Mortgage rates are edging back up as the Middle East conflict stokes inflation fears. The Bank of England has held interest rates at 3.75%, but that does not necessarily mean the best mortgage rates will stop rising. Read on for today’s lowest mortgage rates, the best remortgage deals, best 5 year fixed rates, Buy to Let mortgage deals - all updated daily.

The best mortgage rates are edging back up after many major lenders hiked borrowing costs amid renewed turmoil in the Middle East.

The Bank of England held Bank Rate at 3.75% on 30 July 2026 for a fifth consecutive meeting. 6 Monetary Policy Committee members voted to hold rates, while 3 voted to increase them to 4%.

The BoE decision does not necessarily mean fixed mortgage rates will remain unchanged. Fixed deals are priced largely according to swap rates, lender funding costs and expectations about future interest rates.

When the mortgage market is volatile, it’s even more important to act early. If you’re buying or remortgaging soon, consider locking in a rate and keeping it under review in case pricing improves before you complete. If you’re remortgaging, you can lock in a new deal up to 6 months before your current deal ends.

But remember, the lowest mortgage rate isn’t always the cheapest overall. Always compare arrangement fees. Also, the rates available to you will depend on factors including your deposit, whether you’re buying or remortgaging, and the type and length of mortgage you choose.

The best mortgage depends on your personal circumstances. We’ve partnered with Mortgage Advice Bureau, and their award-winning expert advisers will find the right mortgage for you.

Source: Mortgage Advice Bureau. Updated: 3 August 2026.Find more about our rates data here. The best mortgage for you depends on your personal circumstances. These tracker mortgage rates cover all variable rate mortgages, including discounted variable rate mortgages.

Fixed Rate Mortgages (Purchase)

The best mortgage rates on fixed deals vary depending on how long you fix for. Here are the best 2, 3, 5 and 10 year fixed rate mortgage deals currently available if you’re buying a house:

Source: Mortgage Advice Bureau. Updated: 3 August 2026. Find more about our rates data here. The best mortgage for you depends on your personal circumstances.

The best 2 year fixed rate mortgage if you’re buying a house is currently available from Danske Bank at 4.13% (fees £1,124).

But when you’re comparing the best mortgage deals for you, you’ll need to factor in any fees so that you can calculate which is the best mortgage deal overall. This matters because a mortgage with a low rate but a high product fee may not be the cheapest option, especially if you have a smaller mortgage.

But don’t worry, you don’t need to work this out yourself – a mortgage broker will do the calculations to find the best mortgage deals available for you.

2 year fixed rate mortgages are one of the most common mortgage types that buyers take out. They can appeal to borrowers who want short-term certainty but do not want to commit to a longer fixed period. Find out more about what you should consider in our guide What type of mortgage should I get?

Source: Mortgage Advice Bureau. Updated: 3 August 2026. Find more about our rates data here. The best mortgage for you depends on your personal circumstances.

Looking for a 3 year fixed deal? The best 3 year fixed rate mortgage in the UK if you’re buying a house is from Halifax (fees £1,099) which offers a rate of 4.38%.

Source: Mortgage Advice Bureau. Updated: 3 August 2026. Find more about our rates data here. The best mortgage for you depends on your personal circumstances.

But don’t just look at rates, remember to factor in any mortgage fees so you can calculate the best deal for you overall. An expert mortgage broker can crunch the numbers to find the right mortgage available for you.

Source: Mortgage Advice Bureau. Updated: 3 August 2026. Find more about our rates data here. The best mortgage for you depends on your personal circumstances.

Looking for a longer fixed deal? The best mortgage rate on a 10 year fixed rate mortgage in the UK is from Halifax at 5.13% (fees £1,099).

A longer fixed rate mortgage can give you more certainty over your monthly repayments, but it may also mean being tied in for longer.

Source: Mortgage Advice Bureau. Updated: 3 August 2026. Find more about our rates data here. The best mortgage for you depends on your personal circumstances. These tracker mortgage rates cover all variable rate mortgages, including discounted variable rate mortgages.

