are calling on the government to reinstate local housing targets as a matter of urgency.

Here at the HomeOwners Alliance we are here to help more people realise their dream of becoming homeowners and our advice is here to demystify and guide you through all of your options. So if you want to help your children, or yourself, on to the property ladder, here’s a round-up of our top advice and guides to help you consider your options.

Firstly you will need to work out what you can afford to borrow. Once you know this you will be able to work out what your monthly mortgage repayments will be and work out what deposit you will need. But remember beyond the cost of the mortgage, there are other buying costs you will need to consider too.

Choosing what type of mortgage to get and which lender has the best rates is a minefield. But our advice is to find a fee free mortgage advisor as your very first step as they will be able to assess your financial position to find you the best option. If you want to do your own research on what mortgages are out there, we have a handy guide that showcases the latest, best first time buyer mortgage rates every month.

The first obvious route is to open a Lifetime ISA as it’s a great way to boost your savings with the 25% government bonus. But there are also other tools you can use to save for a deposit. The return of 100% mortgages means you can buy without a deposit at all. Or consider combining your purchasing power by buying with a partner or buying with friends.

There are various ways to get support from the Bank of Mum and Dad including gifted deposits, the Barclays Family Springboard and other types of guarantor mortgage schemes that enable you to borrow more than you could on your own.

Younger homeowners are 3 times more likely to use government home buying schemes to buy a first home, such as Shared Ownership and the First Homes scheme. Other schemes like Deposit Unlock run by house builders to help you buy a new build home with just a 5% deposit. Our guide to first time buyer schemes goes into detail on all of the available options to help you figure out what’s right for you.

March 31, 2026

March 30, 2026

March 16, 2026

March 12, 2026

March 31, 2026

March 30, 2026

March 16, 2026

March 12, 2026