Find the best estate agent near you Start here

Critical illness cover offers a financial safety net if you're diagnosed with a serious medical condition. But who needs it, how much does it cost and what does it cover?

KEY INFORMATION

Critical illness cover is a type of insurance that pays out a tax-free lump sum if you’re diagnosed with a serious medical condition listed in your policy.

Being diagnosed with a critical illness can have a major impact on your finances. You may not be able to work for a long period plus, you may face additional costs as a result such as paying for private medical care.

Critical illness cover, also known as critical illness insurance, is designed to help ease this financial burden, leaving you to focus on your recovery.

Common uses of critical illness cover payouts include:

If you’re not sure whether critical illness cover is right for you, it’s a good idea to talk it over with an expert. Our partners at LifeSearch offer fee free advice. They will compare quotes from a range of major UK insurers and all quotes given are without obligation.

Each insurer has its own list of critical illnesses covered, so it’s important to speak to an expert protection advisor before taking out a policy.

However, most policies cover, but aren’t limited to:

You may need to be diagnosed to a certain severity for your policy to pay out and you may need to live for a certain number of days following the diagnosis to be covered.

So it’s important that you thoroughly read your policy documents to determine exactly which illnesses you are covered for, and to what severity.

Your policy documents should make it clear what conditions and illnesses are covered. And if it’s not listed in the policy then it won’t be covered.

While each insurer is different, conditions that generally aren’t covered include:

If you want cover for a certain illness, speak to an expert protection advisor who can recommend a suitable insurer.

Critical illness insurance can be invaluable if you suddenly can’t work for several months or longer due to a serious illness.

You may need critical illness cover if:

You might not need it if:

Our partners at LifeSearch offer fee free advice. They will compare quotes from a range of major UK insurers and all quotes given are without obligation.

When you take out a life insurance policy, you can choose from three different types of cover:

With level term critical illness cover, the amount of cover and your premiums stay the same throughout the term.

Pros of level cover

Cons of level cover

The amount of cover drops over time although the premiums stay the same.

Pros of decreasing cover

Cons of decreasing cover

You may choose to take out increasing cover. This means the amount of critical illness cover increase over time.

Although premiums are usually more expensive and will increase over time too.

To calculate the amount of critical illness cover you need, consider:

One rule of thumb for calculating how much critical illness cover you need, is to multiply your annual income by three. This means you’d be covered financially if you had to stop working for three years due to serious illness.

However, even a small amount of critical illness cover is better than nothing if you’re worried about how you’d cope financially if you become seriously ill in the future.

The easiest way to calculate how much critical illness cover you need is to speak to an adviser who can help you estimate a suitable amount.

While both policies offer financial support if you’re ill, they work differently:

If you’re not sure whether critical illness cover is right for you, it’s a good idea to talk it over with an expert protection advisor.

A combined life insurance and critical illness policy pays out either on death or diagnosis of a critical illness, whichever happens first. This can be more cost-effective than taking out separate policies.

These policies generally only pay out once. However, some policies may give a partial critical illness pay out for a condition and severity that could be deemed less severe. When this happens, it tends to be 25% of the policy is paid out, but the full sum assured is still in place for any future ‘full’ claim.

You may prefer to buy two separate policies, one life insurance and one critical illness insurance policy.

How much you’ll pay for critical illness cover depends on the amount of cover you want and your circumstances.

Generally, the older you are the more expensive the policy will be. But your lifestyle will be taken into account too. For example, a non-smoker could expect to pay less for critical illness cover than someone who smokes.

| Factor | How it affects premiums |

|---|---|

| Amount of cover | The higher the lump sum you could claim, the higher the premiums are likely to be |

| Age | The older you are, the higher premiums are likely to be |

| Health & lifestyle | This includes smoking and alcohol consumption as these can increase your risk of getting certain serious illnesses |

| Occupation & high risk hobbies | The higher your risk of injury, the higher your premiums may be |

| Length of cover | The longer your policy is in place for, the greater your chance of claiming |

| Type of cover | You’ll pay more if you take out an increasing or level term policy, compared to a decreasing term |