The lowest mortgage rate in the UK on a tracker mortgage is currently from Barclays at 3.99% (fees £1,104). However, it’s important to remember that the rate you’ll pay on a tracker mortgage can go up as well as down. This can make budgeting more difficult if the rate you pay increases.

Source: Mortgage Advice Bureau. Updated: 3 August 2026. Find more about our rates data here. The best mortgage for you depends on your personal circumstances. These tracker mortgage rates cover all variable rate mortgages, including discounted variable rate mortgages.

Looking to take out a 5 year variable rate mortgage? The lowest rate if you’re buying a house is from Barclays at 4.35% (fees £1,104). But remember, the rate you’ll pay on a variable rate mortgage can go up or down.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Please note some branches of Mortgage Advice Bureau may charge a fee for mortgage advice if you go direct. The fee is up to 1% but a typical fee is 0.3% of the amount borrowed. So make sure you use this site, this form or phone number for fee-free advice.

Current best mortgage rates (Remortgage)

These are the current best mortgage rates at different deposit levels for 2 and 5 year fixed rate mortgages and 2 year tracker mortgages if you’re remortgaging.

If your current mortgage deal ends in the next six months, it’s a good idea to review your options now. That way you can secure a new rate, then keep it under review in case rates improve before you need to switch.

Source: Mortgage Advice Bureau. Updated: 3 August 2026.Find more about our rates data here. The best mortgage for you depends on your personal circumstances. These tracker mortgage rates cover all variable rate mortgages, including discounted variable rate mortgages.

Fixed Rate Mortgages (Remortgage)

Remortgaging and looking for a fixed deal? Here are the current best mortgage rates in the UK for 2, 3, 5 and 10 year fixed rate remortgages:

Source: Mortgage Advice Bureau. Updated: 3 August 2026. Find more about our rates data here. The best mortgage for you depends on your personal circumstances.

If you’re remortgaging, the best 2 year fixed rate mortgage rate is currently from Monmouthshire Building Society at 4.38% (fees £1,010). Find more about our rates data and methodology here.

But when you’re looking for the best mortgage deals for you, you’ll need to consider the overall cost including any fees. However, you don’t need to calculate this yourself – an expert mortgage adviser can do this for you.

If you’re remortgaging, it’s a good idea to compare your options with your current lender, known as a product transfer, as well as other lenders. A product transfer may be quicker, but switching lender could give you access to a wider range of deals. A mortgage broker can look at both options for you to help you decide which is best for you.

Source: Mortgage Advice Bureau. Updated: 3 August 2026. Find more about our rates data here. The best mortgage for you depends on your personal circumstances.

While for 3 year fixed rate mortgages in the UK, if you’re remortgaging, the best current rate is from Halifax at 4.50% (fees £999).

Source: Mortgage Advice Bureau. Updated: 3 August 2026. Find more about our rates data here. The best mortgage for you depends on your personal circumstances.

The best mortgage rate on a 5 year fixed rate mortgage is currently from Monmouthshire Building Society at 4.47% (fees £1,010) for remortgages.

Source: Mortgage Advice Bureau. Updated: 3 August 2026. Find more about our rates data here. The best mortgage for you depends on your personal circumstances.

The best mortgage rate on a 10 year fixed rate mortgage in the UK if you’re remortgaging is from Santander at 4.91% (fees £1,224).

Tracker Mortgages (Remortgage)

Here are the lowest mortgage rates in the UK on 2 and 5 year tracker mortgages if you’re remortgaging:

Source: Mortgage Advice Bureau. Updated: 3 August 2026. Find more about our rates data here. The best mortgage for you depends on your personal circumstances. These tracker mortgage rates cover all variable rate mortgages, including discounted variable rate mortgages.

The best 2 year variable rate mortgage for remortgages is currently from Barclays at 4.04% (fees £1,104). Find more about our rates data and methodology here.

But remember, the rate on variable rate mortgages can go up or down. So make sure you can afford repayments if the rate you pay increases.

Also, when you’re looking for the best mortgage deals for you, you’ll need to factor in any mortgage fees so that you can calculate which is the best deal overall. If you’re using a mortgage broker, they will do this for you.

Source: Mortgage Advice Bureau. Updated: 3 August 2026. Find more about our rates data here. The best mortgage for you depends on your personal circumstances. These tracker mortgage rates cover all variable rate mortgages, including discounted variable rate mortgages.

The best mortgage rate on a 5 year tracker mortgage is from Barclays at 4.35% (fees £1,058) for remortgages.

Source: Mortgage Advice Bureau. Updated: 3 August 2026. Find more about our rates data here. The best mortgage for you depends on your personal circumstances.

Here are the best mortgage rates currently available if you have a 10% deposit (90% LTV) and are looking for a variable rate mortgage. Read our Best first time buyers mortgage rates guide – we bring you the best current fixed and variable mortgage rates in the UK whatever your deposit size, from 0% to 40%.

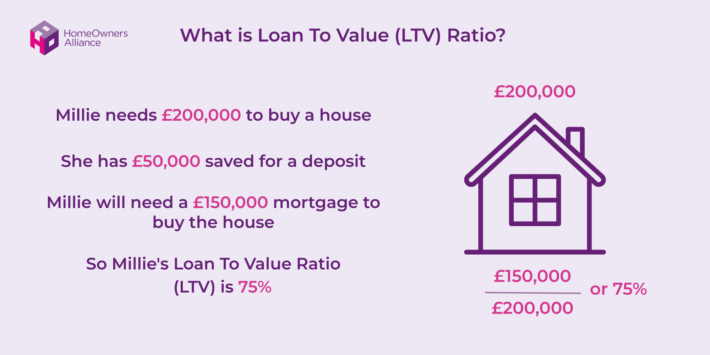

LTV stands for ‘loan to value ratio’ and is the size of your mortgage in relation to the value of the property you’re buying. You can work out your LTV with our handy loan to value calculator.

Your LTV is usually one of the biggest factors affecting the mortgage rates you may be able to access. Generally, the lower your LTV, the more competitive the rates available to you may be.

If you’re buying your first home, read our guide to first time buyer mortgages to understand deposits, affordability, Mortgage in Principle and how to apply before comparing rates.

If you’ve got savings, could you use them to offset the amount of interest you pay on your mortgage? Find out how these mortgages work and the best offset mortgage rates currently available (updated daily) in our guide Offset mortgages explained.

How do I find the best green mortgage rates?

You can find more information on green mortgages including some of the best green mortgage rates currently available in our guide Are green mortgages worth it?

As featured in

Latest mortgage rate news

The Bank of England held Bank Rate at 3.75% on 30 July 2026 for a fifth consecutive meeting. The Bank voted 6–3 to hold rates, with three members voting to raise Bank Rate to 4%.

The hold was widely expected and does not guarantee that fixed mortgage rates will remain unchanged. Lenders may continue to reprice deals in response to swap rates, energy prices and changing expectations about future interest rates.

Major mortgage lenders including Nationwide, NatWest and Barclays have increased rates on fixed deals, following the latest disruption in the Middle East. However, some lenders including Nottingham Building Society have continued to reduce fixed rates.

The picture is very different compared to what we’ve seen in recent weeks, as many lenders had cut fixed mortgage rates multiple times following recent, rapid hikes.

Office for National Statistics figures released in July showed that CPI inflation fell by more than expected to 2.6% in June, down from May’s 2.8% reading. However, this respite isn’t predicted to last long, with renewed fighting in the Middle East pushing oil prices higher once again.

“Unfortunately, we are seeing mortgage rates increasing. This is due to the tension in the Middle East continuing to affect swap rates, which affect mortgage interest fixed rates. We also have a changing political landscape in the UK and that also has an impact on things.”

“As I always say, please encourage anyone that you know that has a remortgage coming up to lock in an interest rate six months before. We cannot say that enough because that is going to help you when this happens in the market and with so much political uncertainty it is likely that we will continue to see movements. If mortgage rates go up again, you’ll have that rate locked in and if rates come down, you can change your rate all the way up until completion.“

KEY INFORMATION

How to secure the best mortgage rates

Whether you’re buying your first home or remortgaging, getting the best mortgage rate for you isn’t just about finding the lowest headline rate. It’s important to compare the overall cost of the mortgage, including any mortgage fees and cashback incentives.