Example 1. For a 30 year old office worker, who’s healthy, here’s how much premiums may be for combined level term assurance with guaranteed critical illness over a 25 year term.

| Smoker? | Sum | Monthly premium |

|---|---|---|

| No | £50,000 | £13.49 |

| No | £100,000 | £24.16 |

| Yes | £50,000 | £18.03 |

| Yes | £100,000 | £33.57 |

Example 2. For a 50 year old office worker, who’s healthy, here’s how much premiums may cost for combined level term assurance with guaranteed critical illness over a 25 year term.

| Smoker | Sum | Monthly premium |

|---|---|---|

| No | £50,000 | £58.18 |

| No | £100,000 | £116.37 |

| Yes | £50,000 | £96.61 |

| Yes | £100,000 | £193.21 |

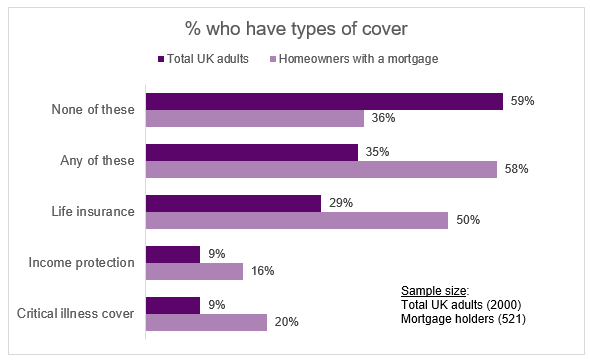

Despite the benefits of these policies, new research from LifeSearch and HomeOwners Alliance reveals 36% of mortgage holders in the UK have no form of life insurance, income protection, or critical illness cover – equating to roughly 2.34 million* mortgage holders nationwide.

The research also found women were more vulnerable to sudden income loss than men. When asked how quickly they’d feel the financial impact if their income stopped due to illness or injury: 14% of women say they would fall behind on mortgage payments immediately, compared to just 6% of men.

Within two months, 27% of women surveyed said they would be in difficulty, nearly twice the proportion of men (14%). And after six months, over half of women (51%) would struggle to keep up, compared to 39% of men.

So if you don’t have protection insurance in place, it’s a good idea to speak to an expert adviser who can explain your options.

There are some steps that may reduce the cost of critical illness cover:

You can buy critical illness insurance by speaking to our partners at LifeSearch.

Yes, you can have multiple policies with different insurers. Each will pay out if their conditions are met.

Only if your inability to work is due to a listed illness. You may also wish to consider income protection insurance, which offers a regular income if you’re unable to work due to an accident or illness and will pay out until you return to work, you retire or the policy expires.

Each insurer will have its own criteria but you’ll usually need to be a permanent UK resident and be over 18 years old. Although upper age limits may apply.

Article written August 2025

HomeOwners Alliance Ltd is registered in England, company number 07861605. Information provided on HomeOwners Alliance is not intended as a recommendation or financial advice.

Mortgage service provided by London & Country Mortgages (L&C), Unit 26 (2.06), Newark Works, 2 Foundry Lane, Bath BA2 3GZ, authorised and regulated by the Financial Conduct Authority (FRN: 143002). The FCA does not regulate most Buy to Let mortgages. Your home or property may be repossessed if you do not keep up repayments on your mortgage.

HomeOwners Alliance Ltd is an Introducer Appointed Representative (IAR) of LifeSearch Limited, an Appointed Representative of LifeSearch Partners Ltd, authorised and regulated by the Financial Conduct Authority. (FRN: 656479).

Independent Financial Adviser service is provided by Unbiased, who match you to a fully regulated, independent financial adviser, with no charge to you for the referral.

Bridging Loan and specialist lending service provided by Chartwell Funding Limited, registered office 5 Badminton Court, Station Road, Yate, Bristol, BS37 5HZ, authorised and regulated by the Financial Conduct Authority (FRN: 458223). Your property may be repossessed if you do not keep up repayments on a mortgage or any debt secured on it.