When there’s volatility in the mortgage market, it’s more important than ever to shop around for the best mortgage ratesfor you. If you’re remortgaging, you can do this up to 6 months before your current deal ends.

You can apply for a mortgage and lock in a rate, then keep it under review in case rates improve before you need to switch.

When you’re looking at the best mortgage rates remember to look at the whole picture including any mortgage fees so you can find the cheapest mortgage deal for you overall.

But don’t worry, a mortgage broker will do the calculations for you to find the best mortgage deals available for you.

When will UK mortgage rates come down?

The Bank of England held Bank Rate at 3.75% on 30 July, but this does not necessarily mean fixed mortgage rates will remain unchanged. Experts had previously expected mortgage rates to trend down during 2026, but the outlook has become more uncertain following the conflict in the Middle East and renewed inflation concerns.

The next Bank of England decision is due on 17 September 2026. However, fixed mortgage rates could move before then as lenders respond to swap rates and market expectations.

This unpredictable outlook comes as little surprise to the UK public. In our 2026 research, we found that around a quarter of Brits expect rates to rise (23%) and a similar proportion think they will fall (25%), while 28% expect them to stay the same and 24% are unsure.

On 21 July 2026, the average 2 year fixed mortgage rate in the UK was 5.54%, according to Moneyfacts. The average 5 year fixed mortgage rate was 5.57%.

Average mortgage rates provide a useful benchmark, but many borrowers qualify for rates below the average depending on their deposit, loan-to-value (LTV) and circumstances. However, for other borrowers, the rate they’ll be offered will be higher than these averages.

How much is the average standard variable rate?

The average standard variable rate in August 2026 in the UK is 7.13%. The standard variable rate is the default rate you’ll roll onto when your mortgage deal ends. But SVRs vary widely by lender.

So while the best mortgage rates on offer this month may seem high compared to what has been available in recent years, your lender’s Standard Variable Rate (SVR) could be significantly higher.

If you’re already on your lender’s standard variable rate, it’s worth checking whether you could save money by switching to a new mortgage deal. While this won’t be the right option for everyone, SVRs are often higher than the rates available on new fixed and tracker mortgages.

How to find the best mortgage deals

If your current mortgage deal ends in the next six months you should act now to find the best mortgage deal for you. Here’s our advice:

Shop around: Whether you’re remortgaging or buying a house, don’t just go to your bank for your mortgage. Always shop around for the best mortgage rates for you. Although it’s important to always compare the cost of the whole mortgage, not just the interest rate. Getting fee-free advice from a mortgage broker is the quickest and easiest way to find the best mortgage rate for you.

Act now: The mortgage market has been volatile in recent months. But if you secure a remortgage deal several months in advance you’ll have that in the bag while keeping your eye out for other deals before your remortgage completes. Get fee-free advice from a mortgage broker today to explore your options.

Beware of the SVR: If you’re on your lender’s standard variable rate, check your deal now to see if you can save by remortgaging as average mortgage interest rates on SVRs have soared over the last few years.

Mortgage rates are the rate of interest charged by a mortgage lender (bank or building society). The interest is charged by the lender as compensation for the money they have lent them in order to purchase a property.

Interest rates are determined by the lender and can be either fixed (ie remain the same for the term of the mortgage) or variable (where they fluctuate with a benchmark interest rate). Before you compare mortgages, you need to understand the different types. For more information see what type of mortgage should I get?

How long does a mortgage application take?

A mortgage application usually takes two to four weeks to process. However, factors including how busy the lender is, how straightforward your circumstances are and how quickly you respond to any requests can influence how long it takes for a mortgage to be approved. Find more information in our guide How long does it take to get a mortgage?

APRC stands for Annual Percentage Rate of Charge and shows, as a percentage, the annual cost of a mortgage over its lifetime. It incorporates all relevant charges (including fees) that relate to the mortgage borrowing. This is useful when comparing the best mortgage rates.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Please note some branches of Mortgage Advice Bureau may charge a fee for mortgage advice if you go direct. The fee is up to 1% but a typical fee is 0.3% of the amount borrowed. So make sure you use this site, this form or phone number for fee-free advice.

If the base rate changes, how does it affect my mortgage?

Most trackers track the Bank of England base rate. So an increase to the base rate means your monthly mortgage payments will increase. And if the base rate decreases, so will your mortgage payments.

Discount rate mortgages

Your rate is a discount on the lender’s own standard variable rate (SVR). If the base rate changes, your lender can decide whether to pass on any or all of the increase/ decrease.

Your lender sets the amount you pay. If the base rate changes the lender can decide whether to pass on any or all of the increase/ decrease. These mortgages can be extremely expensive.

Fixed rate vs variable rate mortgages

Here’s an illustration of the rate you’ll pay on a fixed rate mortgage vs how it can fluctuate on a variable rate deal.

Should I remortgage now?

If your current mortgage deal ends in the next 6 months, and certainly if it ends in the next 3 months, you should start the remortgage process now to secure a rate. You can then keep the rate under review in case a better rate comes up before you need to switch.

Being ready with your next move before your current deal comes to an end also means you’ll avoid your mortgage rolling onto your lender’s Standard Variable Rate which is averaging an eye-watering 7.13%. Read our guide Should I remortgage now?

Can I remortgage early?

You may want to remortgage early to get a cheaper rate than you’re currently paying. This may be the case if rates have dropped since taking out your mortgage, or if you now have access to better rates because you’ve built up equity in your property and have a lower LTV. However, it’s important to factor in all the costs, including any early repayment charge, and compare that to any savings you may be able to make by remortgaging before your current mortgage deal ends.

It’s possible to get a mortgage without a deposit, these are called 100% mortgages. But by saving a deposit of at least 5% and ideally at least 10% you’ll typically have access to more lenders and usually better mortgage rates too.

While the lowest mortgage rates are usually reserved for people with a deposit of at least 40%. This may be a cash deposit if you’re buying your first home or this could be equity in your home if you’re remortgaging.

If you’re buying your first home, read our guide to first time buyer mortgages to compare deposit options, understand affordability checks and find out how to apply.

Comparison of how deposit amount affects mortgage rates

Here’s an example of how much you’ll pay on a mortgage if you have a 40% deposit compared to if you have a 10% deposit. These examples are based on the best mortgage rates when taking out a £200,000 2 year fixed rate mortgage over 30 years.

Deposit amount

Best mortgage rate

Monthly mortgage payment

40%

4.13%

£974

10%

4.58%

£1,027

Source: Mortgage Advice Bureau. 23 July 2026.

These examples only take into account the mortgage rate, not any fees you may pay like arrangement fees. To get a better understanding of the overall costs, speak to a mortgage broker who will crunch the numbers to find the best mortgage available for you.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Please note some branches of Mortgage Advice Bureau may charge a fee for mortgage advice if you go direct. The fee is up to 1% but a typical fee is 0.3% of the amount borrowed. So make sure you use this site, this form or phone number for fee-free advice.

Will I pay more for my mortgage in 2026?

This depends on the rate you’re currently paying compared to the best mortgage deal you can get today.

If you’re coming off a cheap fixed rate mortgage, you’ll pay more for your mortgage in 2026.

But if this includes you, don’t put off remortgaging because your costs could increase by much more if you do nothing and roll onto your lender’s standard variable rate when your current deal ends.

You’ll pay less on your mortgage in 2026 if your current mortgage deal is ending soon and the rate you’re paying is higher than you can get on a new deal.

However, always factor in any fees when comparing the cost of mortgages, don’t just look at the rate.

Historic UK mortgage rates (2000-2026)

Average mortgage rates in the UK have changed substantially over the last 25 years. This table shows how they’ve changed since 2000.

Year

2 year fix

3 year fix

5 year fix

2 year variable

2000

6.50%

6.20%

6.00%

6.30%

2001

5.80%

5.60%

5.50%

5.70%

2002

5.20%

5.00%

5.00%

5.10%

2003

4.80%

4.60%

4.50%

4.60%

2004

4.50%

4.30%

4.30%

4.20%

2005

4.40%

4.20%

4.20%

4.10%

2006

4.60%

4.40%

4.40%

4.30%

2007

5.00%

4.80%

4.80%

4.70%

2008

6.00%

5.80%

5.70%

5.60%

2009

4.00%

3.80%

3.70%

3.60%

2010

3.50%

3.30%

3.30%

3.20%

2011

3.80%

3.60%

3.50%

3.40%

2012

3.60%

3.40%

3.40%

3.20%

2013

3.50%

3.30%

3.30%

3.10%

2014

3.40%

3.20%

3.20%

3.00%

2015

3.20%

3.00%

3.00%

2.80%

2016

3.10%

2.90%

2.80%

2.60%

2017

3.00%

2.80%

2.70%

2.50%

2018

2.90%

2.70%

2.60%

2.40%

2019

2.80%

2.60%

2.50%

2.30%

2020

2.70%

2.50%

2.40%

2.20%

2021

2.60%

2.40%

2.30%

2.10%

2022

3.50%

3.30%

3.20%

3.10%

2023

3.50%

4.80%

4.70%

4.60%

2024

4.70%

4.50%

4.40%

4.30%

2025

4.90%

4.09%

4.50%

5.20%

Table data source: Statista

What does LTV mean?

LTV stands for loan-to-value, and tells you what percentage of the home’s value is borrowed. The best mortgage rates are usually available to those with an LTV of 60% or lower.

Pay a fixed rate during your initial term, usually 2, 3, 5 or 10 years. Your monthly mortgage payments won’t increase if interest rates rise, but you won’t pay less if they fall either.

Tracker mortgages

The rate you pay goes up and down in line with the base rate. So if the Bank of England cuts interest rates, your mortgage payments will go down. But if it hikes interest rates, your mortgage payments will go up.

Discounted variable rate mortgages

Discounted variable rate mortgages track under the lender’s standard variable rate. So your rate may go up or down, depending on any changes the lender makes to its standard variable rate.

Standard variable rate

Your lender sets the mortgage rate you pay. If the base rate changes the lender can decide whether to pass on any or all of the increase/ decrease. These mortgages can be extremely expensive.

At HomeOwners Alliance the best mortgage rates in our tables are from the award-winning expert advisers at Mortgage Advice Bureau and are updated regularly. These best mortgage rates do not take into account fees and are for illustration only. The average mortgage rate figures we use are from sources including Rightmove and Moneyfacts.

Frequently Asked Questions

Are five year fixed rate mortgages a good idea?

Some people choose five year fixed rate mortgages to have certainty over their payments for the next five years, however it does mean you could miss out on better mortgage deals in the meantime if rates go down. Our guide 2 or 5 year fixed rate mortgage explains what to weigh up.

However, what’s right for you will depend on your circumstances so it’s a good idea to chat through your options with an expert mortgage adviser.

What is a good mortgage rate?

In August 2026, the current average mortgage interest rate on a 2 year fixed rate mortgage at 60% LTV is 4.59%, according to Rightmove.

In comparison, the best mortgage rates are lower. The best rate on a 2 year fixed rate mortgage in August 2026 is from Danske Bank at 4.13% (Max LTV 60%, fee £1,124).

If you’re looking at the current best mortgage rates in the UK, choosing between a fixed and variable deal such as a tracker mortgage can be a tough decision. The type you choose determines whether you’ll pay a fixed amount on your mortgage each month, or whether it can go up or down.

To check when your current fixed rate mortgage finishes, you’ll need to check your paperwork or contact your lender. It’s a good idea to start the remortgage process up to 6 months before the end of your current deal.

I’m selling: How do I find the best estate agent?

Start by using our Best Estate Agent Finder tool, which compares fees, the average time to sell a property like yours, how often they achieve the asking price and how successful they are at selling similar homes. You may consider using an online agent. Check out our online estate agent comparison table.

Can you apply for a mortgage before finding a house?

You can’t make a full mortgage application until you’ve had an offer accepted on a house but you can get a ‘mortgage in principle‘ before finding a house. Find out more in our guide on Mortgages in Principle.

How much deposit do I need to access the best rates?

The lowest mortgage rates are usually offered to borrowers with large deposits, typically 40% or more of the property value. Having a higher deposit reduces the lender’s risk and can unlock lower interest rates and better deals.

A number of factors can affect the mortgage rate you are offered, including your credit score, deposit size (loan-to-value ratio), length of mortgage deal, personal circumstances like employment status and any existing debts.

Will my rate go up after the fixed term ends?

Once your fixed-rate period ends, your mortgage usually reverts to the lender’s standard variable rate (SVR), which is typically higher and can change at the lender’s discretion. You can avoid unexpected increases by remortgaging onto a new fixed or tracker deal before the fixed term expires. You can start the remortgage process up to 6 months in advance.

How often do lenders update their rates?

Lenders can update mortgage rates as frequently as daily or weekly, depending on market conditions and their internal lending policies. It’s important to check rates regularly if you’re in the market for a mortgage.

What’s the difference between APRC and interest rate?

The interest rate is the percentage charged on the mortgage loan amount, while the APRC (Annual Percentage Rate of Charge) shows total annual cost of your mortgage over its lifetime, including interest and fees, expressed as a percentage.

How do I find the best mortgage rate?

The best mortgage depends on your personal circumstances. So the simplest way to find the best mortgage rate for you is to speak to an expert mortgage adviser.

Get fee-free mortgage advice from Mortgage Advice Bureau today

Get fee-free mortgage advice from the award-winning experts at Mortgage Advice Bureau. No hidden costs, just clear, expert mortgage advice. Compare deals or speak to an adviser today.

Compare thousands of mortgage deals from across the market and book your free appointment with an expert adviser

Key mortgage terms explained

Not sure what some of the terms mean? Here’s a quick guide to the most common mortgage phrases you’ll come across when comparing the best mortgage rates.

The percentage of the property’s value you borrow. For example, a £180,000 mortgage on a £200,000 property is 90% LTV.

APRC (Annual Percentage Rate of Charge)

The total annual cost of your mortgage over its lifetime, including interest and fees, expressed as a percentage. Useful for comparing the best mortgage rates.

The interest rate you’ll be charged for the set period at the start of your mortgage.

Initial rate period

The length of your fixed or variable rate mortgage deal before you switch to the standard variable rate.

Mortgage term

The full length of your mortgage, including any introductory term.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Please note some branches of Mortgage Advice Bureau may charge a fee for mortgage advice if you go direct. The fee is up to 1% but a typical fee is 0.3% of the amount borrowed. So make sure you use this site, this form or phone number for fee-free advice.

How this site works

HomeOwners Alliance Ltd is registered in England, company number 07861605. Information provided on HomeOwners

Alliance is not intended as a recommendation or financial advice.

HomeOwners Alliance Ltd is an Introducer Appointed Representative of Mortgage Advice Bureau (Derby) Limited which is authorised and regulated by the Financial Conduct Authority.

HomeOwners Alliance Ltd is an Introducer Appointed Representative (IAR) of LifeSearch Limited, an Appointed

Representative of LifeSearch Partners Ltd, authorised and regulated by the Financial Conduct Authority. (FRN:

656479).

Independent Financial Adviser service is provided by Unbiased, who match you to a fully regulated, independent

financial adviser, with no charge to you for the referral.

HomeOwners Alliance Ltd is an Introducer Appointed Representative (IAR) of Fluent Money Limited, which is authorised and regulated by the Financial Conduct Authority. Calls may be monitored/recorded.

If you take out a mortgage or protection product through Mortgage Advice Bureau, they pay us a referral fee of 25%. You are not obliged to use their services.

Compare Best Mortgage Rates

See the deals you qualify for & how much you could borrow